In W23 in the sugar landscape, some of the most relevant trends included:

- Brazil's sugar production in early May-25 remained stable at 42.5 mmt despite lower TRS levels, with a record-high sugar mix of 51.2%. However, uncertainty over the 2024/25 harvest and a potential 15 mmt crushing shortfall could reduce output and support prices for 2026 contracts.

- India's sugar production is expected to exceed 29.5 mmt in 2025/26 due to improved cane planting and favorable weather conditions, following a five-year low. Despite high ethanol diversion, adequate carryover stocks and domestic demand stability ensure overall supply balance.

- Russia expanded its sugar beet area by 5% YoY, with a projected output of 6.1 to 6.5 mmt, exceeding domestic needs and sustaining export potential. However, low soil moisture and replanting needs raise weather-related production risks into late 2025.

- Ukraine's sugar exports rose sharply in May-25, making sugar the primary contributor to the rise in road-based agricultural exports.

1. Weekly News

Brazil

Brazil's Sugar Market Steady but Uncertain Following Mixed Indicators in Early May Report

The sugar market showed a mixed response following the Brazilian Sugarcane Industry Union's (UNICA) latest report for the first half of May-25. The Total Recoverable Sugar (TRS) was revised downward to 140.5 kilograms (kg) per metric ton (mt). Meanwhile, the sugar mix rose to a record 51.2%, keeping total sugar production steady at 42.5 million metric tons (mmt). Despite stable output, the report raised uncertainties about the actual condition of Brazil’s 2024/25 harvest, prompting cautious market sentiment.

Crushing reached 42.3 mmt during the period, slightly above the five-year average but still trailing 2024's pace. A sharp drop in Apr-25 productivity and reliance on cane carried over from the previous season contributed to this lag. While TRS fell 5% year-on-year (YoY), higher sugar mix levels helped stabilize prices.

The current forecast for crushing in the Center-South region remains at 620 mmt, supported by strong crop health indicators, though a potential 15 mmt reduction scenario has been considered. This would lower sugar output by around 1 mmt and reduce the trade surplus, potentially supporting prices for 2026 contracts. However, significant price rallies remain unlikely unless losses exceed 45 mmt. Continued monitoring of global demand and Northern Hemisphere developments will be key to future market direction.

India

India's Sugar Output Expected to Rebound in 2025/26 Following Improved Cane Planting and Monsoon Outlook

India's sugar production is projected to recover significantly in the 2025/26 season (October–September), following a five-year low of 29.5 mmt expected in 2024/25. Improved sugarcane planting in key states such as Maharashtra and Karnataka, aided by favorable weather and a strong monsoon in 2024, is set to support timely crushing starting Oct-25. The Indian Meteorological Department (IMD) forecasts an above-normal monsoon in 2025, further boosting cane prospects.

Despite a 7% YoY decline in sugar output in 2024/2, driven by poor rainfall in 2023 and red rot disease in Uttar Pradesh, carryover stocks of 5.2 to 5.3 mt on October 1, 2025, are expected to meet early season domestic demand. Ethanol diversion in the current season is estimated at 3.3 to 3.4 mt, up from 2.15 mt in 2023/24. Domestic sugar consumption for 2024/25 is estimated at 28 mt, with exports projected at 0.9 mt. Following export restrictions in 2023/24, the government authorized 1 mt of exports for the current season. Additionally, the fair and remunerative price (FRP) for cane in 2025/26 has been raised by 4% to USD 4.14 per quintal (INR 355/quintal). Indian Sugar Mills Association (ISMA) will release preliminary sugar production estimates for 2025/26.

Russia

Russia Expands Sugar Beet Sowing as Export Outlook Improves Despite Weather Risks

As of early Jun-25, Russia expanded its sugar beet sowing area to over 1.17 million hectares (ha), nearly 5% higher than last year, with further slight increases expected as planting continues in northern regions. The growth was concentrated in the South and Central regions, while areas such as Volga-Ural and Altai Republic saw modest declines. Despite early sowing in the South, replanting occurred in some areas due to late frosts, with sugar beet occasionally replaced by more popular oilseeds such as sunflower oil.

Crop conditions vary by region. While some southern areas show vigorous growth, concerns persist over low soil moisture levels, raising risks if rainfall remains insufficient through Sep-25. Sugar production is projected at 6.1 to 6.5 mmt, in line with last year and above domestic consumption, suggesting continued export potential. Preliminary data indicate a notable rise in rail exports to Commonwealth of Independent States (CIS) countries and Mongolia in May-25. If this trend continues, excess sugar stocks built up over recent years could normalize by the end of the 2024/25 season.

Ukraine

Ukraine's Sugar Exports Lead Rise in Agricultural Road Shipments in May Despite Logistical Challenges

In May-25, Ukrainian agricultural exports by road increased by 10.5% month-on-month (MoM), reaching 324,200 mt. Sugar was the leading export commodity, totaling 39,100 mt, followed by sunflower oil. The highest growth in export volume was recorded at the Moldovan and Romanian borders, while the Hungarian border saw only a modest rise.

Road transport costs for domestic routes declined slightly, while rates on European routes remained stable. As of early June, agricultural export volumes by road totaled 19,500 mt. Despite logistical challenges, strong sugar exports highlight Ukraine's continued role in regional supply chains.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W23 2024 to W23 2025)

.png)

Brazil

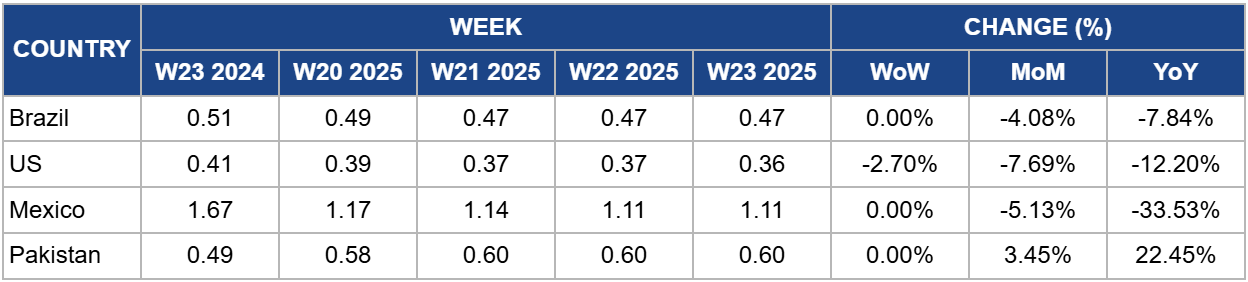

In W23, Brazil's sugar prices held steady at USD 0.47/kg, showing no weekly change but down 7.84% YoY from USD 0.51/kg. This price softness reflects both weaker domestic production and global market dynamics. According to UNICA, Center-South sugar output fell by 6.8% YoY in early May-25 and is down 22.7% cumulatively for the 2025/26 season, largely due to delayed crushing and adverse weather earlier in the season.

However, recent rainfall forecasts are improving expectations for cane yields, which may help stabilize or even increase future output. Despite current production setbacks, the market response has been muted due to already-committed export volumes and expectations of a broader global supply recovery. This limits the immediate price rise, though weather volatility and harvest pace remain key variables. If rainfall continues to support field conditions, recovery in late-season output could further pressure prices through Q3-Q4 2025.

United States

The United States (US) sugar prices fell by 2.70% week-on-week (WoW) to USD 0.36/kg, marking a YoY decline of 12.20% from USD 0.41/kg. This downward trend reflects subdued trading activity and relatively stable domestic supply conditions. However, policy developments are introducing new pricing risks.

The recent implementation of a 10% tariff on Brazilian sugar imports, which is significant given Brazil's role as a top US supplier, is expected to raise import costs. While some of these added costs may be absorbed along the supply chain, they introduce upward pressure on domestic prices. If importers pass on even a portion of the tariff burden, prices may see modest increases in the near term, particularly if domestic supply tightens or if alternative sourcing proves costly. Market participants should monitor import flows and potential supply substitutions heading into Q3-2025.

Mexico

In W23, Mexico's sugar prices held steady at USD 1.11/kg with no weekly changes, though decreased sharply by 33.53% YoY from USD 1.67/kg. This significant annual decline reflects easing domestic market pressures and heightened trade uncertainty.

As of April 19, 2024/25 sugar production reached 3.85 mmt, 1.4% higher than the previous season, indicating steady supply growth. However, the recent imposition of 25% US tariffs on Mexican agri-food exports, including sugarcane, presents a major disruption risk. If these tariffs persist, they may severely constrain Mexico’s export opportunities to its largest sugar trading partner. Furthermore, excess domestic supply could intensify, especially in major producing regions, putting further downward pressure on prices in the near term. Without alternative export outlets or domestic demand growth, Mexican sugar prices may continue to weaken into Q3-2025.

Pakistan

Pakistan's sugar prices held steady at USD 0.60/kg in W23, reflecting no weekly change but a sharp 22.45% YoY increase from USD 0.49/kg. This sustained rise is driven by elevated sugarcane procurement costs, declining recovery rates, and earlier high-volume sugar exports, which have tightened domestic supply.

Despite government interventions, such as price caps, anti-hoarding measures, and subsidized sugar allocations, retail prices remain elevated, ranging between USD 0.58/kg and USD 0.64/kg. With a projected national sugar shortfall of nearly 1 mmt, market fundamentals point toward continued upward pressure on prices. Although raw sugar imports are under consideration to ease supply constraints, their timing and scale will be critical in determining short-term price trends.

3. Actionable Recommendations

Implement Risk-Based Hedging to Address Brazilian Harvest Volatility

Traders and importers should use futures contracts and options to hedge against potential price increases linked to Brazil's uncertain 2024/25 harvest outcomes. With a possible 15 mmt crushing shortfall scenario on the table, locking in favorable prices now can protect margins if supply tightens unexpectedly.

Expand Alternative Export Channels Amid US Tariff Pressures

Sugar exporters from Mexico and Brazil should accelerate diversification into Asian, African, and Middle Eastern markets. With rising tariffs from the US (25% on Mexico, 10% on Brazil), shifting focus to under-tapped regions will help maintain volumes and reduce overreliance on the US market.)

Bolster Strategic Reserves in High-Risk Markets Like Pakistan

Given Pakistan's tight supply and persistent price pressures, government agencies and major distributors should preemptively build sugar reserves via timely imports. Coordinated procurement, particularly ahead of seasonal shortfalls, can help cushion consumers from inflationary shocks and stabilize the domestic market.

Sources: Tridge, Agro Link, Agro Investor, Financial Express, Agronews Castilla y León