In W24 in the soybean landscape, some of the most relevant trends included:

- Argentina’s soybean harvest reached 80.7% completion with stable production at 48.5 mmt.

- Amid US-China trade concerns, China doubled soybean imports mainly from Brazil in May-25 to 13.92 mmt.

- Argentinian soybean prices rose 2.56% WoW in W24 due to tighter domestic supply and steady export demand.

- Brazil's soybean price rose WoW to USD 0.39/kg, despite weaker YoY exports.

- US prices stayed firm at USD 0.46/kg on strong demand and weather-related planting delays.

1. Weekly News

Argentina

Argentina Soybean Harvest Reached 80.7% with Yields Varying Widely Across Regions

Argentina’s 2024/25 soybean production estimate remains steady at 48.5 million metric tons (mmt), with a neutral outlook. As of May 28, harvest progress reached 80.7%, advancing 6.4% over the week. Early-planted soybeans are 86% harvested, though progress is slower in northern Buenos Aires province due to recent heavy rainfall. Nationwide average yield is estimated at 3.09 metric tons (mt) per hectare (ha), with notable regional variation. Yields are as low as 1.20 mt/ha in northeastern Argentina to as high as 3.74 mt/ha in the northern core region, according to the Buenos Aires Grain Exchange (BAGE).

Brazil

Severe Rainfall Slashes Soybean Yields in Rio Grande do Sul for 2024/25 Season

In Rio Grande do Sul, Brazil, soybean production for the 2024/25 season ended with a significant drop in productivity, according to data from Emater/RS-Ascar released on June 5. Despite a planted area of 6.77 million ha, average yields reached only 1.96 mt/ha, 38.43% below the initial projection of 3.12 mt/ha. Prolonged rainfall disrupted harvesting operations and damaged crops across much of the state, especially in the Bagé region, where persistent wet conditions delayed the completion of the harvest. In Dom Pedrito, where floodplain areas usually performed well during La Niña years, yields were disappointing at just 1.86 mt/ha across lowland and upland areas. The adverse weather and challenging economic context will limit post-harvest land use, as many farmers lack the resources to invest in winter crops or livestock fattening. As a result, a portion of the land may remain fallow until the summer season.

Brazil’s Soybean Acreage Expansion Slows in 2024/25 Amid Rising Costs and Export Decline

Soybean growers in Brazil have slowed their pace of area expansion. In Paraná, they planted only 4.55 million ha in the 2024/25 season, just 89% of the initial estimate and down from 94% the previous year. Meanwhile, producers in Mato Grosso, the country’s top soybean-growing state, expanded the planted area to 10.17 million ha, reaching 98% of the target and exceeding the previous season’s 8 million ha. Despite gains in some states, the overall national expansion rate has declined. Soybean exports fell 6.46% year-on-year (YoY) in May-25 and nearly 50% in Jan-25. Rising production costs, especially for fertilizers and agrochemicals, along with ongoing logistical and market uncertainties, have prompted producers to take a more cautious approach.

China

China’s Soybean Imports Surge to Record 13.92 MMT in May-25

Chinese buyers increased soybean imports to 13.92 mmt in May-25, more than doubling Apr-25’s volume, as they rushed to secure large quantities. This volume is mainly from Brazil amid fears that a renewed United States (US)-China trade conflict could raise global prices. On Apr-25, they had already raised imports by 73%. Chinese crushers booked over 40 cargoes from Brazil in early Apr-25, capitalizing on competitive prices and avoiding potential disruptions from US-origin beans. Although Brazil has overtaken the US as China’s top soybean supplier, the US still plays a vital role, with soybeans remaining the leading American agricultural export to China. Following a truce in Geneva, Beijing cut tariffs on all US goods, but existing duties on US farm products, including soybeans, still apply. US-China trade talks will resume in London, potentially reshaping future sourcing strategies.

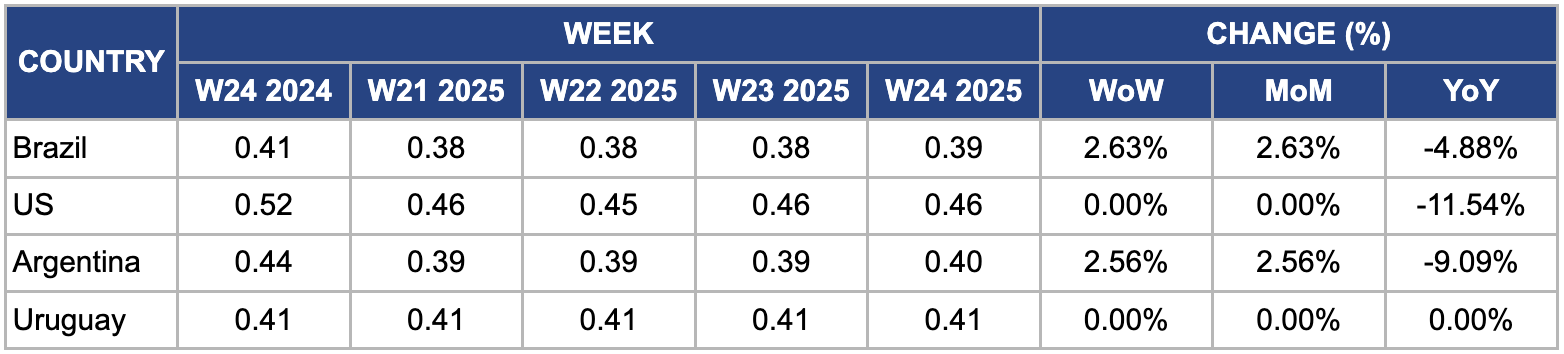

2. Weekly Pricing

Weekly Soybean Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Pricing Important Exporters (W24 2024 to W24 2025)

Brazil

In W24, Brazil’s soybean prices rose 2.63% week-on-week (WoW) and month-on-month (MoM) to USD 0.39 per kilogram (kg), driven by stronger domestic and external demand, according to the Center for Advanced Studies on Applied Economics (CEPEA). Despite firm pricing, liquidity in the national spot market remained limited as market participants closely monitored ongoing trade negotiations between China and the US. On May-25, Brazil exported 14.09 mmt of soybeans, reflecting continued international interest. However, prices declined 4.88% YoY due to ample global supply and weaker international demand. Brazil’s 2024/25 soybean output is expected to remain high, with the National Supply Company (CONAB) projecting production at 147.7 mmt, maintaining downward pressure on prices in the longer term.

United States

In W24, US soybean prices held steady WoW and MoM at USD 0.46/kg, supported by improved export activity and lingering weather concerns. The United States Department of Agriculture (USDA) reported stronger-than-expected weekly export sales, especially to key buyers like China and Mexico, which boosted market confidence. Moreover, scattered rainfall and cooler temperatures across parts of the Midwest delayed planting progress, raising concerns about potential yield impacts. While overall crop prospects remain favorable, these short-term uncertainties and improved demand provided a modest upward price.

Argentina

In W24, Argentina's soybean prices increased by 2.56% WoW and MoM to USD 0.40/kg, mainly supported by improved export activity and a slight tightening in domestic supply. While the harvest is nearing completion, with around 95% done as of early Jun-25, logistical delays due to intermittent rains in parts of Buenos Aires and Santa Fe limited immediate availability in local markets. Meanwhile, demand from key buyers like China and the European Union (EU) remained steady, particularly for soybean meal and oil, which helped lift prices. Argentina's 2024/25 soybean output will reach 48.5 mmt, similar to last year. However, lower carryover stocks kept the domestic market tighter than expected, supporting the modest price recovery in W24.

Uruguay

In W24, Uruguay’s soybean prices remained unchanged at WoW, MoM, and YoY at USD 0.41/kg, indicating a stable market environment. This price stability reflects a balanced supply-demand situation. It is underpinned by an estimated 2024/25 soybean production of around 3.5 mmt with average yields of approximately 3.2 mt/ha due to generally favorable weather conditions throughout the growing season. The export performance also remained consistent, with Uruguay exporting about 2.8 mmt of soybeans in the first half of 2025 (H1-25), primarily to China and other key Asian markets. Moreover, currency stability, with the Uruguayan peso remaining steady against the US dollar, has helped control input costs and maintain export competitiveness, reinforcing the observed price equilibrium.

3. Actionable Recommendations

Promote Investment in Drainage and Climate-Resilient Infrastructure in Southern Brazil

Prolonged rainfall in Rio Grande do Sul caused a 38% drop in soybean yield due to harvest delays and crop damage. Local governments and producer associations should incentivize investments in field drainage systems, raised beds, and post-harvest infrastructure (e.g., drying and storage units) to reduce losses from excessive moisture. These improvements would mitigate future climate-related yield risks, enhance land productivity, and allow more consistent seasonal planning.

Facilitate Targeted Export Incentives for Argentina’s Soybean Derivatives

Given Argentina’s relatively steady production and tightening domestic supply, combined with strong demand from China and the EU for soybean oil and meal, policymakers should support exporters of value-added soybean derivatives rather than just raw beans. This can be done through export credit guarantees, streamlined logistics support, and tax incentives for crushing plants, helping Argentina capture higher margins while reducing pressure on raw supply.

Enhance Brazil’s Competitive Position Amid Global Trade Shifts

With Brazil facing declining YoY soybean export volumes despite high production, exporters should diversify marketing channels beyond China and address logistical bottlenecks. This includes expanding port capacity in the North and Northeast regions to reduce dependence on overland routes, improving transparency in freight and customs processes to lower export costs, and developing digital market intelligence tools to anticipate shifts in global demand, especially as geopolitical tensions may reshape Chinese sourcing strategies. These efforts would reinforce Brazil’s global leadership in soybean exports while enabling adaptation to increasingly volatile trade patterns.

Sources: Tridge, Agrolink, UkrAgroConsult