.jpg)

In W24 in the wheat landscape, some of the most relevant trends included:

- Brazil imported 3.09 mmt of wheat from Jan-25 to May-25, the highest since 2001, driven by strong Argentine supply. Domestic demand remains stable.

- Romania forecasts a record 2025 crop following a recovery from last year's drought.

- Russia's wheat exports are expected to fall to 1.1 mmt in Jun-25 due to tighter quotas and reduced supply, while FOB prices dropped YoY amid rising costs and a stronger ruble.

- US wheat prices rose WoW in W24 due to delayed harvests and robust global demand.

1. Weekly News

Brazil

Brazil’s Wheat Imports Reached 24-Year High in Early 2025

Brazil’s wheat imports surged in early 2025, reaching 3.09 million metric tons (mmt) from Jan-25 to May-25. This is the highest volume for this period since 2001, according to data from the Secretariat of Foreign Trade (SECEX). Over the past 12 months, nearly 7 mmt entered the country, a level not seen in six years. Researchers attribute this rise to increased wheat availability from Argentina over the last two years, which has supported higher Brazilian imports. Despite the growth in inflows, domestic mills reportedly maintain adequate stocks, reducing the need for aggressive purchases during Brazil’s off-season.

Russia

Russia’s Wheat Exports Drop Sharply in 2024/25 Due to Quota Cuts and Slowing Demand

Analysts expect Russia’s wheat exports to decline sharply in Jun-25 to just 1.1 mmt, down from 2.16 mmt in May-25 and far below the 4.64 mmt exported in Jun-24. Reduced overall supply and a significantly smaller export quota than in 2024 drove the decline. From Jul-24 to May-25, Russia shipped 40.9 mmt of wheat, 10 mmt less than the 50.9 mmt exported during the same period in the 2024 season. Egypt (8.25 mmt), Turkey (3.35 mmt), and Bangladesh (2.7 mmt) remained the major buyers.

Romania

Romania Eyes Record Wheat Harvest in 2025 Amid Favorable Weather and Strong Recovery from Drought

Romania is on track for a record wheat harvest in 2025, driven by favorable weather conditions that have helped the country rebound from 2024's drought. Following severe heat and dryness in the summer of 2024 that cut yields and led to 9.29 mmt, wheat harvest was down 3.5% YoY from 2023. The 2025 season has seen regular and abundant spring rains, particularly in Apr-25 and May-25, restoring soil moisture and supporting strong crop development. The Agriculture Minister projects a harvest of 14 to 15 mmt, while market analysts forecast 13 to 13.3 mmt, surpassing the previous record set in 2021. This sharp production rebound could strengthen Romania’s position as a key wheat exporter in the European Union (EU) and Black Sea region. This may contribute to downward pressure on European wheat prices amid the broader recovery in regional output.

Ukraine

Ukraine’s Corn Exports Dropped Sharply in 2024/25 MY

As of June 9, in the 2024/25 marketing year (MY), Ukraine exported 38.51 mmt of grain and leguminous crops. This is down 24.7% YoY or 9.60 mmt compared to the same period last year, according to the Ministry of Agrarian Policy and Food of Ukraine. Wheat exports totaled 15.02 mmt, marking an 18.8% YoY decline or 2.82 mmt.

United States

Uncertain Future for US Wheat as Biofuel Policy Favors Corn and Soy

Analysts warn that the future of the United States (US) wheat belt is uncertain, as wheat growers face mounting challenges that could shift production to Canada. However, Canadian farmers may resist expanding wheat acreage due to already well-established crop rotations. The National Association of Wheat Growers (NAWG) expressed deep concern over the potential decline of the US wheat industry, drawing parallels to the loss of the oat sector. Wheat faces unique disadvantages compared to other crops, particularly its exclusion from the booming US biofuels market, which heavily supports corn and soybeans. Unlike these crops, wheat lacks the necessary sugar content to qualify for renewable fuel incentives, putting it at a competitive disadvantage.

2. Weekly Pricing

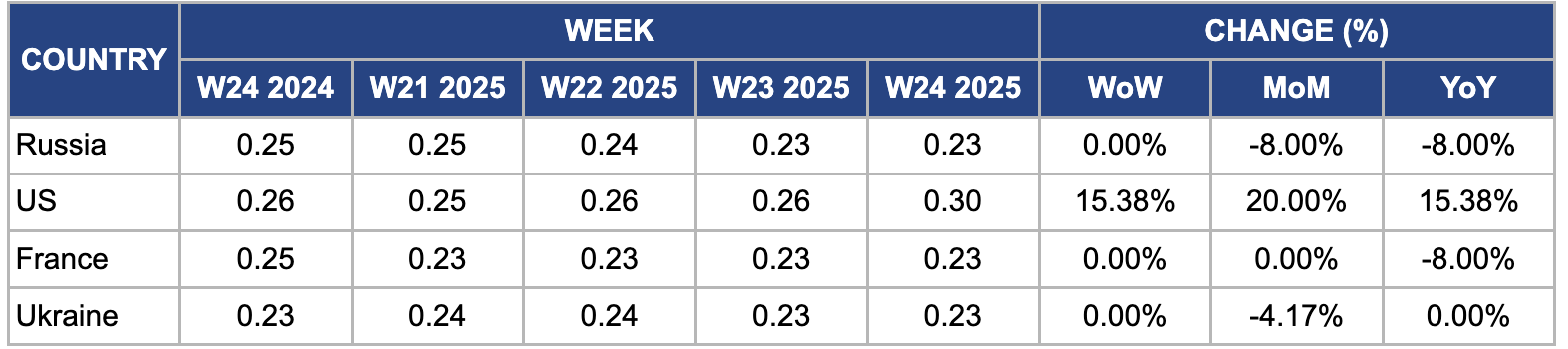

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W24 2024 to W24 2025)

Russia

In W24, Russian FOB wheat prices held steady at USD 0.23 per kilogram (kg), showing no change week-on-week (WoW) but down 8% month-on-month (MoM) and 8% YoY. The stability comes amid expectations of a record 2025 wheat harvest projected at 88 mmt, supported by favorable weather and increased planting area. Government-imposed export quotas of 10.6 mmt from Feb-25 to Jun-25 have boosted domestic supply, adding downward pressure on prices. Meanwhile, the strengthening Russian ruble (RUB) has undermined export competitiveness, and rising production and logistical costs continue to squeeze exporter margins, reinforcing the bearish tone in the Russian wheat market.

United States

In W24, US FOB wheat prices rose by 15.38% WoW to USD 0.30/kg, up from USD 0.26/kg in W23. The price surge was driven by concerns over tightening supplies due to delays in the winter wheat harvest, as wetter-than-average conditions affected key producing states like Kansas and Oklahoma. Strong global demand, with buyers turning to the US amid geopolitical uncertainties, further supported the increase. Moreover, limited export competition from other major producers facing production challenges contributed to the bullish momentum in US wheat prices.

France

In W24, wholesale wheat prices in France remained stable WoW and MoM at USD 0.23/kg, underpinned by a reduced 2024/25 production forecast of 25.78 mmt, driven by slightly lower yields of 6.15 metric tons (mt) per hectare (ha) due to adverse weather conditions. However, prices declined 8% YoY, as extra-EU exports were projected at just 3.5 mmt, the lowest in decades, reflecting weak demand from key markets like Algeria and China. Moreover, aggressive competition from major suppliers such as Russia, which continues to offer lower-priced wheat, further eroded France’s export competitiveness and added downward pressure on the market.

Ukraine

In W24, Ukrainian wheat prices held steady WoW but fell 4.17% MoM to USD 0.23/kg, driven by mounting domestic supply pressure and a seasonal slowdown in export activity. Traders accelerated efforts to offload old stocks ahead of the 2024/25 harvest, which added to the downward price trend. At the same time, ongoing logistical challenges at Black Sea ports and stiff competition from Russian and EU wheat limited Ukraine’s export potential. Market sentiment also weakened amid expectations of a stable upcoming harvest, supported by favorable weather in key producing regions.

3. Actionable Recommendations

Strengthen Brazil’s Strategic Wheat Reserve Program

Given Brazil’s record-high wheat imports in 2025 and domestic mills already holding adequate stocks, the government and milling industry should consider establishing or expanding a strategic wheat reserve program. This program would enable the purchase of surplus wheat during periods of high import availability (e.g., from Argentina) and store it for future use during off-seasons or supply shocks. This approach would reduce price volatility, enhance food security, and ensure stable flour supplies without relying on continuous imports, especially during years when neighboring exporters face production issues or shift trade priorities.

Facilitate Targeted Export Expansion for Romania’s Record Wheat Harvest

Romania should work with EU trade authorities and private exporters to secure new wheat export contracts in North Africa, the Middle East, and Asia, capitalizing on the projected record 2025 harvest. This could include promotional trade missions, government-backed guarantees, and optimizing logistics through Black Sea ports. Maximizing exports during a bumper crop year will stabilize domestic prices, support farmer incomes, and increase Romania’s footprint in global wheat markets, especially as other suppliers like Russia reduce exports due to quotas.

Develop a US Wheat Incentive Program Linked to Sustainability and Rotation Benefits

US policymakers and agricultural organizations should launch subsidies or incentive programs for wheat to counteract the decline in wheat acreage. They must emphasize wheat’s role in sustainable crop rotation and soil health and offer carbon credit eligibility or payments for including wheat in rotational systems. By actively repositioning wheat as an environmentally beneficial and economically viable crop, the US will slow or reverse the drop in wheat production and maintain its competitiveness, especially as biofuel incentives continue to favor corn and soybeans.

Sources: Tridge, AgroInvestor, CanalRural, Oil World, UkrAgroConsult