In W30 in the tomato landscape, some of the most relevant trends included:

- The reinstatement of 20.91% anti-dumping duties on Mexican tomatoes has triggered a sharp 13.93% WoW price increase to USD 1.45/kg. Compounded by severe drought in key growing regions, this policy is forcing Mexican growers to scale back plantings, with a projected 5% drop in exports and a potential 50% surge in US retail prices.

- Adverse weather is creating a divided production outlook in the Mediterranean. In Spain, intense heat has forced an early, low-quality harvest and is expected to slash processing tomato output by 23%. Conversely, Italy's processing sector is recovering with a forecast 6.2% increase in volume, while Morocco’s continues to demonstrate remarkable stability, reinforcing its position as the world's third-largest exporter.

- European prices are undergoing seasonal corrections despite underlying cost pressures. France's wholesale prices dropped 9.07% WoW to USD 1.49/kg as the market adjusted from earlier seasonal highs. Similarly, Turkey's prices saw a slight 0.58% WoW decline, balanced by peak domestic harvest and strong export demand.

- With minimal price changes and strong export growth, Morocco is proving to be a reliable supply partner for the EU and other regions. Its ability to maintain consistent output and pricing amidst global disruptions positions it as a critical player for traders seeking to mitigate risk.

1. Weekly News

Italy

Italian Processing Sector Recovers, Shifts to Premium Products

In Italy, the industrial tomato crop is expected to recover, with a forecast of 5.6 mmt, up 6.2% compared to the 2022–2024 average. This follows the start of the harvest campaign in northern Italy on July 23. Alongside the increase in volume, the sector is also undergoing a strategic shift toward higher-value items, such as premium pasta sauces and certified canned products Organic production now represents 9.1% of northern acreage, reflecting growing premium market demand.

Mexico

US Reinstates Anti-Dumping Duties

The United States (US) terminated the 2019 Suspension Agreement on July 14, 2025, reinstating 20.91% anti-dumping duties on Mexican fresh tomatoes. The 2019 Suspension Agreement was a trade deal that paused a US anti-dumping investigation into Mexican tomatoes. In exchange for not facing tariffs, Mexican exporters agreed to sell their tomatoes above a minimum reference price, a measure intended to prevent unfairly low prices in the US market.

This termination is driving Mexican growers to scale back autumn-winter plantings due to reduced investment expectations, with export forecasts down 5% to 1.96 million metric tons (mmt) for 2025. US retail prices are expected to rise by up to 50% due to tariff pass-through effects, as Mexico supplies 93% of the US’ fresh tomato imports.

Drought Constrains Production Volume

Severe drought conditions in key growing regions are compounding supply pressures. This is particularly concerning in Sinaloa, which accounts for 19% of national production. The 2025 production forecast stands at 3.10 mmt, down 3% from 2024's 3.19 mmt. Growers are increasingly seeking alternative export markets to mitigate reduced US demand.

Morocco

Strong Export Performance Continues

Morocco exported 621,000 metric tons (mt) of fresh tomatoes in the 2024/25 season, generating over USD 1.5 billion in revenue and reinforcing its position as the world's third largest tomato exporter. European Union (EU) market expansion continues, with exports growing 58.2% over the past decade. In particular, Spanish imports have risen sharply, up 34.9% year-on-year (YoY) to 31,986 mt in Q1-2025.

Spain

Extreme Heat Drives Early Harvest

In Spain, mid-30°C temperatures with peaks of 38-40°C in southern regions forced an unusually early tomato harvest starting in late June/early July. Heat stress is causing significant quality issues, including sunscald, blossom-end rot, and skin cracking, while minimal July rainfall (0-5mm) following record spring rains has created challenging growing conditions. Because of these conditions, the supply of visually perfect, undamaged tomatoes, Class I, will be severely limited. With retailers and consumers still demanding high-quality produce, the price for this top-tier segment will increase sharply. In this limited supply scenario, Class I tomatoes become a premium item.

Water Constraints Shrink Processing Output

National processing tomato output is forecast to decline 23% from 3.1 mmt in 2024 to 2.4 mmt in 2025, with Extremadura yields revised down 10% despite expanded hectares. With reservoirs at 77% capacity and water allocations tightened in drought-affected areas, irrigation capabilities are increasingly constrained.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W30 2024 to W30 2025)

Mexico

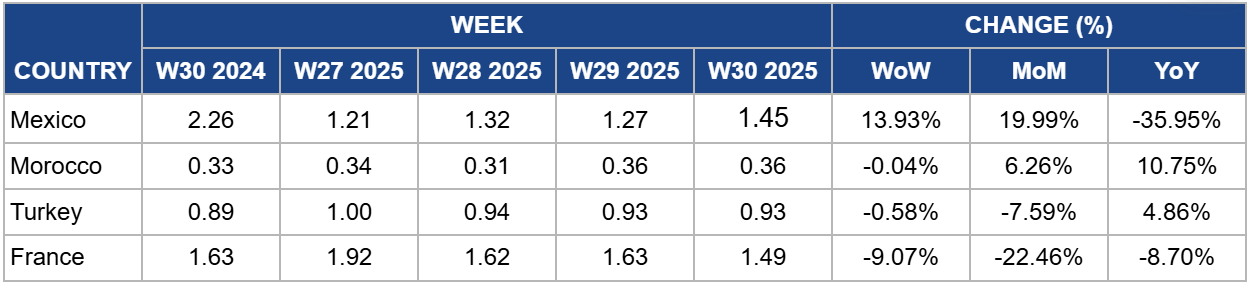

The wholesale price of fresh tomatoes in Mexico saw a significant 13.93% week-on-week (WoW) increase, climbing from USD 1.27/kg to USD 1.45/kg in W30. This surge is a direct market response to the US terminating the Suspension Agreement on July 14 and reinstating a 20.91% anti-dumping duty. The price pressure is compounded by supply-side issues, including severe drought in key regions like Sinaloa and growers scaling back planting in anticipation of the trade restrictions. This recent jump is part of a larger upward trend, with prices rising 19.99% month-on-month (MoM).

Despite these recent hikes, the price remains down 35.95% YoY. However, this significant drop is primarily explained by the high price of USD 2.26/kg recorded in W30 2024. Last year's peak was driven by its own set of severe weather events and acute trade tensions. Therefore, the current price of USD 1.45/kg, while lower than last year's anomaly, reflects a market now grappling with the new reality of US tariffs rather than a simple price collapse.

Morocco

The price of fresh tomatoes in Morocco showed remarkable stability, holding steady at USD 0.36/kg through W29 and W30 with no WoW change. This stability is notable given ongoing seasonal pressures and a domestic labor crisis, and is supported by Morocco's role as a major global exporter providing consistent, large-scale volume to the market.

Looking at the monthly trend, the price has appreciated steadily, rising 6.26% MoM from USD 0.34/kg in W27. This gradual MoM increase reflects the slow accumulation of production costs throughout the season, particularly those related to managing persistent drought conditions.

The 10.75% YoY increase, from USD 0.33/kg in W30 2024, points to more fundamental market shifts. This longer-term rise is driven by the sustained costs associated with the drought and by increased international demand for a reliable Moroccan supply, especially as other key European producers like Spain face their own climate-related disruptions.

Turkey

Looking at the monthly trend, prices have decreased by 7.59% since the beginning of Jul-25, when they were at USD 1.00/kg in W27. This month-long decline is a sign of the peak harvest's impact, as increasing domestic yields throughout Jul-25 put downward pressure on prices from their earlier highs.

However, the current price is still 4.86% YoY higher than the USD 0.89/kg recorded in the same week last year. This yearly strength indicates that underlying market conditions are more robust than in 2024. Major price drivers are higher input costs for growers and sustained demand from European importers, especially for premium varieties, which helps maintain a higher overall price floor compared to the previous year.

France

Looking at the monthly data, the price has fallen 22.46% MoM from its peak of USD 1.92/kg at W27. This steep MoM decline is due to a seasonal adjustment. As France's domestic harvest comes into full swing during Jul-25, the increased local supply puts intense downward pressure on prices, correcting them from the higher levels seen in late spring and early summer.

The current price of USD 1.49/kg is also 8.70% YoY lower than the USD 1.63/kg recorded in the same week of 2024. This implies that while prices remain seasonally elevated due to high production costs, the supply situation this year is likely more stable or abundant than it was during the same period last year.

3. Actionable Recommendations

Monitor US-Mexico Trade Impact on Global Supply Chains

With Mexican growers scaling back autumn-winter plantings due to the 20.91% US anti-dumping duties, traders should expect significant supply redistribution in Q4-2025 and Q1-2026. Similarly, rising US retail prices of up to 50% will create opportunities for alternative suppliers, including Morocco, Turkey, and greenhouse producers in the Netherlands and Canada. Traders are advised to monitor Mexican export diversification to European and Asian markets, as this could pressure existing supplier relationships and pricing structures in those regions.

Capitalize on Mediterranean Production Challenges

Spain’s tomato processing output decline and early harvest quality issues create immediate opportunities for alternative suppliers. Conversely, Italy’s production increase and France’s stable greenhouse output position these countries to capture market share. Traders should closely monitor the situation in Spain, particularly water allocation constraints in drought-affected areas and reservoir levels, as these may signal continued supply disruptions through Q3-2025.

Leverage Morocco’s Market Stability for Long-term Partnerships

Morocco’s minimal price volatility amid global disruptions, combined with export growth to the EU over the past decade, positions the country as a reliable supply partner. With stable annual export capacity and strong financial performance, traders should establish strategic relationships ahead of potential supply gaps and continued weather challenges. Focus on quality, consistency, and logistics optimization to maximize Morocco’s competitive advantages.

Sources: Tridge, USDA, WPTC, FreshPlaza, industry reports