In W33 in the soybean landscape, some of the most relevant trends included:

- China's soybean meal stocks surpassed a record 1 mmt, signaling a significant imbalance between massive imports and weak domestic demand, alongside a new long-term strategy to reduce import dependency.

- India is projected to import a record 5.5 mmt of soybean oil, a 60% YoY increase, as its price advantage over palm oil drives a massive substitution in demand from the world's largest vegetable oil buyer.

- Argentine soybean prices surged 5.00% WoW after the government announced a permanent export tax cut, a move designed to boost sales and incentivize future planting.

- A lower US crop forecast from the USDA supported global prices, with US prices rising 4.65% WoW.

- Brazil's harvest estimates were revised upwards by both CONAB and Abiove, solidifying its massive supply.

- Uruguay's prices held their recent parity with US benchmarks, a direct result of geopolitical trade shifts, even as a 26% smaller crop is forecast for the next season, posing a future supply risk.

1. Weekly News

China

China's Soybean Meal Surplus Hits Record High Amid Weak Demand

China's soybean meal inventories have surged to a historic high, exceeding one million tons for the first time. This massive surplus is a direct result of record-breaking soybean imports, which increased by 4.6% year-to-date through Jul-25, driven by the country's tariff policies. As processors convert these beans into meal, supply is far outpacing the current weak demand from the livestock sector, creating a significant market imbalance.

Despite the immense oversupply, which would typically push prices down, the market has seen a slight upward trend. This is attributed to support from the futures market, where uncertainty in global trade is strengthening domestic contracts. However, analysts warn that this situation is unsustainable. The fundamental pressure from record stocks and sluggish demand is expected to cause a price correction soon, posing a potential risk for soybean exporters who rely on the Chinese market.

China Plans to Curb Long-Term Soybean Imports, Boosting Domestic Supply

China is signaling a strategic long-term reduction in its reliance on soybean imports, aiming to decrease them to 79 million metric tons (mmt) by 2034. This shift is driven by a dual strategy: boosting domestic production through improved yields and implementing government policies to reduce soybean meal demand in animal feed.

In the interim, China is deepening its alignment with its top supplier, Brazil, through a "Soy China" initiative. This program aims to create a dedicated supply chain for soybeans explicitly produced to meet Chinese quality and sustainability standards. While imports are forecast to rise slightly in the 2025/26 season, the overarching goal is to significantly lower foreign dependency over the next decade.

India

Price Shift Drives India's Record Soybean Oil Imports

India's soybean oil imports are projected to surge by 60% to a record 5.5 mmt in the 2024/25 season. This historic shift is driven purely by price, as soybean oil has become cheaper than palm oil, which is trading at a premium. Consequently, price-sensitive Indian refiners and consumers are substituting away from more expensive alternatives. Palm oil imports are expected to fall to a five-year low, and sunflower oil imports are set to hit a three-year low. This change in purchasing patterns by the world's largest vegetable oil importer is expected to support global soybean oil prices while pressuring the palm oil market.

Ukraine

USDA Projects Record Ukrainian Soybean Harvest, Contradicting Local Estimates

The United States Department of Agriculture (USDA) is maintaining its forecast for a record-high soybean production in Ukraine of 7.6 mmt for the 2025/26 season. This optimistic outlook stands in contrast to projections from local Ukrainian analysts, who have lowered their estimates to a range of 5.8–6.5 mmt, citing adverse weather conditions. The USDA's steady forecast for Ukraine is notable as it comes at the same time the agency has reduced its overall global and United States (US) soybean production forecasts.

United States

New Study Shows Main Crop Soybeans Tolerate Higher Leaf Loss, Raising Insecticide Thresholds

New research from the North Carolina State University indicates that main crop soybeans are far more resilient to leaf damage than previously understood, tolerating up to 66% defoliation without measurable yield loss. As a result, the economic threshold for insecticide intervention has been raised from 15% to 25% leaf loss. This finding encourages a more cost-effective and sustainable Integrated Pest Management (IPM) approach, where farmers spray only when necessary, reducing costs and the risk of insecticide resistance. However, this higher threshold does not apply to more vulnerable second-crop soybeans, which retain the original 15% limit due to their shorter growing season.

US Crop Outlook and Chinese Demand Shape Market Direction

Global soybean prices are at a pivotal juncture, with market direction hinging on two key factors: the final output of the US soybean harvest and the strength of Chinese demand. A recent USDA report surprised markets by lowering its forecast for the US 2025/26 crop and ending stocks, citing a reduced yield estimate. This projection, falling below market expectations, provided immediate support to prices in Chicago and Brazil.

Looking ahead, the market will closely monitor the upcoming Pro Farmer Crop Tour, an annual US field survey that assesses crop conditions to provide independent estimates of yield and production. The tour offers a more accurate, on-the-ground evaluation of US crop potential, which could either confirm or challenge USDA's revised figures. Simultaneously, the trajectory of Chinese purchases remains a critical variable. While recent trade negotiations have sparked some optimism, significant skepticism persists regarding a substantial short-term recovery in demand from the world's largest soybean importer. The interplay between US supply realities and Chinese buying behavior will be the primary driver of price trends in the coming weeks.

2. Weekly Pricing

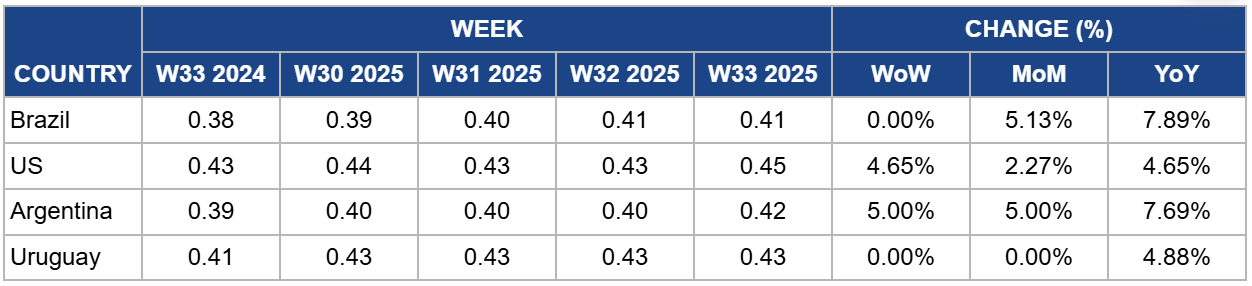

Weekly Soybean Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Pricing Important Exporters (W33 2024 to W33 2025)

Brazil

In W33, Brazilian soybean prices held steady at USD 0.41 per kilogram (kg), experiencing no week-on-week (WoW) changes. However, prices show a modest increase month-on-month (MoM) at 5.13% and a more prominent year-on-year (YoY) at 7.89%. The flat WoW performance is primarily due to producers holding back sales amidst logistical issues and tax policy uncertainty. The stronger MoM and YoY figures reflect the robust demand seen earlier in the season, particularly from China, and the underlying strength of Brazil's position as a top global supplier.

Recent data from Brazil's National Supply Company (CONAB) indicates an upward revision for the country's soybean harvest, which rose by 0.16 mmt from the previous month to a new total of 169.65 mmt in Jul-25. Similarly, the Brazilian Association of Vegetable Oil Industries (Abiove) also increased its forecast, estimating the harvest at 170.3 mmt, an increase of 0.6 mmt from its last report.

In Mato Grosso, higher prices, driven primarily by substantial port premiums, spurred a significant increase in sales for the current 2024/25 soybean harvest in Jul-25. Conversely, forward sales for the upcoming 2025/26 season remain historically slow. Despite a slight monthly price increase, the overall price level is considered unattractive by producers, causing them to delay sales commitments as they wait for more favorable market conditions.

United States

US soybean prices saw a notable increase of 4.65% WoW to USD 0.45/kg in W33. This price is also up 2.27% MoM and 4.65% YoY. The weekly price jump was attributed to a technical rebound in the futures market and short-term supply tightness as the market transitions from old to new crop supplies. For the week ending August 7, US export data showed a net reduction in old crop soybean sales by 377,610 metric tons (mt), despite new purchases from Mexico and the Netherlands.

On a brighter note, new crop sales were impressive at 1.133 mmt, with significant buys from an undisclosed destination (424,200 mt) and Mexico (251,100 mt). Still, the market's sentiment is weighed down by concerns over export demand, stemming from unresolved trade issues with the top importer, China. Despite forecasts for a large harvest, the current export pace and domestic crush demand are providing short-term price support.

Argentina

In W33, Argentina’s soybean prices experienced a strong 5% increase WoW, reaching USD 0.42/kg. This also represents a 5% MoM and 7.69% YoY gain. The sharp weekly increase is a direct result of new government incentives, including a favorable exchange rate and government tax cut on exports, which have boosted the competitiveness of Argentine soybeans on the global market and stimulated strong buying interest. The Argentine president announced a permanent reduction in the tax rate for soybeans and their by-products, a critical move as exports had been paralyzed since a temporary tax break expired on July 1. This announcement has already boosted futures prices for the upcoming 2025/26 crop. The lower tax is expected to incentivize farmer sales and stimulate planting intentions for the next season, aiming to improve the crop's profitability, which had been declining and causing some farmers to shift acreage to corn.

Uruguay

Uruguayan soybean prices remained stable WoW at USD 0.43/kg, showing no change MoM. However, prices have risen 4.88% YoY. The stability in the short term reflects a balanced market. At the same time, the annual increase is tied to the broader strength in the global soybean complex and Uruguay's ability to position itself as a reliable alternative supplier, capturing demand that might have otherwise gone to larger producers. With the ongoing US-China trade disputes, Uruguay soybean traders have more to gain, and it is expected that in the upcoming period, China's demand will grow and pressure prices up. For the next soybean campaign, Uruguay is estimated to have a slight reduction in area of 3.3% YoY, about 40,000 hectares (ha) less. However, there will be a significant reduction in expected yield, which will fall by more than 700 kg/ha, from 3,120 in this year's harvest to 2,390 kg/ha in the next, and total production will fall by approximately 26% YoY to 3.3 mmt.

4. Actionable Recommendations

Monitor US Harvest Progress and Adopt New IPM Guidelines

Buyers should closely follow the development of the US soybean crop, as unexpected weather events could affect final yields and market prices. Locking in contracts early may help hedge against potential price volatility. Meanwhile, US soybean growers are advised to implement the new Integrated Pest Management (IPM) thresholds from North Carolina State University. Main crop soybeans can now tolerate up to 25% leaf loss before economic damage occurs, allowing growers to reduce unnecessary insecticide applications, lower input costs, enhance profitability, and promote sustainable farming practices by mitigating pesticide resistance.

Track Supply Risks in Ukraine and Uruguay

Traders and buyers should closely monitor the developing harvest situation in Ukraine, where the USDA's forecasts significantly exceed local estimates due to adverse weather conditions, creating potential for supply surprises.. Additionally, while Uruguay remains a reliable supplier, forecasts indicate a 26% reduction in next season’s crop. Buyers should proactively adjust procurement strategies to hedge against potential tightening of global supply.

Leverage Argentine Export Incentives

Global buyers should consider Argentina for competitive soybean purchases following the government’s permanent export tax reduction. The policy has already elevated local prices and is intended to enhance Argentina’s attractiveness in international markets. For Argentine producers, this presents an opportunity to accelerate sales of the current crop and secure favorable terms for the 2025/26 season.

Engage Strategically with China’s Evolving Market

Exporters across all regions should maintain close engagement with Chinese buyers while adapting to China’s changing soybean strategy. Record-high soybean meal inventories indicate weak demand, and long-term policies aim to reduce imports, making volume-driven strategies risky. Exporters, particularly from Brazil, should align with initiatives like “Soy China,” emphasizing quality, traceability, and sustainability. Other exporting nations should accelerate efforts to diversify their customer base, mitigating risks from China’s push for self-sufficiency. Both established and emerging exporters can capture market share by offering reliable quality and competitive pricing as China broadens its supplier network.

Sources: Tridge, Canal Rural, Hungarian Soybean and Protein Crop Association, UkrAgroConsult