W33 2025: Sugar Weekly Update

In W33 in the sugar landscape, some of the most relevant trends included:

- Brazilian and Mexican sugar markets remain stable, with opportunities to secure medium-term contracts and hedge against currency risks.

- US and Pakistani markets face supply and policy pressures, requiring diversified sourcing and stronger logistics coordination.

- Brazilian mills are advised to balance domestic supply with export commitments to capture global demand without spiking local prices.

- Pakistani importers should leverage government allocations and forward contracts to mitigate ongoing price escalations.

- Continuous market monitoring and data-driven strategies are key to managing volatility and optimizing profitability across all markets.

1. Weekly News

Brazil

Tight Opening Stocks Collide with Strong Crush Pace

Brazil’s Center-South (CS) opened the 2025/26 season with historically tight carry-in sugar, after Wilmar, a leading global agribusiness, said the Sugarcane Industry Union’s (UNICA) mill-by-mill revision cut CS stocks at the end ofMar-25 to 1.9 million metric tons (mmt) from 4.3 mmt previously. The smaller buffer means domestic and export availability early in the season is more sensitive to any logistics or weather interruption, even as mills push high sugar mix.

Meanwhile, price action in W33 continued to key off Brazil supply headlines: market trackers flagged cumulative CS sugar output through mid-Jul-25 running below last year, with drought/heat effects cited by Brazil’s National Supply Company (Conab) earlier in the season. With global futures near multi-month lows at midweek, any confirmation of below-trend Total Recoverable Sugar (ATR) or mixed to ethanol could tighten Q4-2025 physicals.

Brazilian Sugar Eases on Strong Center–South Output and Stable Exports

Raw sugar eased to recent lows in W33 as participants concluded that Brazil’s production is more resilient than feared earlier in the year, with Center–South performance outweighing supply jitters elsewhere. That narrative limits rallies unless adverse weather trims ATR or slows field throughput.

From W33, the data thread from UNICA showed mixed fortnightly output but a higher sugar allocation, which keeps the export pipeline well supplied into late Q3-2025. Near-term, the balance hinges on sustaining dry days and maintaining high ATR. However, meaningful rainfall would quickly flip sentiment.

India

Trade Body Seeks Larger Export Window and Ethanol Diversion

With 2025/26 sugar output projected markedly higher, India’s industry is lobbying for bigger export quotas (2 mmt) and a higher diversion to ethanol (5 mmt) to avoid domestic oversupply. Industry experts state that calibrated exports plus ethanol offtake will stabilize ex-mill prices and mill cash flows through the crush.

From W32, the All India Sugar Trade Association (AISTA) reported 0.64 mmt shipped so far under this season’s limited quota, highlighting latent export capacity if permissions broaden. Export parity, and how it interacts with global prices, remains the key lever.

Ethanol Policy Momentum Continues

The Indian Sugar Mills Association (ISMA) reiterated that ethanol blending remains a “national imperative,” pushing back on mileage/engine concerns and reinforcing the program’s role in balancing the sugar market and energy policy aims. Additionally, New Delhi is working toward new blending guidelines that would lock in additional offtake for the 2025/26 crush.

An early signal on ethanol pricing and procurement volumes would let mills plan cane payments and product mix ahead of peak crush, reducing the risk of late-season price stress.

Mexico

Mexico’s Sugar Industry Eyes Gradual Production Recovery Amid Calls for Structural Reforms

Mexico’s industry briefings continue to flag a gradual production recovery into 2025/26 after last season’s weather setbacks. The government/balance-sheet view has been broadly stable month-on-month (MoM), with no disruptive policy shifts signaled.

From W33’s domestic press, the sector is still working through 2024/25 losses and advocating for structural reforms to bolster mill finances and cane productivity, factors that will shape export availability and internal pricing discipline in the coming crush.

Mexico’s Sugar Outlook Linked to US Market Conditions with Cautious Production Prospects

Mexico’s balance remains closely tied to US market conditions via suspension agreements and Tariff-Rate Quotas (TRQ) dynamics. With the US raising its stock outlook, pressure to expand Mexican shipments in the near-term looks limited, keeping domestic supply focused inward.

Any improvement in cane yields plus smoother mill uptime could lift 2025/26 production from last year’s troughs. However, execution risk, such as infrastructure and rainfall distribution, keeps planners cautious about forward export commitments.

Pakistan

Enforcement Drive Persists as Prices Stay Elevated

Pakistan's authorities maintained a nationwide crackdown on hoarding and profiteering this month to cool retail and wholesale sugar prices, which remain high in key urban centers. The campaign includes tighter monitoring at mills and along distribution channels.

From prior weeks, officials also floated targeted imports and stock audits. However, implementation pace will determine how quickly wholesale benchmarks respond, given persistent bottlenecks between mill gates and retail shelves.

Pakistan’s Sugar Market Awaits Import Clarity to Support Prices and Mill Margins

While Pakistan's policymakers have discussed import options to stabilize supplies, traders note that sentiment improvement lags announcements until physical arrivals materialize. With demand steady and supply lines uneven, price softness requires either credible import tenders or a demonstrable release of domestic stocks.

Follow-through on enforcement, plus clarity on any duty/tax treatment for potential imports, will shape Q4-2025 wholesale direction and mill margin expectations.

2. Weekly Pricing

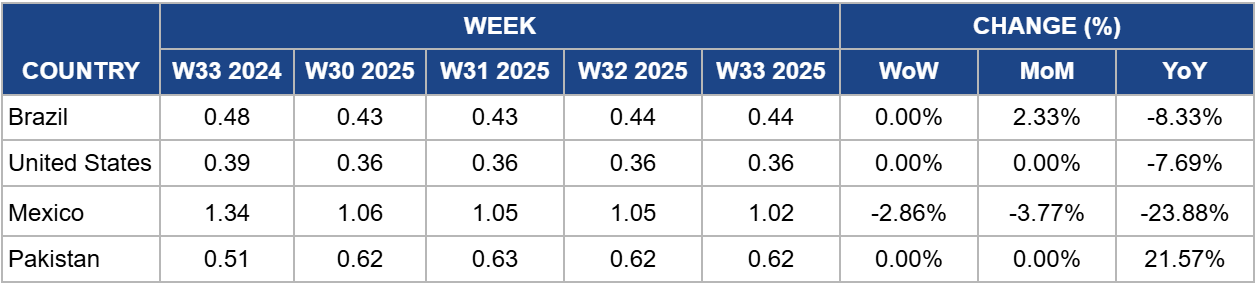

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W33 2024 to W33 2025)

.png)

Brazil

Brazil’s domestic sugar market remained flat in W33, with wholesale crystal sugar prices averaging USD 0.44/kg. This stability was driven by stronger mill activity and increased crushing volumes in the Center-South region. However, steady global demand and a relatively low stock buffer helped prevent a sharp decline, signaling that the market remains fundamentally tight despite temporary price easing.

Prices are expected to remain stable or experience slight downward pressure, especially if production momentum accelerates in line with favorable weather conditions. However, any uptick in international demand or logistical disruptions could create short-term price support.

United States

US wholesale sugar prices remained flat at USD 0.36/kg in W33, supported by the Tariff Rate Quota (TRQ) system that continues to insulate the domestic market from global price softness. The relative stability was also driven by steady industrial demand from the food and beverage sectors, which remained resilient despite weaker international benchmarks.

Wholesale prices are expected to remain stable in W34, barring any unexpected policy adjustments or shifts in global trade flows. With TRQs capping imports, domestic supply tightness will continue to support the current pricing window.

Mexico

Wholesale sugar prices in Mexico showed relative stability in W33, trading at USD 1.02/kg, down 2.86% WoW. This stability comes despite fluctuating global prices, reflecting the market’s seasonal balance and controlled distribution channels. Improved domestic output projections have alleviated some supply concerns, but persistent logistical inefficiencies and constrained export flows kept wholesale levels steady.

Prices are likely to hold steady in W34, with limited volatility expected in the absence of policy changes or weather disruptions. However, any sudden announcement related to trade adjustments, crop health issues, or transport disruptions could introduce modest upward price pressure.

Pakistan

In W33, wholesale sugar prices remained flat at USD 0.62/kg. Despite this WoW stability, prices remain elevated, up 21.57% YoY due to limited supply. Government crackdowns on hoarding and cartel activity, alongside emergency imports, have done little to ease the supply squeeze in urban centers. Limited domestic availability, combined with inefficiencies in distribution networks, has kept wholesale prices elevated, intensifying inflationary pressure on consumers and small-scale processors.

Wholesale prices are projected to remain firm or trend slightly upward in W34, unless government interventions lead to a tangible increase in available supply. However, targeted enforcement and expedited import releases could introduce minor relief by the latter half of the week.

3. Actionable Recommendations

Secure Hedging and Protect Margins

Industry players in Brazil and Mexico, where wholesale sugar prices are holding steady with only moderate volatility expected, should focus on securing medium-term contracts to stabilize margins while global demand remains supportive. Incorporating currency hedging strategies will be particularly beneficial for exporters to shield profits from exchange rate fluctuations, especially given Brazil’s exposure to currency volatility. In Pakistan, where wholesale prices continue to climb amid persistent supply constraints, importers and refiners should explore forward contracts with regional suppliers to mitigate the risk of further cost escalations and ensure more predictable cash flows.

Optimize Logistics and Diversify Sourcing

Diversifying sourcing channels and strengthening logistics operations is increasingly vital in today’s market environment. In the US and Mexico, processors dependent on domestic supply should consider expanding their supplier base to mitigate risks tied to policy adjustments, such as revisions to US tariff-rate quotas. Pakistan, meanwhile, continues to face logistics and distribution bottlenecks that amplify retail and wholesale price pressures. Strengthening collaboration with transport partners, enhancing transparency across supply chains, and quickly leveraging government import allocations could improve market efficiency and temper ongoing price volatility.

Monitor Markets and Align Strategic Planning

Producers and traders must align production and trade decisions more closely with evolving market dynamics. In Brazil, mills should maintain a balanced approach between domestic allocations and exports to capture value from steady global demand without destabilizing local markets. In Mexico and Pakistan, consistent monitoring of weather conditions, crop performance, and regulatory shifts will be essential to time bulk purchases or export contracts effectively. This disciplined, data-driven approach will enhance market responsiveness, reduce exposure to sudden price shocks, and help sustain profitability in a complex trading environment.

Sources: Tridge, Wholesale Sugar Suppliers, Daily Magazine, McKeany-Flavell, USDA, Business Insider, Yahoo Finance, Reuters, Arab News, Times of India