W33 2025: Tomato Weekly Update

In W33 in the tomato landscape, some of the most relevant trends included:

- In Europe, a severe heatwave has sent French wholesale prices soaring as the market anticipates critical supply shortages. The crisis is even more acute in Spain’s Extremadura region, where a combination of extreme weather and processor prices below production costs has devastated the crop, creating projected losses of over USD 84 million.

- Morocco is aggressively capitalizing on Europe’s supply shortfall, dropping its prices to secure a dominant share of the EU import market. At the same time, Turkey remains a stable, competitive alternative.

- North American markets are characterized by ample supply. California is experiencing a bumper crop with high yields due to favorable weather, though grower prices remain at "survival" levels.

- For Mexican exporters, a 12% WoW price rebound offers a critical window to lock in US contracts at competitive rates, despite prices remaining significantly below last year's levels.

- Rijk Zwaan, a Dutch company specializing in high-quality, innovative, climate-resilient vegetable seeds, is expanding its tomato portfolio in Asia with new R&D facilities in Japan and Vietnam. Strong performance in China and rising demand for protected-cultivation tomatoes support efforts to improve yields, shelf-life, and pest resistance.

1. Weekly News

European Union

EU Tomato Market Stable Despite Slight Dip in Summer Production

The European Union's (EU) fresh tomato market remains stable, though a slight decline in summer 2025 cultivation is anticipated amidst growing pressures. While the Netherlands experienced increased winter production due to lower energy costs, most member states expect a minor drop in summer output compared to 2024. Producers face significant challenges from rising costs, climate change, and intense competition from Moroccan imports. Despite these production hurdles, consumption within the EU is growing, primarily driven by consumer demand for cherry and specialty varieties. In Spain, for example, consumption rose 6% YoY in 2024, with cherry tomatoes becoming the most consumed vegetable.

On a positive note, after a decade of stagnation, EU tomato exports are set to increase again in 2025, mainly due to higher shipments to the United Kingdom (UK). The European Commission (EC) forecasts total EU fresh tomato production to reach approximately 5.6 million metric tons (mmt) this year.

Brazil

Tomato Prices Fall in Mato Grosso do Sul Following Increased Supply at CEASA/MS

Consumers in Mato Grosso do Sul, Brazil, are experiencing notable price declines for tomatoes this week, driven by increased supply at the Centrais de Abastecimento de Mato Grosso do Sul (CEASA/MS) market. Long-life tomato prices have fallen alongside curly lettuce, while other vegetables such as green zucchini, watermelon, and melon have seen price increases due to cold weather affecting production.

China

Rijk Zwaan Expands Tomato Innovation in Asia with New R&D and High-Tech Facilities

Rijk Zwaan, a Dutch vegetable breeding company specializing in the development of high-quality, innovative, and climate-resilient seed varieties, is strengthening its tomato portfolio in Asia with new research and development (R&D) and demonstration facilities, including a high-tech greenhouse in Japan dedicated in part to tomato development and a new R&D station in Vietnam to enhance tropical varieties. Tomatoes remain among the company's key crops in Asia, with strong performance in China supported by broad distribution through wholesalers, supermarkets, e-commerce, and foodservice. Demand is rising for high-quality, climate-resilient tomato varieties suited to protected cultivation, as growers seek enhanced yields, longer shelf-life, and resistance to pests and diseases. The company aims to leverage these innovations to support sustainable production and meet evolving consumer preferences across the Asian market.

Spain

Extreme Weather and Low Prices Devastate Extremadura's Tomato Crop

Extremadura's 2025 tomato season is facing a severe crisis, projected to be one of the worst in recent years, with estimated losses of USD 84.40 million (EUR 72.52 million). A combination of adverse weather, including spring rains that delayed planting and extreme summer heat that damaged fruit development, has caused a dramatic drop in yields. Production is expected to fall nearly 25% year-on-year (YoY), resulting in a shortfall of over 467,000 metric tons (mt) compared to contracted volumes.

Compounding the issue, the Farmers and Ranchers Union (LA UNIÓ) reports that prices paid by the processing industry are below the average production cost of USD 187.75/mt (EUR 161.32/mt), which violates Spain's Food Chain Law. The union has criticized a competing study for using unrealistic yield data that weakened farmers' negotiating power. They are now demanding an official damage assessment and financial compensation from the government, warning that the convergence of poor harvests and unfair pricing threatens the viability of many farms in the region.

United States

Abundant Yields and Modest Prices Define California's 2025 Tomato Season

California's 2025 processing tomato season is shaping up to be unexpectedly successful, driven by a "nearly perfect" mild summer with minimal pest and disease pressure. While initial forecasts predicted lower yields than in 2024, the favorable weather has produced an abundance of high-quality fruit, with some growers now concerned about managing the excess supply rather than filling contracts.

Despite the bumper crop, the financial outlook is tempered. The California Tomato Growers Association and processors agreed on a base price of USD 109 per ton, a figure described by one grower as enough to "survive" but not highly profitable. Processors have contracted 10.3 mmt, 7% below 2024’s final production, yet strong yields are expected to satisfy this demand effectively. While the season has been overwhelmingly positive so far, farmers remain cautious, as a potential late-season heatwave could still impact the final harvest.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W33 2024 to W33 2025)

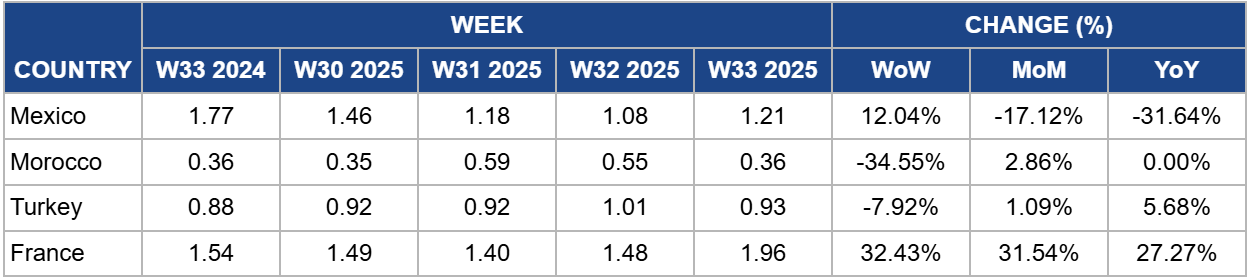

Mexico

Mexico's tomato prices increased by 12.04% week-on-week (WoW) to USD 1.21 per kilogram (kg) in W33, signaling a potential end to the price slide seen in Jul-25. This recovery is linked to a stabilization of supply after the peak harvest season and steady demand from the United States (US) market. However, the price remains down 17.12% month-on-month (MoM). It is significantly lower than the USD 1.77/kg seen this time last year, indicating that the market has not yet recovered from a broader oversupply situation that defined much of 2025. The United States Department of Agriculture (USDA) estimates that Mexico's tomato export volumes could decline by 5% YoY in 2025, potentially tightening the supply of fresh tomatoes in the US-Mexico trade and contributing to price increases in both markets. Although the wholesale price of fresh tomatoes in Mexico plummeted 31.64% YoY from USD 1.77/kg during the same period last year, market projections indicate that prices are likely to rise from this level in the coming weeks.

Morocco

In W33, the wholesale price of fresh tomatoes in Morocco experienced a sharp 34.55% WoW price drop to USD 0.36/kg. According to the latest short-term outlook for EU agricultural markets, in 2025, EU tomato production is expected to decrease by 2.6% YoY, mainly due to a decline in processing tomatoes, while fresh tomato production remains stable yet below the 5-year average. At the same time, the import volume of fresh tomatoes from Morocco is expected to increase. Morocco's tomatoes will reach an expected share of 70% of the EU's imports, with value varieties like cherry tomatoes gaining more ground in EU member states' store shelves. This surge in supply hitting the market, from peak harvesting, is aimed at capitalizing on the high prices in Europe. Morocco's tomato traders are moving large volumes quickly, even at a lower price point, to clear inventory before quality degrades. As of W33, the price is on par with the previous year, indicating this may be a seasonal, albeit sharp, correction.

Turkey

Turkey's tomato wholesale prices experienced a modest 7.92% WoW decrease to USD 0.93/kg in W33, pointing to a stable and well-supplied market. The slight dip is due to increased competition from seasonal European production, which is temporarily reducing demand for Turkish imports in some key markets. Nevertheless, Turkey gained 25% of the EU import share in 2025, second only to Morocco. Due to the prolonged season of tomato harvest in Turkey, there is a substantial supply on the market right now, which is pressuring prices down. On the other hand, price levels recorded a slight increase of 1.09% MoM and 5.68% YoY, indicating an overall stability in the market.

France

In W33, France wholesale tomato prices experienced a staggering 32.43% WoW and 31.54% MoM price increase to USD 1.96/kg as a direct consequence of a heatwave. The market is pricing in a future supply shortage, and the rush to secure high-quality produce has driven prices to a yearly high. The significant 27.27% YoY increase also suggests that underlying production costs and baseline demand in the region have been consistently more substantial than in the previous year. Despite a rising influx of tomatoes from Morocco, supply currently cannot match demand, and the low domestic supply is expected to drive prices up in the upcoming weeks as well.

3. Actionable Recommendations

Capitalize on Moroccan Tomatoes for Supply Security

With French tomato prices at a premium and supply uncertainty rising, European buyers should diversify sourcing immediately. Securing volumes from Morocco allows buyers to take advantage of significantly lower prices while benefiting from logistical proximity to Western European markets. Although Turkish tomatoes are competitively priced, Moroccan produce offers a direct and timely alternative to French and Spanish supply, helping mitigate short-term supply risks.

Secure US Contracts Ahead of Market Saturation

Mexican exporters should leverage the current WoW price rebound to actively market available inventory to US buyers, emphasizing stable supply and competitive pricing. Locking in short-term contracts can preempt potential market saturation from late-season US domestic production. Highlighting the significant YoY price deficit frames current exports as cost-effective and strategically advantageous for US importers.

Adopt a Dual Sourcing Strategy to Manage European Market Volatility

European tomato markets remain highly sensitive to weather-driven supply fluctuations. Exporters and buyers should pursue a dual approach: fulfill immediate high-value demand with remaining French stock, while pre-booking late-August to early-September shipments from Turkey to hedge against potential shortfalls. Turkish supply is stable and will play a critical role in filling gaps once the impact of the French heatwave is fully realized, ensuring continuity in supply and pricing stability.

Sources: Tridge, HortiDaily, FarmProgress, FruitNet