In W38 in the milk landscape, some of the most relevant trends included:

- A key divergence is emerging in the European dairy sector. Raw milk prices in the EU were higher in Aug-25 due to tight supply in some regions, while the prices for finished goods like butter and SMP are collapsing, putting significant pressure on processor margins.

- A combination of high inventories from Q2-2025 and a declining global butter market has sent SMP prices into a sharp decline across Western Europe. Major exporters such as Germany and the Netherlands are seeing prices fall to nearly 10% below last year's levels.

- Major players are making strategic moves to gain efficiency and market power. Lactalis and Sodiaal are investing over a billion dollars in modernizing their French operations, while the FrieslandCampina-Milcobel merger continues to move forward.

- The downturn in the conventional dairy market is contrasted by strong growth in high-value niches. The UK organic milk sector is sustaining double-digit YoY growth, and food-tech startups creating dairy and fat alternatives are securing significant investment.

1. Weekly News

Europe

EU Raw Milk Prices Inch Higher in August, but Weak Butter Market Caps Gains

The average raw milk price in the European Union (EU) registered a modest increase in Aug-25, rising 0.8% from Jul-25 to USD 0.58 per kilogram (kg) (EUR 0.53/kg), driven by tightening milk supplies in key producing nations. This contributed to a 12% year-on-year (YoY) price increase. Reduced milk production in major exporters like Germany, the Netherlands, and France created upward pressure on farmgate prices, with Belgium experiencing the most significant monthly increase of 9.9%. However, analysts suggest a substantial price rally is unlikely. The primary limiting factor is the sharp downturn in the global butter market, which has historically been a key driver of milk price increases. With butter prices falling due to increased global supply from regions like New Zealand and the prospect of additional duty-free butter imports from the United States (US), the upside for the broader dairy complex is now severely constrained, preventing a significant pass-through of higher farmgate prices to commodity products.

EU Dairy Supplies Built Up in Q2-2025 on Stable Milk Flow and Weak Export Demand

Available supplies of butter, cheese, and milk powders in the EU increased in Q2-2025, as a marginal 0.06% rise in milk production was compounded by a 2.7% decline in total exports. Cheese stocks grew as a decline in exports, caused by comparatively high EU prices and weaker demand from the Middle East and North Africa (MENA) region, the US, and China, offset modest gains in production and imports. For butter, available supplies were boosted as higher domestic production and increased imports negated the impact of strong export volumes. In the powders category, skim milk powder (SMP) supplies rose by 5.5% YoY, driven by a matching 5.5% increase in production. Meanwhile, whole milk powder (WMP) inventories swelled by a substantial 20.5%, a direct result of poor price competitiveness that led to a significant decline in export demand, causing more product to remain within the EU. According to the latest short-term outlook, the European Commission (EC) expects milk deliveries to remain stable in 2025 (+0.15% YoY). The decline in the dairy herd size will be balanced by the increase in milk yields (+1.2%) in combination with improving milk fat (+0.2%) and protein (+0.1%) content.

EU-Mercosur Trade Deal Divides European Agricultural Sector

The adoption of the new EU-Mercosur Free Trade Agreement (FTA) has elicited a sharply divided response from Europe’s agricultural sector, pitting the specialized interests of the dairy industry against the broader concerns of the general farming lobby. The European Dairy Association (EDA) has strongly welcomed the deal, highlighting a significant market access victory. The agreement will increase the tariff-free quota for EU cheese exports to the Mercosur bloc tenfold, to 30,000 mt, a move the EDA believes will foster a more resilient and globally competitive dairy sector. In stark contrast, the EU’s main farming organization, Copa-Cogeca, has urged the European Parliament to reject the agreement. They warn that the deal poses a threat of unfair competition, citing significant disparities in production and sustainability standards between the two blocs and arguing that the proposed safeguards for European farmers are vague and unenforceable.

Belgium

Milcobel and NoPalm Ingredients Partner to Create Palm Oil Alternative from Dairy Byproduct

Belgian dairy cooperative Milcobel has entered into a strategic partnership with biotech startup NoPalm Ingredients to produce a sustainable palm oil alternative by upcycling a dairy byproduct. Under the agreement, Milcobel will supply whey permeate, a sidestream from its cheese production, to NoPalm Ingredients. The startup will then use its proprietary fermentation technology to convert this whey permeate into high-value oils and fats that can replace palm oil in food and non-food applications. This collaboration allows Milcobel to valorise a low-value sidestream into a new revenue source while advancing its circularity and sustainability goals. For NoPalm, the deal secures a stable feedstock for its demonstration factory, set to open in 2026, and includes a feasibility study to co-locate its first commercial factory at Milcobel’s Langemark site by 2028. The partnership is a key example of how the traditional dairy industry can collaborate with biotech to create a more resilient and sustainable food system.

France

Sodiaal Secures USD 75.6 Million EIB Loan for Innovation and Sustainability

Sodiaal, France's largest dairy cooperative, has secured a USD 75.6 million (EUR 70 million) loan from the European Investment Bank (EIB) to finance its research, development, and innovation strategy from 2025 to 2028. The investment, backed by the EU's InvestEU programme, is designed to make the dairy sector greener by cutting carbon emissions, reducing plastic packaging, and lowering water consumption. For Sodiaal, which owns major brands like Yoplait and Entremont, the funds will strengthen the competitiveness of its 8,000-member dairy farms, and more than 14,500 member farmers in a rapidly changing global market. This is the second EIB loan granted to the cooperative, signaling a long-term partnership focused on helping Sodiaal navigate strong international competition and adapt to new consumer expectations, positioning sustainability and profitability as intertwined strategic goals for the future.

Lactalis Announces USD 1.18 Billion Investment to Modernize French Operations

French dairy giant Lactalis has announced a significant USD 1.18 billion (EUR 1 billion) long-term investment program to modernize its 69 domestic manufacturing sites by 2030. The capital expenditure is earmarked for three primary areas: upgrading production equipment, fostering product innovation, and accelerating the company's decarbonisation efforts to reduce its environmental footprint. This move comes as the French dairy market navigates significant challenges, including stricter environmental constraints and intense international competition. Despite these pressures, Lactalis reported a 1.4% increase in its domestic sales volumes in the first half of 2025, outperforming the national market. The company's investment signals a proactive strategy to solidify its market-leading position and enhance the efficiency and sustainability of its operations for future growth.

Netherlands

Dutch Startup Secures USD 2.3M to Commercialize Sunflower-Based Dairy Fat Alternative

Dutch food-tech startup Time-Travelling Milkman has secured USD 2.3 million (EUR 2 million) in pre-Series A funding to commercialize its innovative dairy fat alternative, Oleocream. Developed as a spin-off from Wageningen University, Oleocream is created through a patented process that uses only sunflower seeds and water, preserving the seeds' natural oleosomes to produce a creamy texture that mimics traditional dairy fats. The ingredient is positioned as a clean-label solution to replace not only dairy fats but also unsustainable tropical fats like palm and coconut oil, providing a timely alternative for manufacturers facing the upcoming EU deforestation regulation. The new capital will enable the company to scale up production and launch its own line of next-generation cream cheeses and desserts, while also supplying Oleocream as an ingredient to the burgeoning plant-based and hybrid dairy sectors. Time-Travelling Milkman's Oleocream can directly complement the traditional dairy sector by enabling the creation of innovative hybrid products that blend dairy with plant-based fats. With production scaling to 1,000 mt a year, the startup is positioned to supply commercial volumes, allowing dairy companies to reduce the animal fat content in products like cream cheese and desserts to appeal to flexitarian consumers. This partnership offers the dairy industry a pathway to enhance sustainability and meet evolving consumer demands for cleaner, blended food options.

United Kingdom

UK Milk Production Maintains Strong YoY Growth Trend

Milk production in Great Britain continues to demonstrate a strong YoY growth trend, with daily deliveries for the week ending September 20 running 5.7% higher than the same period in 2024. According to the latest data from the Agriculture and Horticulture Development Board (AHDB), deliveries also increased by 1.3% compared to the previous week, maintaining solid production volumes as the autumn season progresses. This strong performance builds on the consistent growth seen throughout the summer, with total United Kingdom (UK) production for Aug-25 estimated at 1,262 million liters. The sustained high level of milk flow provides an ample supply of raw material for the UK's dairy processors, reinforcing their competitive position for exports. However, this robust production also continues to contribute to the well-supplied European market, adding to the broader structural oversupply that is currently exerting downward pressure on global dairy commodity prices.

GB Organic Milk Production Sustains Double-Digit YoY Growth

The organic milk sector in Great Britain continues to demonstrate exceptional growth, with daily deliveries for the week ending September 20 holding steady at 12.0% above the levels of the same period last year. This sustained double-digit YoY increase is supported by a significant 4.9% rise in volumes compared to the previous week, indicating strong ongoing production. According to the AHDB, this performance builds on a remarkable 12.2% increase in organic milk volumes for the financial year to date (since Apr-25). The consistent and substantial expansion of the organic milk pool signals robust consumer demand that appears insulated from the broader downturn in the conventional dairy market. This provides a clear growth opportunity for processors, offering a reliable and expanding supply of high-value raw material to develop and market premium organic dairy products.

2. Weekly Pricing

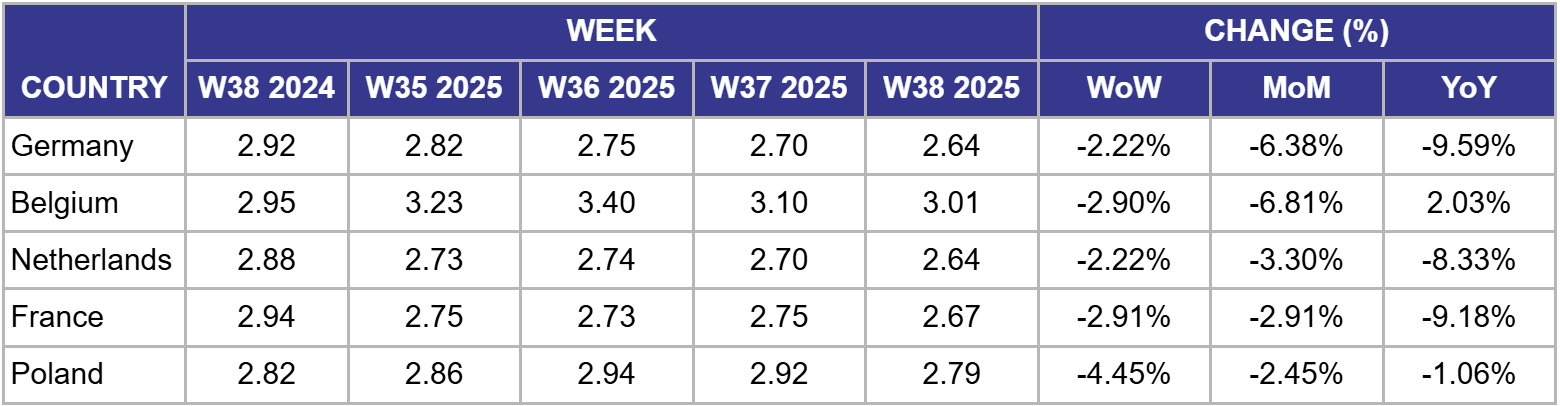

Weekly Powdered Milk Pricing Important Exporters (USD/kg)

* Varieties: Skim Milk Powder (SMP)

Yearly Change in Powdered Milk Pricing Important Exporters (W38 2024 to W38 2025)

* Varieties: SMP

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

Germany

In Germany, the price of SMP was USD 2.64/kg in W38, continuing its decline by 2.22% week-on-week (WoW) and 6.38% month-on-month (MoM), which deepened the YoY drop of 9.59%. The German SMP market remains in a steep downturn, with prices falling across all timeframes. The market is being overwhelmed by bearish factors, primarily the spillover weakness from the collapsing European butter market and high inventory levels for dairy commodities such as milk powder reported in Q2-2025. As a major export hub, Germany is highly exposed to the weak international sentiment, and the well-supplied European market continues to exert significant downward pressure on prices, pushing them to substantial lows compared to the previous year.

Belgium

In Belgium, the price of SMP was USD 3.01/kg in W38, a decrease of 2.90% WoW and 6.81% MoM. This has reduced the YoY gain to 2.03%. The Belgian market continues to correct downwards from its recent highs, with the negative WoW and MoM figures indicating that bearish European sentiment is now the prevailing market driver. Although Belgium saw the EU's sharpest rise in raw milk prices in Aug-25, this cost-push factor has failed to support SMP prices. The market is instead being dragged down by the broader collapse in the European butter market and high continental stock levels. The premium for Belgian SMP is rapidly eroding as it realigns with the lower prices in neighboring countries. This price correction is occurring despite a 16% decline in SMP production in Belgium between Jan-25 and Aug-25.

Netherlands

In the Netherlands, the price of SMP was USD 2.64/kg in W38, declining by 2.22% WoW and 3.30% MoM, extending the YoY decline of 8.33%. The Dutch market continues to weaken, with prices falling in line with the broader European trend. Despite reports of tighter domestic milk supplies and higher farmgate prices in Aug-25, these bullish fundamentals are being completely negated by the severe downturn in the finished goods markets. The price is being pressured by the combination of high European dairy inventories reported for Q2-2025 and the significant price weakness in the butter market. The deepening negative YoY figure confirms that these powerful bearish factors are dictating the market's direction.

France

In France, the price of SMP was USD 2.67/kg in W38, falling 2.91% WoW and 2.91% MoM, which pushed the YoY comparison to a 9.18% drop. After a minor bounce last week, the French market has resumed its sharp decline, aligning with the bearish trend across Western Europe. The identical WoW and MoM decreases highlight the rapid pace of the recent downturn. This price weakness is being driven by the dominant negative sentiment across the continent, stemming from the collapse in butter prices and high dairy commodity stocks.

Poland

In Poland, the price of SMP was USD 2.79/kg in W38, a sharp decrease of 4.45% WoW and 2.45% MoM. This has caused the price to flip to a negative 1.06% YoY comparison. The Polish market has experienced a major reversal, with the recent price rally coming to an abrupt end. The sharp WoW drop indicates that the bullish effect of strong regional demand has been completely overwhelmed by the pan-European market collapse. The pronounced weakness in the butter market and high inventories across the continent are now forcing Polish prices down. The flip to a negative YoY figure is the most significant development, showing that Poland is no longer an outlier and has rejoined the broader bearish trend affecting the entire EU.

3. Actionable Recommendations

Combat the Margin Squeeze by Upcycling Byproducts

The current European market is squeezing processor margins between high raw milk costs and collapsing commodity prices. To counter this, European dairy processors should look beyond primary products and invest in valorizing their sidestreams. The partnership between Milcobel and NoPalm Ingredients, which turns low-value whey permeate into a high-value, sustainable palm oil alternative, is a prime example of this strategy. By identifying byproducts and collaborating with biotech or food-tech innovators, processors can create new, high-margin revenue streams that are not tied to volatile commodity cycles. This circular economy approach not only improves profitability but also enhances a company's sustainability credentials, attracting environmentally conscious partners and customers.

Tap into High-Growth Niches with Organic and Hybrid Products

While the global conventional dairy market is oversupplied, niche categories are thriving. The UK organic milk sector's sustained double-digit growth indicates strong, insulated consumer demand that can support premium pricing and serves as a prime example. Dairy brands should see this as a clear signal to diversify their portfolios. This means either launching dedicated organic lines to capture this proven market or innovating with hybrid products, as seen in the Netherlands. Blending traditional dairy with innovative plant-based ingredients, like the sunflower-based fat from Time-Travelling Milkman, can appeal to the growing number of flexitarian consumers, offering a path to growth even when the core market is weak.

Sources: Tridge, AHDB, Green Queen, Just Food, European Commission, Food & DrinkTechnology, Feed Strategy, Association of Milk Producers