.jpg)

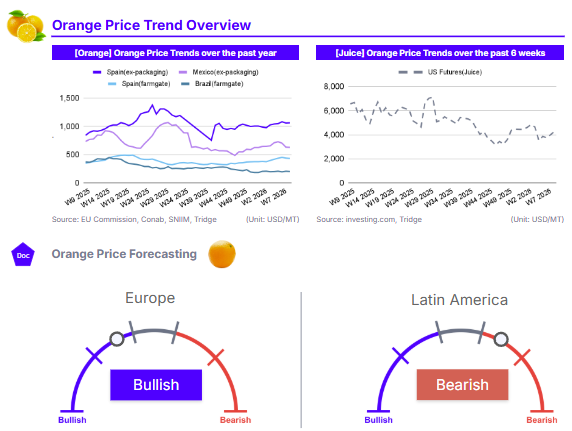

As of W9 2026, global orange prices exhibited sharp gains in US Futures contrasting with softening physical markets in Latin America and Europe. US Orange Juice Futures surged to USD 4,277.0/mt (+6.89% WoW), rebounding from early Feb-26 lows. Conversely, Brazil’s farmgate price fell to USD 201.6/mt (-2.20% WoW) as the harvest winds down, while Mexico’s ex-packaging price dipped to USD 629.0/mt (-0.54% WoW) due to weather-induced quality issues. In Spain, farmgate prices declined to USD 432.9/mt (-1.33% WoW) following supply pressure from Egypt and Morocco. Long-term analysis shows prices in Brazil and the US remain significantly lower YoY due to recovering 2025/26 production and high inventories. However, Spain maintains a strong bullish trend (+25.16% YoY) driven by a projected 9.72% seasonal production shortfall. With Brazilian orange juice inventories up 75.4% by late 2025 and European production hitting structural lows, buyers should prioritize Brazilian sourcing for juice while targeting the EU market for fresh fruit exports.

1. Weekly Price Overview

US Futures Surge as European and Latin American Markets Soften

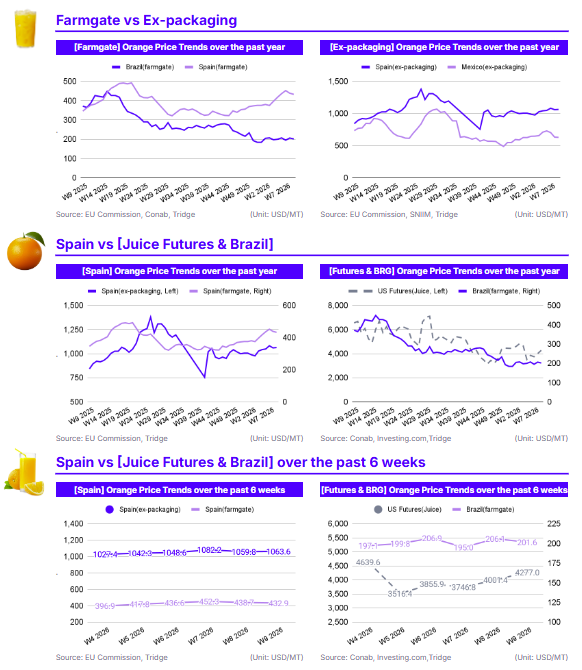

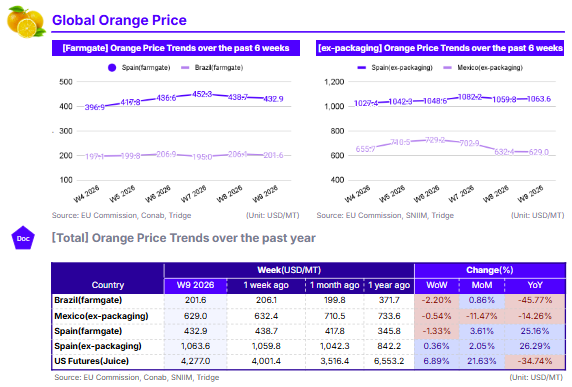

In the United States (US), Orange Juice Futures jumped 6.89% week-on-week (WoW) to USD 4,277.0 per metric ton (mt). This spike is a sharp rebound from early Feb-26 dip and is driven primarily by short-term speculative trading rather than changes in domestic production. Foreign supplies are also sufficient exemplified by Brazilian orange juice inventories being up 75.4% at the end of 2025. Brazil’s farmgate price fell 2.20% WoW to USD 201.6/mt. This decline is seasonal as the citrus belt harvest winds down and late-season varieties underperform, cooling domestic pricing as the primary window closes.

Mexico’s ex-packaging price dipped a marginal 0.54% WoW to USD 629.0/mt. Prices remain pressured by inconsistent fruit quality, a lingering result of delayed harvests and damage caused by tropical storms Raymond and Priscilla. In Spain, farmgate prices fell 1.33% WoW to USD 432.9/mt, while ex-packaging prices rose 0.36% to USD 1,063.6/mt. The farmgate drop stems from increased competition and supply pressure from Egypt and Morocco, which has temporarily neutralized the upward pressure of Spain's projected 9.72% seasonal production shortfall.

2. Price Analysis

Structural Deficits in Europe Contrast with Stabilizing Global Supply

In the US, Orange Juice Futures rose 21.63% month-on-month (MoM) to USD 4,277/mt, although they remain 34.74% lower year-on-year (YoY). Similarly, Brazil’s farmgate price reached USD 201.6/mt, up a marginal 0.86% MoM but down a significant 45.77% YoY. The massive YoY declines in both countries highlight the continued stabilization of global supply following the 2024 production crisis. Brazil’s 2025/26 crop is forecast at 13.5 million metric tons (mmt), a 3.7% increase from previous estimates, which has established a cheaper global baseline compared to the previous year. While US Futures saw a sharp MoM recovery, this is viewed as a short-term speculative trading coupled with a technical correction, as high Brazilian inventories, which rose 75.4% by late 2025, continue to provide a bearish long-term ceiling for juice prices in the Americas.

In Spain, prices showed consistent long-term strength, with farmgate prices up 3.61% MoM and 25.16% YoY to USD 4,32.9/mt, while ex-packaging prices rose 2.05% MoM and 26.29% YoY to USD 1,063.6/mt. This surge reflects a structural deficit in the Northern Hemisphere. The World Citrus Organisation (WCO) projects Spanish production to drop 9.72% this season to 5.59 mmt, which is 11.20% below the four-year average. This local shortage, exacerbated by adverse weather in early 2026, keeps European prices elevated despite growing competition from Egypt and Morocco.

Mexico’s ex-packaging price fell 11.47% MoM and 14.26% YoY to settle at USD 629.0/mt. This downward trend is primarily a result of quality issues rather than abnormally high volume. Heavy rains from tropical storms Raymond and Priscilla delayed the harvest and impacted fruit consistency, forcing prices downward despite a projected 0.4% decrease in total citrus production for the 2025/26 market year. Consequently, Mexico’s price movement diverges from Spain's upward trend, as poor fruit quality in Mexico offsets the impact of marginally lower production.

3. Strategic Recommendations

Leverage High Brazilian Orange Juice Inventories and Estimated Production

Global orange juice processors and beverage manufacturers should prioritize sourcing from Brazil to capitalize on significantly improved liquidity and a normalized supply environment. Following the extreme supply crunch of 2024, the Brazilian market has seen a significant recovery, with orange juice inventories rising by 75.4% by the end of 2025. This stockpile provides a critical buffer against short-term price spikes, such as the 6.89% week-on-week (WoW) surge recently observed in US Futures. With the USDA forecasting orange juice production in Brazil at 1.03 mmt in 2026, up 1.86% YoY, the production outlook remains robust despite the 2025 harvest season winding down. By leveraging Brazil’s high inventory levels, importers can achieve cost stability and avoid the speculative volatility currently characterizing the North American futures market.

Target European Markets to Fill Structural Supply Gaps in Fresh Oranges

Fresh orange exporters and global traders should direct shipments toward the European Union (EU) to capitalize on a structural deficit across major producing countries. According to the WCO, Spanish production is projected to decline by 9.72% this season, falling 11.20% below the five-year average. This trend is mirrored across the Mediterranean, with total Northern Hemisphere citrus production expected to drop significantly compared to previous seasons. Spain's farmgate prices have already surged 25.16% YoY to USD 432.9/mt, signaling strong domestic demand that local supply cannot meet. While North African origins like Egypt and Morocco have begun filling this gap, the persistent production lows in Spain, Italy and other European hubs create a high-value opportunity for Southern Hemisphere and North American exporters. Exporters should focus on high-quality fresh fruit to compete with regional imports. Given the 26.29% YoY increase in ex-packaging prices in Spain, the European market remains a lucrative destination for fresh citrus despite the arrival of competitive Mediterranean volumes.