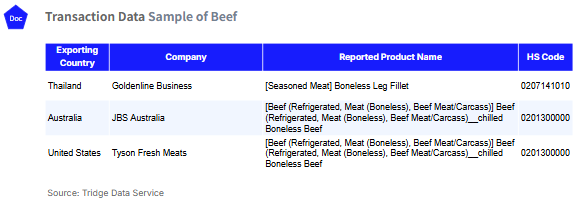

W8 2026: Beef

In the EU, prices remain high due to structural factors such as herd contraction, rising feed and energy costs, and environmental regulations that limit rapid expansion, even though short-term fluctuations reflect minor adjustments in supply and demand. In Brazil and Argentina, prices are rising as strong export demand, particularly from Asia and China, coincides with tighter domestic cattle availability and ongoing herd management or rebuilding efforts. In the US, beef prices are supported by historically low cattle inventories following prolonged droughts, maintaining bullish futures and elevated retail prices, while government import quotas provide temporary supply relief. Australia is experiencing downward pressure on beef prices due to high female slaughter rates. Overally, global beef markets are expected to remain volatile in 2026 as rising demand driven by population growth and increasing protein consumption in middle-income and developing economies coincides with tightening supply across major producing regions. Looking ahead, stakeholders should adopt region-specific strategies to navigate market volatility. EU producers should focus on efficiency and herd management, Brazil and Argentina on exports and market access, and the US and Australia on herd rebuilding and targeted live exports.

1. Weekly Price Overview

Global Beef Prices Remain Elevated Amid Tight Supply and Strong Demand

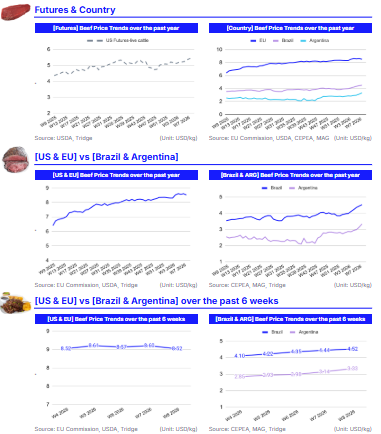

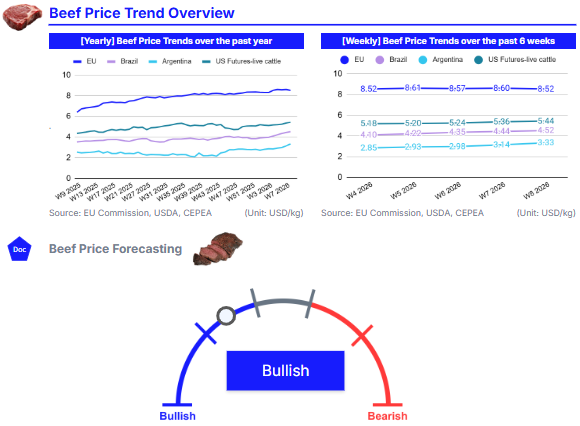

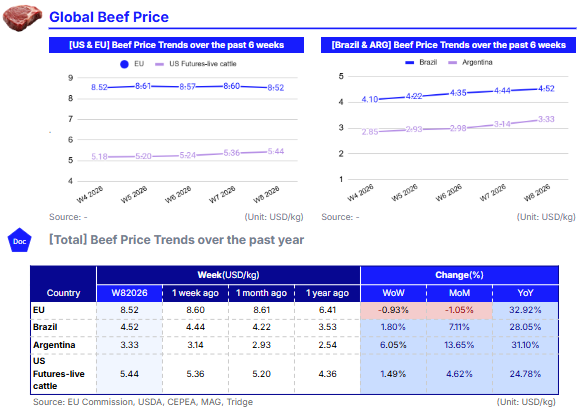

In W8, beef prices in the European Union (EU) averaged USD 8.52 per kilogram (kg), declining by 0.93% week-on-week (WoW) and 1.05% month-on-month (MoM), while remaining significantly higher by 32.92% year-on-year (YoY). The modest weekly decline likely reflects temporary supply increases or a short-term normalization in demand following strong purchasing activity earlier in the year. Despite this weekly easing, prices have remained relatively stable, fluctuating within a narrow range of approximately USD 8.52/kg to USD 8.61/kg since W4. This sustained price level highlights the underlying tightness in the market. On an annual basis, the sharp increase continues to be driven by structural factors, including ongoing herd contraction across the EU, elevated feed and energy costs in recent years, and stringent environmental regulations that limit rapid expansion in cattle production.

In Brazil, prices rose to USD 4.52/kg, increasing 1.80% WoW, 7.11% MoM, and 28.05% YoY. The rise could be attributed to the expectation of a fall in production in 2026, with the United States Department of Agriculture (USDA) estimating a fall of 5.3% YoY to 11.7 million metric tons (mmt). The upward trajectory is also largely supported by strong export demand, particularly from Asia, and tighter cattle availability following earlier herd liquidation cycles. The sustained YoY growth highlights Brazil’s stronger positioning in global beef trade flows amid constrained global supply.

Argentina’s beef prices reached USD 3.33/kg, up 6.05% WoW, 13.65% MoM, and 31.10% YoY. The rise suggests tightening domestic cattle supply, potentially due to herd rebuilding efforts and strong export pull, particularly from China. Domestic inflationary pressures and currency adjustments may also be contributing to nominal price increases.

In the United States (US), live cattle futures averaged USD 5.44/kg, rising 1.49% WoW, 4.62% MoM, and 24.78% YoY. The continued strength in futures prices reflects historically low cattle inventories after prolonged drought-driven herd reductions. Market expectations of tighter beef production in 2026, combined with resilient consumer demand and stable retail beef pricing, have maintained bullish sentiment in the futures market.

2. Price Analysis

Global Beef Markets Face Volatility in 2026 Amid Tight Supply and Rising Demand

Global beef markets are expected to remain volatile in 2026 as demand continues to grow while supply tightens across several major producing regions. Global demand is projected to increase due to population growth and rising protein consumption in middle-income and developing economies. At the same time, global supply is forecast to decline slightly, with the US, New Zealand, and Europe reporting lower production compared to the last five-year average.

The US cattle herd has fallen to its lowest level in more than 70 years, supporting strong demand for imported beef, particularly lean trimmings used in ground beef. Consumer prices in the US remain elevated, with ground beef averaging a record USD 6.69 per pound (lbs) in Dec-25, while total beef imports are rising. In response to tight domestic supply, the US government temporarily increased its beef import quota by 80,000 metric tons (mt) in 2026, allocated to Argentina in four quarterly tranches of 20,000 mt each.

Brazil is emerging as a critical driver of global beef market dynamics after overtaking the US as the world’s largest beef producer in 2025. Brazilian exports to China are expected to fall due to a safeguard tariff-rate quota of 1.1 mmt, prompting exporters to redirect shipments to the US, Southeast Asia, and the Middle East. Brazil has also expanded market access in Indonesia and Vietnam and recently obtained certification from the World Organisation for Animal Health (WOAH) as a country free of foot-and-mouth disease (FMD), raising the possibility of future access to Japan and South Korea. Meanwhile, Argentina and Uruguay are expected to increase exports in 2026 due to higher Chinese import demand and larger quota allocations relative to their 2025 shipment levels.

In Australia, beef production is forecast to decline by 6% YoY to 2.6 mmt due to low-er slaughter levels despite slightly higher carcass weights. The national herd is expected to fall by 3% YoY in 2025/26 due to high female slaughter rates in Victoria and New South Wales before stabilizing at around 27 million heads in 2026/27, representing a 1% YoY decline. Export volumes are projected to fall by 8% YoY to 1.5 mmt in 2026, although Australia is still expected to export 82% of its total beef production in 2025/26. Live cattle exports are forecast to increase by 1% YoY to 784,000 heads, while average export prices are expected to decline by 3% YoY to USD 1,180 per head amid weaker Indonesian demand and a depreciating Indonesian rupiah.

3. Strategic Recommendations

Strategic Exports and Price Management Vital for Global Beef Competitiveness in 2026

In the EU, where prices remain elevated at USD 8.52/kg to USD 8.61/kg due to structural herd contraction, EU producers should focus on cost efficiency and herd management. This could include targeted feed optimization, sustainable production practices to comply with environmental policies, and strategic slaughter scheduling to balance supply without exacerbating price volatility. Processors and retailers may benefit from securing longer-term supply contracts to hedge against short-term fluctuations while exploring alternative sourcing from regions with more flexible production.

In Brazil and Argentina, where prices are rising, market participants should capitalize on strong export demand, particularly from Asia and other high-growth markets. Exporters can focus on expanding market access, diversifying buyers to mitigate risks associated with China’s quota policies, and optimizing logistics to ensure consistent supply to high-demand regions. Producers should also consider herd expansion and efficiency improvements, given Brazil’s rising global influence and Argentina’s ongoing herd rebuilding, to maintain competitiveness and maximize export revenues while managing domestic supply constraints.

For the US and Australia, strategic planning is critical in light of tight supply and volatile global demand. In the US, stakeholders should leverage import quotas effectively while investing in herd rebuilding to ensure long-term market stability. In Australia, actions such as improving feed efficiency, selectively managing female slaughter rates, and targeting live cattle exports to markets like Indonesia, where volume growth is projected despite weaker prices, can help maintain profitability.