In W7, EU WMP saw a slight weekly increase but remained under pressure MoM and YoY, while SMP rose modestly, supported by steady demand from food manufacturers and exports to Southeast Asia and the Middle East. Oceania WMP and SMP strengthened due to tighter inventories and seasonal milk tapering, whereas South American WMP and SMP remained stable, reflecting balanced regional supply-demand conditions. Overally, global milk powder markets gained from early Jan-26 on short-term liquidity tightening, with EU and Oceania WMP showing moderate upward movement and GDT auction recording notable price gains for upcoming deliveries. Despite these short-term gains, EU WMP production declined, exports fell, and overall prices remained below long-term averages amid high global milk supply. Stakeholders are recommended to focus on flexible short-term procurement, diversify sourcing, stagger deliveries, and employ risk management tools to navigate volatility and optimize WMP and SMP value.

1. Weekly Price Overview

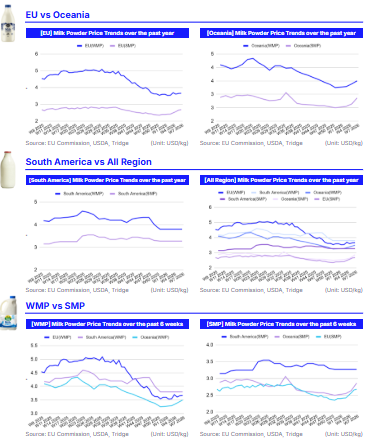

Seasonal Tightening and Steady Demand Support Global Milk Powder Markets

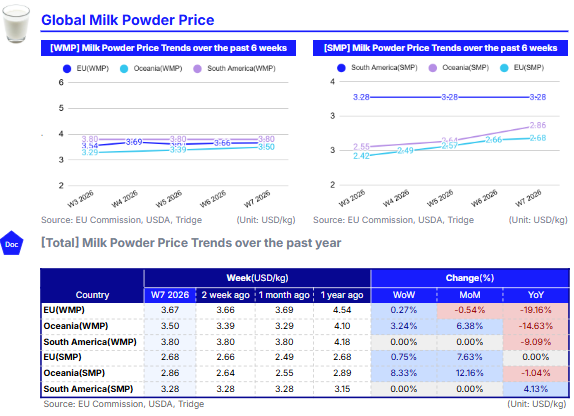

In W7, whole milk powder (WMP) prices in the European Union (EU) averaged USD 3.67 per kilogram (kg), rising by 0.27% week-on-week (WoW) but declining 0.54% month-on-month (MoM) and falling by 19.16% year-on-year (YoY). The slight weekly uptick suggests short-term tightening linked to winter-season milk moderation, while the monthly and annual declines indicate continued structural pressure from comfortable inventories, subdued Chinese restocking, and intensified competition from Oceania.

Oceania’s WMP rose to USD 3.50/kg, up 3.24% WoW and 6.38% MoM, though still 14.63% below last year’s level. The weekly rise is attributed to inventories tightened and seasonal milk production tapered. Output remained steady to lighter, reducing availability and supporting higher prices.

South America’s WMP remained unchanged at USD 3.80/kg since W52, reflecting balanced regional supply-demand conditions and limited spot market volatility. Demand is holding steady compared with previous weeks. Import demand from Brazil remains strong while demand from the African continent and other locations has dwindled recently. Production of WMP increased in several countries with Argentina leading the way.

Meanwhile, EU skim milk powder (SMP) reached USD 2.68/kg, increasing 0.75% WoW and 7.63% MoM, while remaining unchanged YoY. Buyers focused primarily on nearby coverage, with activity centered on routine business rather than extended positions. Demand from food manufacturers, particularly in bakery, confectionery, and recombination segments, has supported price recovery. Additionally, the absence of heavy intervention stocks and stable export flows to Southeast Asia and the Middle East have contributed to firmer pricing.

Oceania SMP stood at USD 2.86/kg, up 8.33% WoW and 12.16% MoM but down by 1.04% YoY. Production is steady to slightly lower as seasonal milk output declines, tightening inventories and supporting the price floor.

South America’s SMP remained steady at USD 3.28/kg WoW, remaining at this level since W51. This resilience is driven by limited export surplus, strong domestic absorption, and relatively tight regional supply conditions.

2. Price Analysis

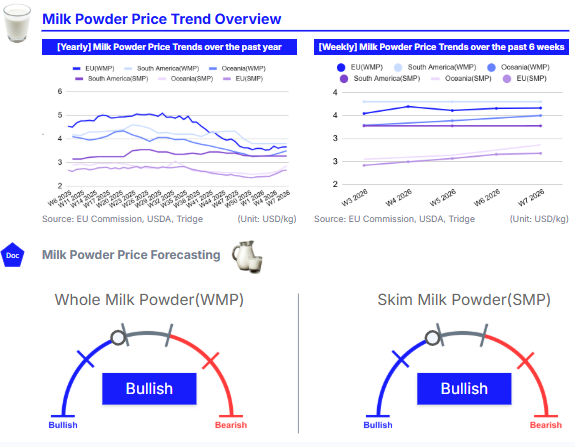

Milk Powder Markets Rally on Short Squeeze Despite Structural Oversupply in 2026

Global milk powder markets strengthened from early Jan-26, led by a short squeeze and tightening liquidity despite structurally weaker fundamentals. In Europe, SMP prices rose to USD 2563.53 per metric ton (EUR 2,200/mt) in late Jan-26, with second-quarter delivery reaching USD 2796.58/mt (EUR 2,400/mt) as limited offers pushed buyers to chase higher prices. WMP also moved higher but remained fundamentally weaker and more volatile, with EU WMP prices reaching USD 3612.25/mt (EUR 3,100/mt). Meanwhile, Oceania WMP stood at USD 3320.94/mt (EUR 2,850/mt), supported by tightening inventories, seasonal milk tapering, and lower volumes on offer. The 10% increase in SMP prices quickly lifted WMP fair value, while Oceania’s Global Dairy Trade (GDT) Event 398 recorded WMP price index gains of up to 3.7% for Mar-26–Jun-26 deliveries, with sales volumes slightly higher than Event 397 but below Event 374 a year earlier. North Asia accounted for 41% of total WMP purchases, followed by Southeast Asia/Oceania at 22%. Chinese WMP stocks remained low and domestic production stayed well below 2023 peak levels, supporting export expectations. However, EU WMP production declined 8.6% YoY in 2025, exports fell 21% YoY, and prices were still 17.7% below the five-year average, although they increased 1.1% in the four weeks to mid-Feb-26.

Despite recent price gains, broader milk supply conditions point to continued pressure in 2026. EU cow’s milk collection rose 5.7% YoY in Dec-25 to 650 thousand mt, with annual 2025 collection 1.6% higher than 2024. Production expanded strongly in Germany (7.8%), France (8%), the Netherlands (7%), and Poland (4.4%).

Globally, major exporting regions ended 2025 over 2% higher YoY in production, with US milk output supported by an additional 250,000 cows. While near-term SMP fundamentals appear slightly tighter, both SMP and WMP markets remain exposed to surplus milk, high stocks, and export dependence, suggesting continued volatility and downward structural pressure through the first half of 2026.

3. Strategic Recommendations

Strengthening Resilience in EU and Global Milk Powder Markets

In light of current market volatility, stakeholders are recommended to implement short-term procurement strategies to mitigate exposure to sudden price fluctuations. With European WMP averaging USD 3.67/kg and SMP at USD 2.68/kg, the emphasis should be placed on flexible, nearby coverage contracts rather than long-term bulk commitments. Food manufacturers, particularly in bakery, confectionery, and recombination sectors, are encouraged to stagger purchases across monthly or quarterly deliveries, allowing for price optimization in response to short-term supply tightening and seasonal production moderation.

Given the differing regional market conditions, stakeholders should diversify sourcing and export channels. Oceania WMP and SMP have risen while South American WMP remains stable, reflecting regional supply-demand balance. Procurement policies should promote multi-region sourcing to mitigate risks from local supply constraints or currency fluctuations. Exporters are advised to prioritize high-demand markets, particularly North Asia and Southeast Asia/Oceania, leveraging low Chinese WMP stocks and below-peak domestic production to secure market share and optimize revenue. Forward contracts for Q2-2026 and Q3-2026 deliveries can be considered to capture favorable pricing observed in GDT WMP index gains of up to 3.7%.

Additionally, policy should emphasize efficient inventory management and product mix optimization in response to structural oversupply. Stakeholders should prioritize conversion of surplus milk into SMP and other value-added dairy products to reduce stock pressure. Policies encouraging optimization of WMP and SMP conversion ratios can enhance profitability, as rising SMP prices support WMP fair value. Risk management frameworks should include market hedging through futures and options, combined with continuous monitoring of seasonal supply changes, export demand, and currency impacts, ensuring resilience against market volatility while maintaining alignment with global trade dynamics.