.jpg)

1. Weekly News

Morocco

Morocco Extends Support for Milling Wheat Imports Through Apr-25

Morocco's National Inter-Professional Office for Cereals and Legumes (ONICL) confirmed that the government will continue supporting milling wheat imports until the end of Apr-25. This decision, made by the Ministries of Finance and Agriculture, extends a support system initially set to end in Dec-24. Morocco has heavily relied on wheat imports over the past two years due to poor domestic crops, making it a key export destination for the European Union (EU) and Russia. Historically, Morocco used to halt imports during good crop years to protect domestic supplies but has taken no such action this year. The support extension will ensure a steady flow of wheat supplies to mills until Morocco's next harvest season. France has traditionally been a major supplier of wheat to Morocco. However, due to poor harvests in France and Morocco's efforts to encourage competition from lower-priced suppliers in the Black Sea region, Russia has expanded its presence in Morocco's wheat market, further highlighting the importance of this market for French traders.

Russia

Russia's 2025 Wheat Crop Forecast Reduced Due to Worst Crop Conditions in Decades

Russia revised its 2025 wheat crop forecast downward by 3 million metric tons (mmt), bringing the total estimated production to 78.7 mmt. Attributed to the worst crop conditions in decades, this adjustment makes it the smallest wheat harvest since 2021, when production reached 76 mmt. Winter wheat production is now projected at 50.7 mmt, a reduction of 3.6 mmt from previous estimates. The current crop conditions in Russia, the world's largest wheat exporter, are the most challenging in decades, contributing to a tighter global supply and demand balance for wheat. He also noted that these factors have yet to be fully reflected in the market, suggesting potential price volatility in the coming months.

Saudi Arabia

Saudi Arabia Secured 804 Thousand MT of Durum Wheat for Delivery in Early 2025

Saudi Arabia's General Food Security Authority (GFSA) has procured 804 thousand metric tons (mt) of durum wheat in an international tender, surpassing the initially requested 595 thousand mt. With a protein content of 12.5%, the wheat is set for delivery to ports in Jeddah, Dammam, Yanbu, and Jizan between Feb-25 and Apr-25. The potential origins of the wheat include the EU, the Black Sea region, North America, South America, and Australia, leaving sellers to determine the source. Preliminary trader estimates suggest one or two consignments may originate from Russia, with additional supplies coming from Romania, Bulgaria, and South America.

United Kingdom

UK Faces Tight Wheat Supply in 2024/25 Despite Significant Beginning Stocks

The United Kingdom's (UK) wheat market for the 2024/25 marketing year (MY) faces a tight balance despite significant beginning stocks of 3.26 mmt, according to the Foreign Agricultural Service (FAS) of the United States Department of Agriculture (USDA). These stocks have partially mitigated concerns about the second smallest wheat harvest since 1999 to 2000, estimated at 10.9 mmt, a decline of approximately 3 mmt year-on-year (YoY) and one of the lowest in recent history. FAS noted that while more prominent barley and oats crops will help address some feed grain supply shortages, high demand for corn imports for feed is expected to persist. Wheat imports are also forecast to rise by over 150 thousand mt compared to the significant 3.15 mmt imported in 2023/24. Despite the increase in imports and carryover stocks, the tight supply remains a key issue. The nearly 1 mmt YoY rise in carryover stocks from 2023/24 provides an essential buffer but is expected to be almost entirely depleted by the end of the 2024/25 MY.

Vietnam

Vietnam’s Wheat Imports Grew From Jan- 24 to Nov-24

From Jan-24 to Nov-24, Vietnam's wheat imports totaled over 5.37 mmt, valued at nearly USD 1.48 billion, reflecting a YoY increase of 34.8% in volume and 8.3% in value compared to the same period in 2023. The average import price was USD 274.9/mt, a YoY decrease of 19.6%. Ukraine emerged as Vietnam's largest wheat supplier, accounting for 26.5% of the total import volume and 24.6% of the total import value. Shipments from Ukraine reached over 1.42 mmt, worth USD 363.77 million, at an average price of USD 255.5/mt. This represented a significant YoY surge of 349.9% in volume, a 312.6% increase in turnover, but an 8.3% decline in price.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W51 2023 to W51 2024)

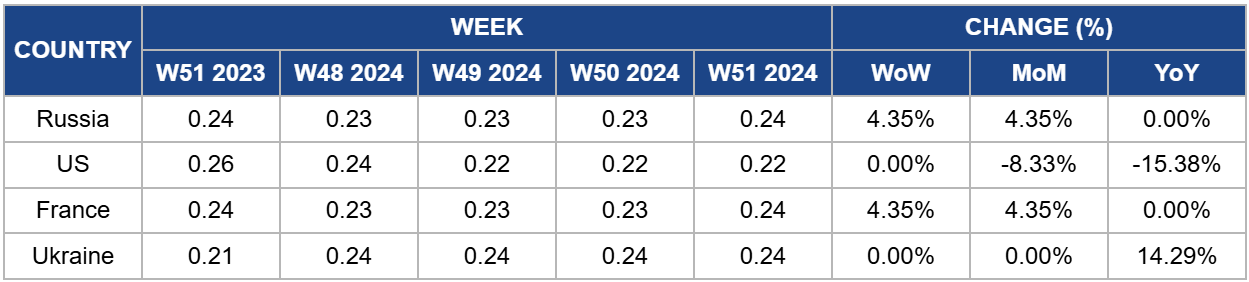

Russia

In W51, Russian wheat prices increased 4.35% week-on-week (WoW) and month-on-month (MoM) to USD 0.24 per kilogram (kg). This price rise is due to several key factors, including increased export demand, particularly from countries in the Middle East and Asia, and logistical challenges other global exporters face. Russia remains a major supplier, and 2024 wheat exports are projected to be around 40 mmt, up from 38 mmt in the previous year. Moreover, the tightening of global wheat supplies due to poor harvests in Europe has reduced competition, further supporting the upward trend in Russian wheat prices.

United States

In W51, wheat prices in the United States (US) remained stable WoW at USD 0.22/kg but experienced 8.33% MoM and 15.38% YoY declines. This decrease can be primarily attributed to improved crop conditions, as favorable rain and snow in Nov-24 provided a buffer for the post-dormancy development phases expected in spring 2025. The USDA's winter wheat condition index showed a record 35-point improvement from late Oct-24 to late Nov-24. Additionally, by November 24, farmers had completed 97% of the expected winter wheat planting for the 2025 harvest, matching last year's rate and slightly falling below the five-year average. There were significant increases in planting activity in California and North Carolina, with 16 of the 18 major wheat-producing regions either completed or near completion of their planting activities.

France

In W51, French wheat prices increased by 4.35% WoW and MoM to USD 0.24/kg, driven by strong export demand, particularly from North African countries like Morocco, which have relied on French wheat due to poor harvests and extended import support programs. Tightened domestic supply from lower carryover stocks and increased miller purchases during the holiday season further supported the price rise. Moreover, while Russia's competitively priced wheat has increased global competition, logistical constraints, and buyer preferences in key markets have favored French exports. Currency fluctuations also played a role, enhancing the competitiveness of French wheat in international markets.

Ukraine

In W51, Ukrainian wheat prices remained stable WoW and MoM at USD 0.24/kg but rose 14.29% YoY, primarily due to drought concerns impacting winter wheat planting for the 2025 harvest. The ongoing war with Russia and unfavorable weather have reduced the winter wheat sown area to an estimated 4.2 million hectares (ha), down from 4.4 million ha in the previous year. These factors will result in a smaller harvest and lower carryover stocks, limiting Ukraine’s exportable surplus. These supply constraints and strong global demand have exerted upward pressure on prices.

3. Actionable Recommendations

Strengthen Wheat Production Through Irrigation Development

Vietnam should prioritize the development of advanced irrigation systems to ensure stable wheat production in drought-prone regions. By adopting technologies like drip or sprinkler irrigation, farmers can optimize water use, increasing yield and reducing crop loss during dry spells. Moreover, Vietnam could explore water harvesting techniques to capture and store rainwater, mitigating the impact of erratic weather patterns. Reducing dependency on imported wheat through improved domestic production would allow Vietnam to allocate resources to other strategic agricultural sectors.

Expand Storage and Processing Capacity for Export Competitiveness

Ukraine should invest in upgrading its grain storage and processing facilities to manage tighter wheat supplies efficiently. In years with reduced production, having adequate storage will allow Ukraine to regulate the flow of exports and avoid flooding the market at lower prices. This can also prevent wastage during peak harvest periods. Furthermore, processing capacity expansion, such as milling or packaging facilities, would enable Ukraine to export higher-value products rather than raw wheat, increasing revenue. Such infrastructure improvements are particularly critical given the ongoing war and adverse weather patterns, which have strained the country's agricultural sector. Financial incentives for private sector investments in these areas could accelerate progress.

Strengthen Export Logistics for Increased Trade Opportunities

Russia should improve its wheat export infrastructure to manage growing global demand, especially from Middle Eastern and Asian markets. Current logistical challenges, such as port congestion and inadequate rail connections, can delay shipments, reducing Russia's competitiveness despite its lower prices. Investments in modernizing port facilities, expanding rail networks, and streamlining export processes could significantly enhance throughput capacity. Moreover, fostering public-private partnerships to fund these projects could expedite development. With projections of 40 mmt of wheat exports in 2024, Russia has a significant opportunity to strengthen its market share, particularly in regions where logistical efficiency is a decisive factor.

Sources: Tridge, NoticiasAgricolas, Oilworld, Rue20, UkrAgroConsult, Vinanet