.jpg)

In W8 in the wheat landscape, some of the most relevant trends included:

- Western Australia exceeded wheat harvest forecasts, reaching 12.45 mmt in 2024/25.

- The UK’s wheat imports also rose 60% YoY, reflecting strong demand for high-quality milling wheat.

- India faces potential wheat price inflation due to above-normal temperatures. In Ukraine, drought conditions have reduced winter wheat planting by 9% YoY.

- Russian wheat prices rose MoM, driven by lower harvest forecasts, while US wheat prices fell YoY due to strong domestic output. French wheat prices increased YoY, but exports declined due to diplomatic tensions and market competition.

1. Weekly News

Australia

Western Australia’s Wheat Harvest Surpassed Forecasts, Strengthening Export Position

Western Australia’s wheat farmers achieved an impressive harvest of 12.45 million metric tons (mmt) in the 2024/25 season, surpassing forecasts by 1.6 mmt. This exceptional yield was due to favorable weather conditions, particularly a warmer winter, and strategic farming practices that maximized productivity. The high output has reinforced Western Australia’s position as a key player in the country’s wheat exports, strengthening its competitiveness against New South Wales. Notably, this harvest marks the third-largest wheat yield ever recorded in the region, with the Grain Industry Association of Western Australia (GIWA) having underestimated pre-harvest projections by up to 20%.

Azerbaijan

Azerbaijan’s Wheat Imports Surged by 23.5% YoY in Jan-25

According to the State Customs Committee, Azerbaijan imported 86,654 metric tons (mt) of wheat in Jan-25, marking a 23.5% year-on-year (YoY) increase. The value of these imports reached USD 18.7 million, up by USD 2.4 million or 14.8% YoY. Wheat accounted for 0.91% of Azerbaijan’s total imports.

India

North India's Warm Winter Pose Risks to Wheat Crop and Inflation

An unusually warm winter in North India raised concerns over the wheat crop, potentially driving up prices and fueling inflation. As the world’s second-largest wheat producer, India has already seen wholesale wheat prices rise on Jan-25 ahead of the new harvest. While the government remains optimistic about a good yield, the Indian Meteorological Department has forecasted above-normal temperatures and below-normal rainfall in Feb-25, which could threaten crop development. However, an incoming Western disturbance may provide some relief to wheat-growing regions. Economic analysts warn that continued high temperatures into Mar-25 could negatively impact Rabi crop production, slowing the decline in food inflation. Jan-25 saw wholesale price inflation ease to 2.31%, but wheat inflation surged to 9.8% YoY, its highest level in nearly two years.

Russia

Russia’s Wheat Stocks Declined 21% YoY in Jan-25 Amid Accelerated Farmer Sales

As of January 1, Russian total wheat stocks stood at 28.7 mmt, marking a 21% YoY decrease from the same period in 2024. The gap, which was 14% in October, has widened due to active sales by agricultural producers. The decline is evident across all key exporting regions, with the Southern Region experiencing the largest drop at 7.8 mmt, down 37% YoY, followed by the Central Region at 6.3 mmt, down 32% YoY, and the Volga Region at 6.4 mmt, down 17% YoY. The most significant stock reduction has occurred on farms, where wheat reserves fell by 29% YoY to 15.4 mmt as of January 1. Farmers have accelerated wheat sales, with Dec-24 transactions reaching 4.8 mmt, up from 4.3 mmt in Dec-23, despite lower production levels. In contrast, ex-farm stocks have experienced a less pronounced decline, standing at 13.3 mmt, a 9% YoY decrease.

United Kingdom

UK Wheat Imports Remained High in 2024/25

According to the Agriculture and Horticulture Development Board (AHDB), the United Kingdom’s (UK) wheat imports remained elevated in Dec-24, while exports experienced a modest uptick. Since the beginning of the 2024/25 season (July to December), wheat imports have totaled 1.70 mmt, reflecting a 60% YoY increase and standing 74% above the five-year average. Germany, Canada, and Denmark were the primary suppliers, underscoring the UK's reliance on high-quality imported wheat for the milling industry. Looking ahead, total wheat imports for the season will reach 2.75 mmt, with 62% of this volume already accounted for by mid-season.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W8 2024 to W8 2025)

Russia

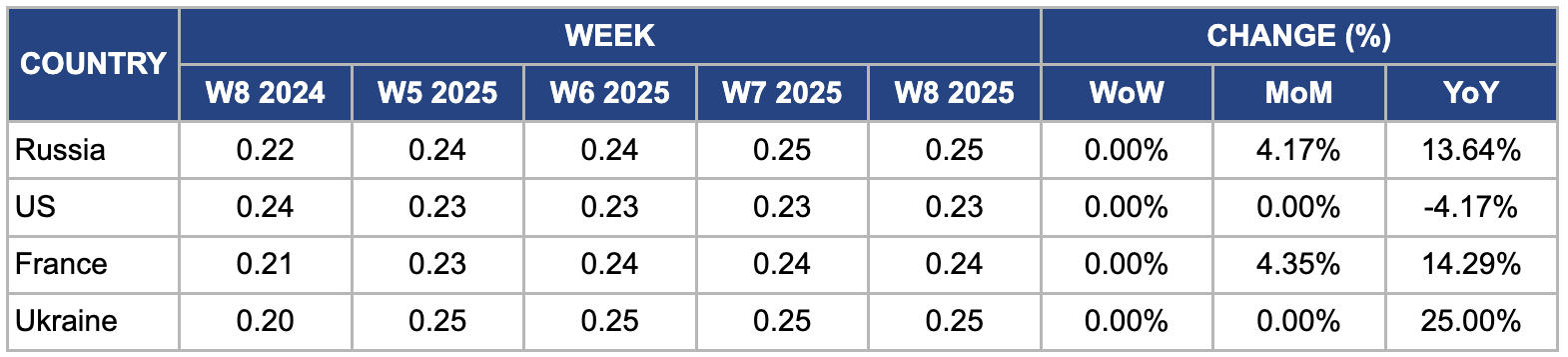

In W8, Russian wheat prices remained stable week-on-week (WoW) but rose by 4.17% month-on-month (MoM) and 13.64% YoY to USD 0.25 per kilogram (kg). The price increase follows the downward revision of Russia’s 2025 wheat harvest forecast to 87 mmt from 89 mmt, citing insufficient precipitation in the Volgograd and Rostov regions and mild frosts affecting crop conditions. This aligns with broader global supply concerns, as the United States Department of Agriculture (USDA) lowered final stock estimates to 257.76 mmt and cut Russian wheat export projections to 45.5 mmt. Russian farmers are reducing wheat cultivation due to rising costs and low prices. The Russian Grain Union (RGU) president also warned of heightened risks of crop failure due to inadequate snow cover and cold fronts.

United States

In W8, United States (US) wheat prices remained unchanged WoW but declined 4.17% YoY to USD 0.23/kg, primarily due to higher domestic production and global wheat supplies. The 2024/25 US wheat output increased, supported by favorable weather and improved yields, leading to ample stock levels. Moreover, intensified competition from major exporters like Russia, Canada, and Australia, where production costs are lower, pressured US wheat prices. Weaker export demand due to competitive pricing from these countries further contributed to the decline, while global price trends reflected ample availability, limiting upward movement in US wheat prices.

France

In W8, French wheat prices remained unchanged WoW but rose by 4.35% MoM and 14.29% YoY to USD 0.24/kg due to a downward revision in 2024/25 production forecasts. France’s wheat export sector experienced challenges from diplomatic tensions with Algeria, reduced Chinese demand, and a poor harvest, leading to a loss of market share to more competitive producers like Russia. The country’s soft wheat harvest has reached its lowest level since the 1980s, while competition from Eastern Europe continues to intensify. Exports to Algeria and China have declined sharply, and sales to Morocco have more than halved, forcing some companies to place staff on unpaid leave. In response, France is working to diversify its export markets by strengthening its presence in the Middle East.

Ukraine

In W8, Ukrainian wheat prices remained unchanged at WoW and MoM but surged 25% YoY to USD 0.25/kg. The 2024/25 wheat harvest forecast remains stable at 22.9 mmt, though export estimates have been revised downward to 16 mmt. As of early Dec-24, Ukraine had sown 4.38 million hectares (ha) of winter wheat, nearly 2% below the planned area and down 9% YoY due to persistent drought conditions affecting key growing regions. The reduced planting area raises concerns over future yields and export availability, potentially tightening the global wheat supply.

3. Actionable Recommendations

Leverage Western Australia’s Strong Harvest for Export Expansion

Australian exporters should capitalize on the 12.45 mmt record wheat harvest by targeting price-sensitive markets like Southeast Asia and the Middle East. With favorable weather conditions boosting yields, Western Australian wheat is well-positioned to compete in global markets. Strengthening trade relationships and offering competitive pricing can help expand exports, especially as demand remains strong in key Asian and Middle Eastern destinations. The expected benefit of this strategy is increased export volumes and improved market share against competing suppliers like Russia and Canada. Western Australian wheat exporters can secure long-term buyers and stabilize revenues by leveraging their production advantage.

Hedge Against Indian Wheat Price Volatility

Indian millers and traders should secure wheat contracts early or explore alternative import sources, such as Australia and Ukraine, to mitigate potential price spikes caused by India’s unusually warm winter. The rising uncertainty over India’s wheat production could lead to domestic supply shortages and higher prices, making it crucial for buyers to secure supply chains in advance. The expected benefit of this approach is cost stability and reduced risk of supply disruptions. By diversifying sources and locking in prices ahead of time, millers and traders can avoid the financial strain of sudden price hikes or policy changes in India.

Diversify Export Markets for French Wheat

French exporters should strengthen trade agreements with Middle Eastern buyers, particularly in Egypt and Saudi Arabia, to offset losses from Algeria and China. Given the downward revision of France’s wheat production forecasts, it is essential to maintain strong demand in stable, high-volume markets. Expanding into newer markets or strengthening existing relationships can help maintain export levels despite supply constraints. The expected benefit of this strategy is reduced dependency on volatile markets and sustained demand for French wheat. By securing buyers in regions with consistent wheat import needs, France can mitigate the risks associated with lower domestic output and fluctuating demand from key trading partners.

Sources: Tridge, Agromeat, UkrAgroConsult