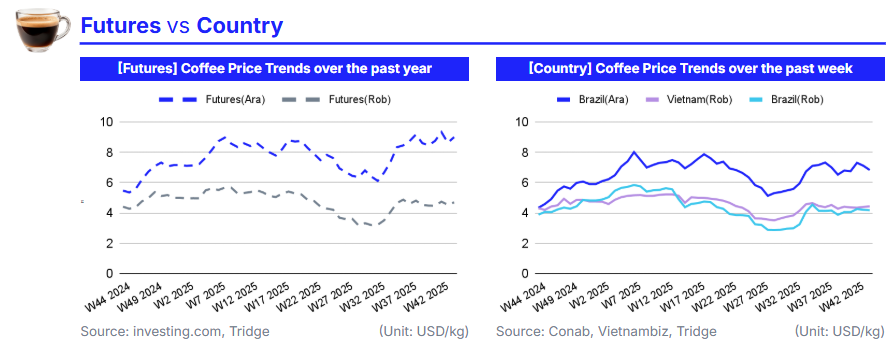

In W44 2025, global coffee prices strengthened for the second consecutive week as tightening certified stocks and ongoing trade disruptions supported the market. Arabica rose 4.23% WoW to USD 9.01/kg, while Robusta increased 3.50% WoW to USD 4.70/kg, driven by falling inventories and reduced export flows from Brazil under the 50% US tariff. Meanwhile, Brazil’s domestic prices weakened, with Arabica down 3.98% WoW and Robusta down 0.83% WoW amid a stronger real and improved weather conditions, while Vietnam maintained stable Robusta prices around USD 4.4/kg.

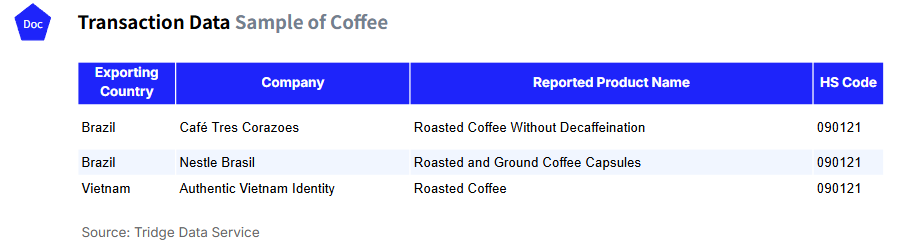

Global coffee importers and roasters in the Americas and Europe should adopt a dual-origin sourcing strategy from Brazil and Vietnam to balance cost and supply stability amid tariff and currency volatility. Buyers should secure medium-term contracts with Café Três Corações and Nestlé Brasil while expanding procurement from Authentic Vietnam Identity to hedge against disruptions and position strategically ahead of potential market corrections in early 2026.

1. Weekly Price Overview

Global Coffee Prices Rebound as Brazilian Rates Decline Under Tariff Uncertainty and Tight Global Stocks

In W44 2025, global coffee prices strengthened for a second consecutive week as supply constraints and trade disruptions continued to support the market. The international Arabica price, represented by US Coffee C Futures, rose 4.23% week-on-week (WoW) to USD 9.01 per kilogram (kg), while Robusta, represented by London Coffee Futures, increased 3.50% WoW to USD 4.70/kg. The rebound followed an early-week dip driven by improved rainfall forecasts in Brazil, before tightening inventories and renewed trade uncertainty reversed the trend.

Intercontinental Exchange (ICE)-certified Arabica stocks fell to 446,475 bags, a new annual low, while Robusta stocks stood at 1,018,500 bags, according to ICE data. Market sentiment was also shaped by the 50% US tariff on Brazilian coffee, which has disrupted trade flows and prompted US roasters to draw down inventories or delay purchases. This has raised roasted coffee retail prices in the US by 41% year-on-year (YoY) in Sep-25, averaging USD 9.14/lb, according to the Bureau of Labor Statistics. In Brazil, farmgate Arabica prices fell 3.98% WoW to USD 6.84/kg, and Robusta dropped 0.83% WoW to USD 4.18/kg amid improved weather in key producing states and speculation that the US may remove tariffs on Brazilian imports. Meanwhile, Vietnam’s crop outlook remains steady at USD 4.43/kg with a minimal rise of 0.73% WoW, although heavy rains have disrupted harvesting in some areas.

2. Price Analysis

Global Coffee Prices Strengthen as Tight Inventories Lift Futures While Brazilian Rates Weaken Under Tariff Pressure

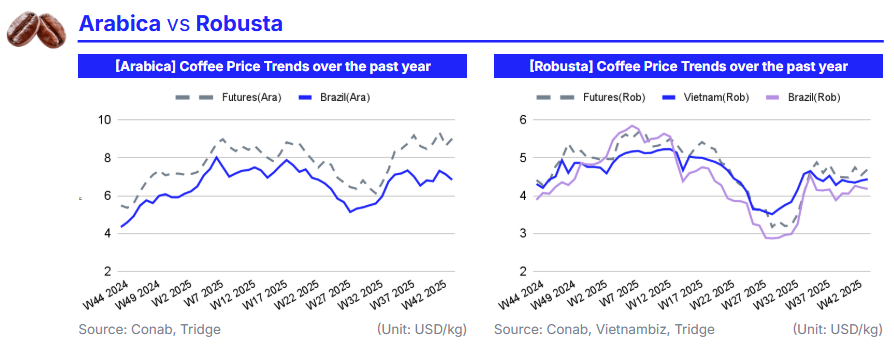

Analyzing the recent data, international coffee prices in W43 2025 show strong WoW gains, led by Arabica with a 4.23% rise to USD 9.01/kg and Robusta with a 3.50% increase to USD 4.70/kg. This rebound is primarily driven by shrinking certified stocks in New York, which fell to 446,475 bags, and in London, where Robusta inventories remain low at just over one million bags. The tight stock situation has intensified upward pressure on futures as US roasters draw down inventories amid ongoing tariff-related trade disruptions. The 50% US tariff on Brazilian coffee, which covers nearly one-third of US imports, has reduced export flows from Brazil, creating temporary supply gaps and amplifying speculative buying across exchanges.

This short-term rally contrasts with Brazil’s domestic market, where Arabica and Robusta prices fell by 3.98% and 0.83% WoW, respectively, due to the appreciation of the Brazilian real and limited export competitiveness. Improved rainfall forecasts in Minas Gerais and São Paulo have eased some weather concerns, although earlier dryness has already affected flowering and could limit yield potential for the 2025/26 crop. On the other hand, Vietnam’s Robusta sector benefits from generally favorable growing conditions, supporting steady exports despite occasional heavy rains.

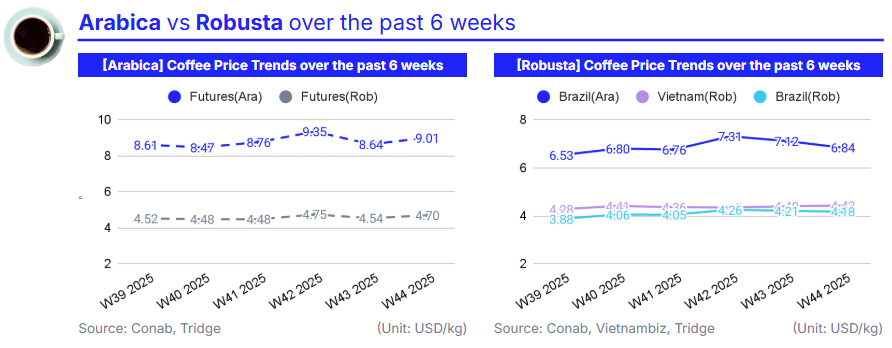

Given the structural tightness in global stocks and policy uncertainty surrounding US tariffs, the short-term outlook remains moderately bullish. Prices are expected to hold firm through Q4-2025, supported by limited supply recovery and persistent logistical inefficiencies. However, if the US removes tariffs on Brazilian or Vietnamese coffee, a temporary price correction could follow as trade flows rebalance. Overall, Arabica prices are projected to remain between USD 8.8 to 9.3/kg and Robusta between USD 4.6 to 4.9/kg through early 2026, with volatility tied to weather and policy outcomes.

3. Strategic Recommendations

Adopt Dual-Origin Coffee Sourcing From Brazil and Vietnam to Balance Cost Efficiency and Supply Stability

Global coffee buyers should adopt a dual-origin sourcing strategy focused on Vietnam and Brazil to balance cost efficiency with supply security amid ongoing tariff and currency volatility. The recent rebound in global prices, driven by tightening certified stocks and reduced Brazilian exports under the 50% US tariff, suggests that Arabica and Robusta will remain elevated through Q4-2025. However, Brazil’s domestic price decline and improved weather outlook present an opportunity to lock in medium-term contracts before any potential tariff removal triggers a correction.

For industrial buyers and roasters in the Americas, according to Tridge Eye, sourcing Brazilian roasted coffee products, particularly from Café Três Corações and Nestlé Brasil, remains strategically attractive. These producers are well-positioned to offer competitive pricing and reliable quality as local farmgate rates remain under pressure from real appreciation. Securing fixed-price or indexed contracts through early 2026 would help hedge against renewed upward movements in global benchmarks, while maintaining supply consistency despite export constraints.

Meanwhile, importers in Asia and Europe should expand procurement from Vietnam’s Authentic Vietnam Identity, leveraging its stable Robusta production and competitive export pricing around USD 4.4/kg. This origin offers insulation from US trade policy risks and benefits from favorable weather conditions and resilient logistics. For value-added coffee producers and capsule manufacturers, incorporating Vietnamese beans into blends could offset rising Arabica costs while maintaining product quality.

Traders should maintain a moderately bullish stance on coffee through early 2026, using short-dated call options to capture potential upside from tightening stocks, while industrial users secure forward contracts at current levels to protect against renewed price volatility once global trade flows normalize.