June Outlook Report: Meat and Seafood

Rene Salinas

게시됨 2023년 6월 1일

PDF 파일 미리보기

•Beef prices in Europe fell as the effect of lower demand managed to more than offset declines in domestic supply. Meanwhile, Brazil’s prices dropped in May despite the lifting of the export ban to China, underlining weak local demand and abundant domestic supply due to lower than expected exports (other importers are shifting origins).

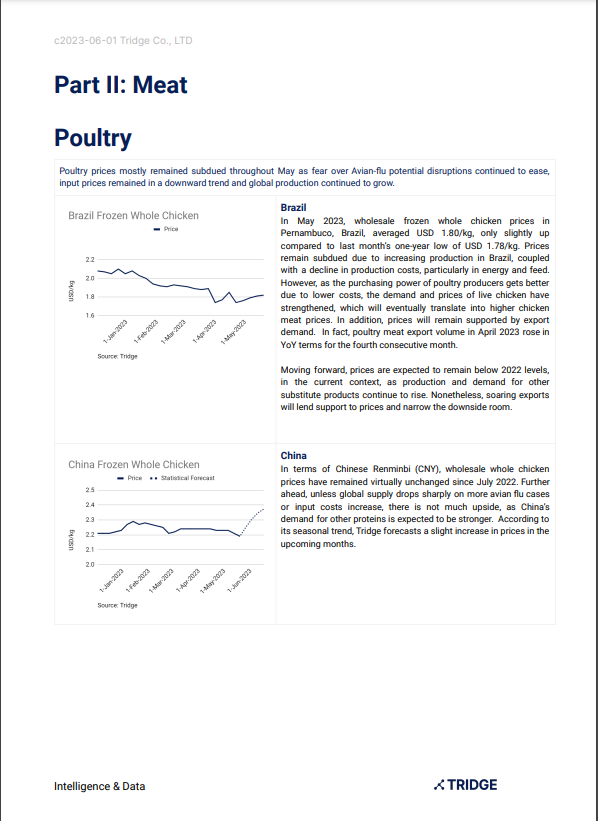

•Poultry prices mostly remained subdued throughout May as fear over Avian-flu potential disruptions continued to ease, input prices remained in a downward trend and global production continued to grow. However, further downside room is limited.

•Fresh Atlantic salmon prices in Norway, the largest exporter of this product, remain considerably high due to supply constraints. The new salmon tax was already voted on and fixed at 25%, which is lower than the original proposal. For the very short term, this clarity might be bearish for prices, but the tax, in addition to lower supply of salmon, is net bullish in the longer term.

•As expected, shrimp prices have mostly continued to ease globally, and the outlook for upcoming months is mainly bearish as global supply continues to increase faster than demand. Strong competition within the world’s two major shrimp exporters, Ecuador and India, continues to add further downward pressure on prices.

•Poultry prices mostly remained subdued throughout May as fear over Avian-flu potential disruptions continued to ease, input prices remained in a downward trend and global production continued to grow. However, further downside room is limited.

•Fresh Atlantic salmon prices in Norway, the largest exporter of this product, remain considerably high due to supply constraints. The new salmon tax was already voted on and fixed at 25%, which is lower than the original proposal. For the very short term, this clarity might be bearish for prices, but the tax, in addition to lower supply of salmon, is net bullish in the longer term.

•As expected, shrimp prices have mostly continued to ease globally, and the outlook for upcoming months is mainly bearish as global supply continues to increase faster than demand. Strong competition within the world’s two major shrimp exporters, Ecuador and India, continues to add further downward pressure on prices.

목차

Part I: Key Indicators

Part II: Meat

Beef

Poultry

Part III: Seafood

Fresh Atlantic Salmon

Frozen Shrimp

관련 시장 데이터

관련 콘텐츠 더 보기

'쿠키 허용'을 클릭하면 통계 및 개인 선호도 산출을 위한 쿠키 제공에 동의하게 됩니다.

개인정보 보호정책에서 쿠키에 대한 자세한 내용을 확인할 수 있습니다.