Demand for Australian Canola Rises as EU Production Suffers

Canola oil prices are currently at a high point as Chinese demand soars and production in the EU has been faltering in recent years. Shifting market dynamics have been conducive to Australia, whose booming production of non-GM canola seeds has allowed it to reaffirm its main exporter status in Europe as well as expanding further to Asian markets.

Production Falters in the EU

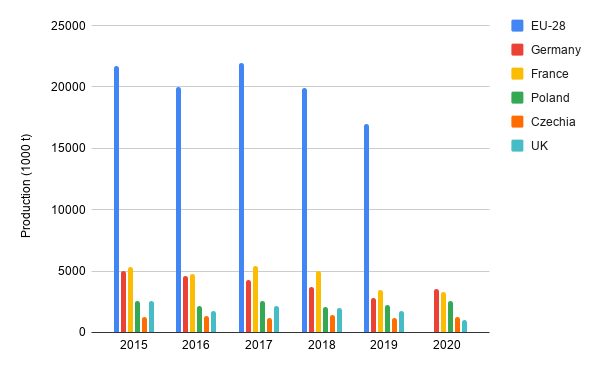

The EU is one of the largest producers of canola, accounting for approximately 30% of total production, but this is set to change as production has been lackluster in recent years. This season, rapeseed production has been hit by severe weather conditions, and while Germany and Poland have maintained their production, largest rapeseed producers France and Ukraine have been greatly affected.

One of the most prominent producers in the EU, France, has suffered the most damage, with reports that production areas have been on the down-low for two consecutive years, averaging around 1 million ha compared to 1.5 million ha. It will get more difficult for the country to return to its previous levels of harvest as increasing production costs and declining yields from pests and weather continue to weigh on growers.

Graph 1: Decreasing Rapeseed Production in the EU

Source: Eurostat*2020 results for EU-28 not available yet

With the continuous trend of decreasing canola production in the EU, the EU has begun to rely more on imports, especially from Ukraine, in which it has supplied roughly 80% of all the EU imports in 2019. However, Ukraine has also suffered from bouts of bad weather this year, on top of the fact that new regulations from the EU limiting pesticides in imports will make it even more difficult for Ukrainian exporters to get their crops across.

Potential for Australian Canola Rises as Competitors Weaken

Australian canola oil is one of the largest canola industries in the world, annually producing more than three million metric tons (with about one million used domestically) and exporting up to 20 percent of the world’s export trade. Australia’s largest market is the EU, which imported an average of two million MT, or USD 1.1 billion, canola annually between 2015 and 2018, with Belgium and Germany being particularly popular destinations. China and Japan are among the next largest markets, having imported USD 80 million and 106 million respectively in the same timeframe.

Graph 2: Major Export Destinations of Australian Canola

Source: Australian Export Grains Innovation Centre.

After two years of drought-ridden production, Australia is projected to rebound immensely in terms of canola production in the 2020/21 crop year, with harvest expectations estimating as high as 3.3 million MT, which would approximate to a 43 percent increase from the previous year. As such, the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) predicts that canola exports could also increase by 42 percent within the next season.

However, Australia’s typical export destinations could be subject to change in the coming years. Australian Export Grains Innovation Centre chief economist Ross Kingwell was especially cognizant of how reliant the Australian canola industry is on the EU, stating that the market was at the mercy of the constantly changing European Union trade policies like the Renewable Energy Directive. While he still believes Australian canola holds several competitive advantages compared to other foreign canola industries, such as using non-GM seeds to produce oils, this puts Australia at risk of being constrained by future potential EU regulations. Thus Kingwell advocates for Australia to diversify its markets to become less reliant on the EU.

One of the most promising markets is China, which has significantly increased demand for Australian crude canola oil as of late despite the progression of the Australia-China Trade War. While the Australia-China Trade War has soured relationships between the two nations, many suppliers are confident that China will still continue to rely on Australian canola despite the threat of tariffs other agricultural industries have been facing. This belief is based on the difficulties in production within the EU combined with how another major supplier of canola and rapeseed, Canada, is in a potentially worse relationship with China than that of Australia.

Australia is also expected to make inroads in expanding further to South Korea and Taiwan. Prices of crude canola oil have risen dramatically due to decreases in supply, and as a result, demand for Australian refined bleached deodorized canola oil from these countries has increased.

Sources

- Australian Broadcasting Corporation. “Australia's canola trade is 'dangerously exposed' to global disruptions and must diversify, experts warn.”

- Bloomberg. “Europe’s terrible rapeseed crops are pulling down global supply.”

- Agricensus. “EU faces fresh fears of tight rapeseed supply in 2020.”

- Australian Export Grains Innovation Centre. Canola.