Demand Shifts: Emerging Consumer Demand is Rebuilding Global Food Trade

Table 1. Summary Table of Global Consumer Demand Shifts

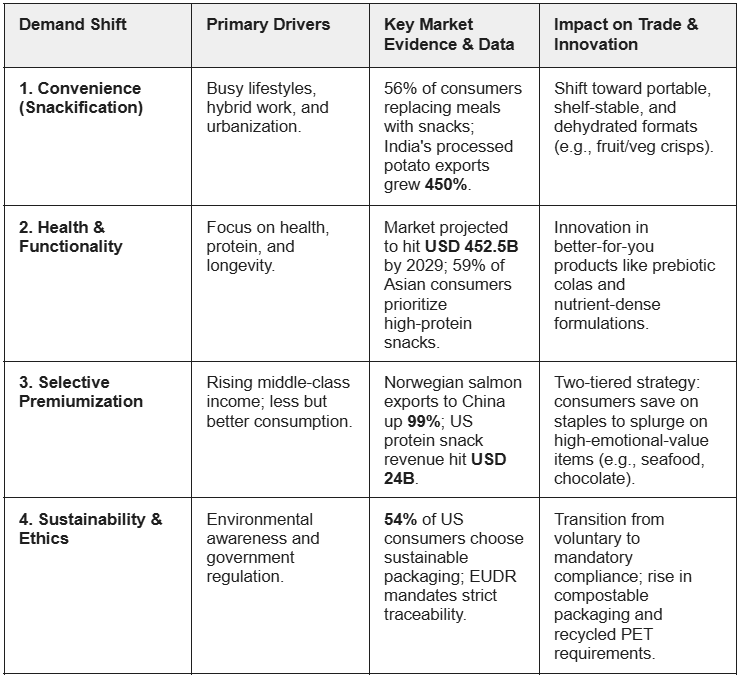

Consumers Gravitate Towards Convenience, Functionality, Premiumization, and Sustainability

In 2025, global food demand experienced structural transformation as consumers increasingly prioritized convenience, health, premiumization, and sustainability over price and quantity alone. These shifts are driven by urbanization, rising middle-class incomes, and growing environmental and health awareness, particularly in Asia, Africa, and Europe. As a result, global agri-food trade is increasingly pivoting towards snacks, functional foods, plant-based ingredients, premium products, and sustainable packaging inputs. Looking ahead, global food demand is expected to remain anchored around these four dominant forces, convenience, health and functionality, premiumization, and sustainability. These drivers will increasingly manifest through deeper structural shifts, sustained product innovation, and packaging-led differentiation across the agri-food value chain.

Convenience and On-the-Go Lifestyles Fuel Snackification Across Consumption, Exports, and Product Innovation

Consumer demand in the agri-food sector is increasingly shifting toward convenience and on-the-go formats, reflecting busy and evolving lifestyles and the normalization of hybrid working patterns. This shift has accelerated the rise of snackification, with a 2024 International Food Information Council survey showing that 56% of consumers have replaced traditional meals with snacks or smaller portions, while 73% snack at least once daily. Asia is at the forefront of this global trend, redefining food consumption patterns across key markets such as India, Singapore, Vietnam, Thailand, Japan, and South Korea. According to Euromonitor, India leads globally, with around 18% of consumers regularly substituting meals with snacks.

As this convenience-driven trend gains momentum, it has created significant scaling opportunities for manufacturers and exporters across the region. For example, India has rapidly expanded its role in the processed snack supply chain, with Global Trade Research Initiative (GTRI) data showing that exports of dehydrated potato granules and pellets reached USD 63.3 million in 2025, a significant 450% increase compared to 2022. Over the same period, exports of other processed potato products, including flour, starch, chips, and ready-to-eat items, totaled USD 18.8 million, with nearly 80% shipped to Malaysia, the Philippines, Indonesia, Japan, and Thailand. These trade flows highlight Asia’s rapidly expanding snack and convenience food ecosystem.

At the same time, the on-the-go consumption trend is reshaping product innovation, particularly in packaging and format design. Manufacturers are increasingly prioritizing portability, ease of consumption, and occasion-based offerings to capture demand. For instance, Pringles introduced several products in 2025, such as Pringles x Miller Lite Beer Can Chicken and 7-Layer Dip, strategically launched ahead of the Super Bowl to capitalize on high-demand snacking occasions. Complementing this, Protis Global notes that 2025 innovation has strongly favored dehydrated and freeze-dried snack formats, including fruit and vegetable crisps, that combine nutritional positioning with shelf-stable convenience, while globally inspired bold flavors continue to broaden the appeal of quick, snackable foods.

Figure 1: Pringles Products Align with Convenience and On-the-Go Trends

Demand for Functional Foods and Nutrient-Rich Products Accelerate Innovation, Consumption, and Market Expansion

Health and functional nutrition has also emerged as a major global food demand driver, as consumers increasingly seek products that go beyond basic nourishment to deliver tangible health benefits. In recent years, this shift has become particularly pronounced across key focus areas such as gut health, protein enrichment, cognitive support, and longevity. Research and Markets estimates the global functional foods market at USD 310.68 billion in 2025, with projected growth at a 9.9% compound annual growth rate (CAGR) to reach USD 452.5 billion by 2029. This expansion is underpinned by evolving dietary patterns, the rise of personalized nutrition, a growing middle-class population, and heightened attention to gut health, clean labels, and natural ingredients.

In Asia, health-driven consumption is increasingly visible in snacking behavior, reinforcing demand for functional and nutrient-dense products. Tridge’s research indicates rising preference for savory and protein-rich snacks, with approximately 59% of Asian consumers prioritizing snacks high in protein, vitamins, and fiber, particularly among Gen Z and Millennials. This trend is further supported by the fact that around 62% of consumers in the region consume at least one healthy snack daily, underscoring the mainstreaming of health-positioned foods.

In response, manufacturers and processors are accelerating innovation in nutrient-rich formulations that align with these health and functional drivers. Capitalizing on growing consumer awareness, brands are reformulating and launching products that combine functionality with everyday consumption occasions. For example, Pepsi introduced its Prebiotic Cola, formulated with prebiotic fiber to support gut health, lower sugar and calorie content, and no artificial sweeteners, directly addressing the rapid expansion of the functional beverage segment in recent years.

Figure 2: Pepsi Prebiotic Cola Responds to Health and Low-Sugar Consumer Trends

Selective Premiumization and the Global Shift Toward High-Value Trade

The demand for premiumization has evolved significantly in 2025, moving beyond simple price-based luxury to a focus on functional value, personal relevance, and everyday indulgence. As global disposable incomes rise, particularly in emerging markets, consumers are increasingly substituting low-value staples with higher value-added goods, driving a structural shift in global trade balances. In the Asia-Pacific region, this is acutely visible in the rapid expansion of the food retail sectors of China and India. India’s food retail sector, for instance, reached a revenue of USD 869 billion in 2024, with consumers in Tier II and Tier III cities increasingly seeking out international brands and premium-quality imports. This demand has specifically fueled the trade of consumer-oriented products like tree nuts, fresh fruits and distilled spirits, which reached USD 8.4 billion in imports in 2024 and exhibited steady growth into 2025. Premium products with high growth potential include specialty chocolates including sugar-free options - a category which exhibited good growth in recent years - as well as premium frozen foods and ready-to-eat/cook options, a category that is expected to boom in the coming years.

In China, the appetite for premiumized luxury foods has remained resilient despite broader economic headwinds. This is most acutely visible in the high-end seafood sector, where Norwegian salmon exports to China exploded by 99% in 2025, reaching 90,906 metric tons (mt). Similarly, lobster imports hit a record 69,774 mt in 2025, a 14.7% YoY increase. This growth is driven by a structural pivot toward selective premiumization within food categories that the specific population of a region values, which in the case of China includes premium seafood.

In developed markets like North America and Europe, premiumization has become a survival strategy for brands operating in high-inflation environments. In the United States (US), despite food-at-home prices remaining nearly 30% higher than pre-2020 levels, households have not simply traded down. Instead, they have become more selective, prioritizing premium attributes in specific categories across all categories. They have adopted a two tiered purchasing strategy, switching to private-label or store brands for staples while splurging on categories that provide high emotional and health returns. Categories like high-protein foods and snacks are experiencing high growth. A 2025 Bain & Company survey found that 44% of US respondents said they want to increase their protein intake, up from 34% from the same period in 2024. Similarly, a study paid for by beef stick company Chomps found that protein snacks are growing at three times the rate of the overall US snacking industry, accounting for USD 24 billion in revenue in 2024.

Similarly, European consumers have adopted a less but better consumption model. This is evidenced by Europe holding a 29.4% market share of the global gourmet food market. An example of gourmet consumption in Europe is the fact that European cheese production was expected to increase in 2025 while milk production was forecast to decrease, indicating a pivot away from commodity products toward a focus on high value products, both for domestic consumption and export purposes. This trend is mirrored in South America, where Brazilian food output is leveling off in volume but shifting toward higher-value animal proteins and specialized crops to satisfy the premium quality standards of the global export market.

Sustainability and Ethical Sourcing as Global Trade Imperatives

Sustainability has continued to transition from a voluntary corporate social responsibility initiative to a mandatory prerequisite for market access in 2025. This structural shift is largely driven by a consumer base where individuals state that environmental concerns directly influence their purchasing habits. In Europe, the implementation of the European Deforestation Regulation (EUDR) has fundamentally redefined import demand profiles. The regulation requires geolocated evidence that commodities such as cocoa, coffee, soy, and palm oil are deforestation-free, creating a significant trade advantage for regions with advanced digital traceability. Conversely, regions lacking these transparency frameworks risk losing a significant share of the EU market. This could pose significant challenges for African countries, which collectively export around 45% of its coffee products and 60% of its cocoa products to the EU. Sustainability compliance has improved in recent years but is far from widespread, especially among smaller producers, who could find themselves locked out of markets such as the EU which require such compliance for market access. In Dec-25 the EUDR deadlines were extended by one year, stretching the deadline to Dec-26 for medium and large enterprises and to Jun-27 for small and micro enterprises, providing some breathing room for compliance.

In the US and Asia, the sustainability movement is manifesting through a surge in demand for eco-friendly packaging, both through consumer demand as well as government initiatives. According to Shorr’s 2025 Sustainable Packaging Consumer Report, which surveyed 2,016 American consumers, over half (54%) of respondents reported deliberately choosing products with sustainable packaging in the past six months, with 43% of consumers willing to pay extra for a product with sustainable packaging. Brands are responding to this consumer sentiment. For example, in Apr-25, Bubbies Ice Cream took a significant step toward sustainability with the introduction of its new certified home-compostable packaging. Bubbies introduced new paper pulp trays to replace its inside clamshell packaging, which is estimated to prevent 310 mt of plastic use annually. In India, as of Apr-25, the Indian government mandates that any new Polyethylene Terephthalate (PET) bottles contain at least 30% recycled plastic, encouraging brands, industries, and everyday citizens to rethink how they use, reuse, and value plastic. This initiative is an example of a government push initiative rather than a consumer pull initiative.

Conclusion

The 2025/26 trade landscape signals the continued transition from an era of food as a mere commodity to food as an expression of lifestyle and personal expression. The structural pivot toward convenience, functional health, selective premiumization, and mandatory sustainability has fundamentally rewired the global value chain. As snackification redefines meal patterns in Asia and protein-dense, functional products dominate Western aisles, exporters are being forced to trade volume for value and transparency. Sustainability, once a niche marketing tool, has matured into a strict license to operate, with regulations like the EUDR creating a need for digitally traceable supply chains. Moving forward, the success of agri-food stakeholders will depend on their ability to navigate this duality in the market: balancing the efficiency of production with the emotional and ethical expectations of a more conscious consumer base. Ultimately, global food trade is no longer just about feeding a growing population, it is about fueling specialized lifestyles and adhering to a new global standard of environmental accountability.