EU’s Sugar Production is Set to Increase After 4 Years

European Union’s (EU) sugar production is set to rebound in the marketing year (MY) 2021-22 that started in October 2021 and will end in September 2022. The region will record higher production due to lower temperatures and reduced cases of yellow virus among the sugar beet harvest. The production is going to rise for the first time in 4 years and is expected to record a YoY increase of 7.7% compared to the previous MY. MY 2020-21 was particularly bad for the crop due to the ban on neonicotinoids and warmer winter causing a high incidence of the yellow virus. According to S&P Global Insights, the sugar beet harvest was nearly complete by the end of December 2021 and the respective countries had already started coming out with projected estimates.

The USDA has forecasted that the sugar production for EU-27 in Raw Sugar Equivalents (RSE) will be 16.6 million mt. The higher production has come from increased production and harvest of sugar beet crops in France, Germany, and Poland. The production volumes might improve even more in the coming months as the main producing countries are anticipating favorable agro climate conditions. Even the forecasted sugar beet production for EU-27 in MY 2021-22, including for industrial use, has been revised up to 18.2 million mt RSE, a YoY increase of over 7%. Even though the outlook for the upcoming MY is positive, the sugar prices are touching new heights in the EU every day due to limited stock held with the sugar traders and processors. The carryover stocks from the MY 2020-21 crop were the lowest compared to the past five years, which is the main cause behind increasing domestic prices.

Source: European Commission.

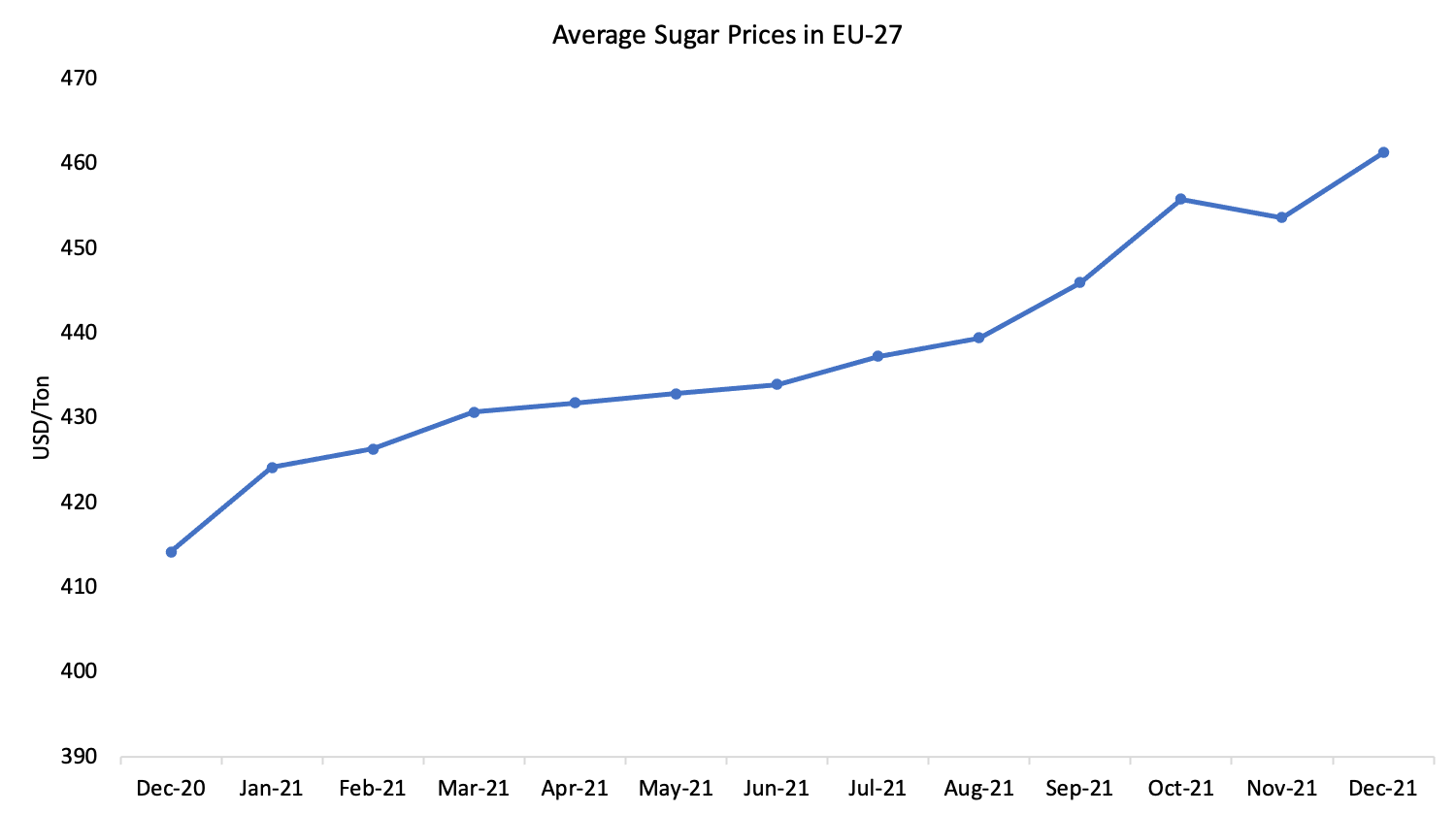

According to S&P Global Insights, due to limited supply, high energy prices, and unattractive freight rates, the sugar prices in the EU have been increasing at a very high rate since the past year. Higher domestic prices have also made the sugar processors and exporters a little reluctant to export as supply in the domestic market has become more profitable given the current market conditions. The demand and consumption of sugar in EU-27 is expected to recover from the COVID-19 outbreak but still remain below the pre-COVID-d19 levels.

The EU is also embarking on a program to reduce sugar content in food products by 10% by 2025. Food processors across the EU are responding to consumer and health authorities’ pressure to reduce sugar content in food and drinks through reformulating products. Looking ahead, it is hard to say if the demand for sugar will increase any more in the coming years. With a positive outlook for production and uncertainty in the consumption demand, EU-27 might end up exporting more sugar in the coming months compared to the previous MY.