Orange Harvests for Juice Production in 2023/24 Expected to Drop to Historic Low

Impact on Orange Markets and Global Trends

Due to a water deficit and high spring temperatures, the Spanish citrus season 2023/24 is predicted to reduce orange production dramatically, most notably in Andalusia. This will have a significant influence on the juice and processing industries. The Spanish juice industry typically relies on fresh fruit that does not fulfill commercial requirements. However, less fruit will be available in 2024, resulting in a lack of raw materials for the juice sector. As a result, the juice sector will have to compete on price with the fresh industry.

Oranges for juice making can be purchased for as little as EUR 0.35 to 0.40 per kilogram (kg), while at the same time, the wholesale price of fresh oranges-Navel-Navelina in Spain reached USD 1.33/kg in W4 of Dec-23, marking a 6.33% month-on-month (MoM) drop, according to Tridge price data. The scarcity is felt globally, with major producers like Florida and Brazil experiencing comparable difficulties. This has already been reflected in the price of orange juice futures, which have risen 119.20 USD/Lbs, or 57.75%, since the beginning of 2023. Orange juice index price previously touched an all-time high of 431.95 USD/Lbs on Oct-23, according to Trading Economics. The issue is expected to ease up before the end of December when the Navelinas are depleted. On the other hand, citrus production in the European Union (EU) is predicted to reach 9.9 million metric tons (mmt) in 2023/24, almost identical to the previous season. However, production of oranges and mandarins/clementines, which account for about 85% of the European Union's (EU) citrus crop, is expected to fall by -2% and -5% year-over-year (YoY).

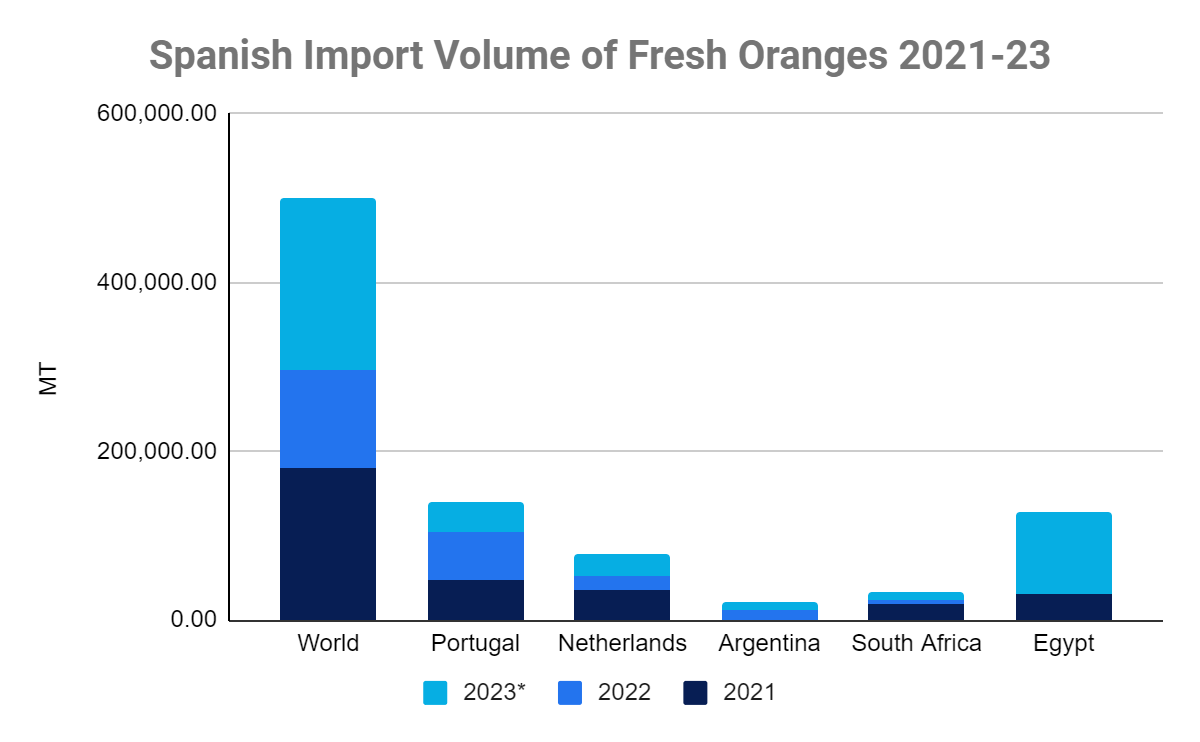

Figure 1: Spain’s Fresh Orange Import Volume 2021-2023

*2023 data are given for the first three quarters

Source: Tridge, TradeMap

Spanish Citrus Challenges: Adverse Weather and Surging Imports

Citrus production in Spain is anticipated to fall. This output decline results from a combination of drought, irrigation restrictions, and extremely high temperatures during the flowering and fruit-setting stages. Given the reduced estimated crop for the EU in 2023/24, fewer citrus fruits are expected to be allocated for processing. Following two seasons of inadequate local harvest, Spanish traders' import of Egyptian oranges has surged dramatically. Due to a lack of oranges in Spain, Spanish importers have resorted to importing directly from Egypt in 2023/24. Egypt’s orange trade volume has grown substantially, surging 48.25% since 2021, up to 97,453.88 metric tons (mt) in the first nine months of 2023.

Based on the current market trend, Tridge expects that the 2023/24 Spanish citrus season will have a historic low in orange production for juice production, owing to severe weather conditions and greater reliance on imports, mainly from Egypt. The global shortage of oranges for processing, which is reflected in rising prices for orange juice futures, emphasizes the gravity of the situation. While overall citrus production in the EU remains reasonably steady, the drop in orange and mandarin/clementine production indicates prospective industry developments. The combination of these factors underscores the pressing need for more raw materials in the juice sector and the growing pricing competition between the juice and fresh orange markets.