Potential Demand for Australian Barley in MY 2023/24 Amidst Disruptions in Global Barley Markets

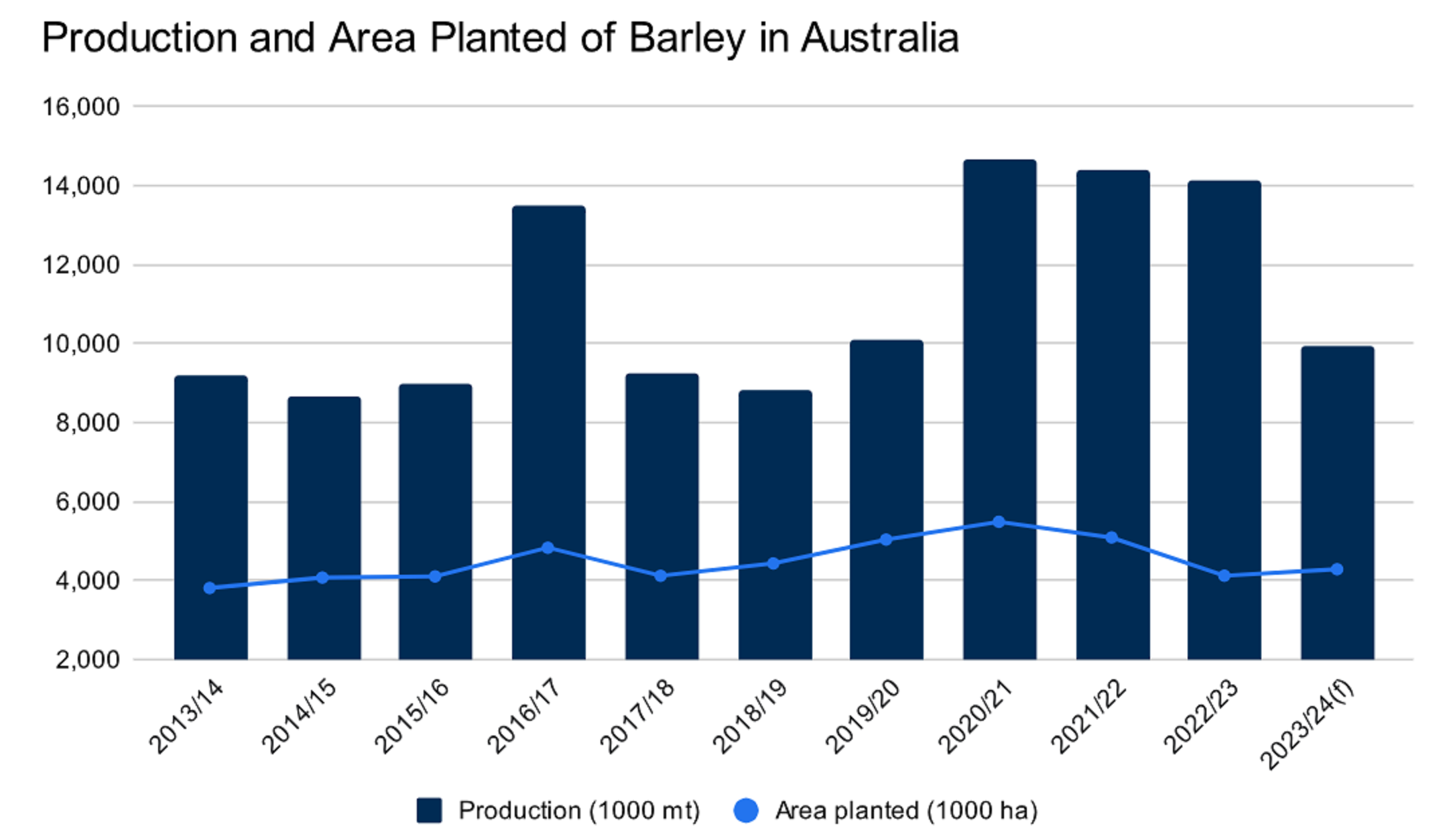

The Australian winter crops in MY 2023/24 are expected to remain above the 10-year average, with an area planted of 23.3 million hectares (ha). Planted from April to June, the Australian winter crop barley's planted area is set to increase by 4% YoY to 4.3 million ha in MY 2023/24. However, The Bureau of Meteorology has increased the probability of an El Niño occurring to 70%, three times higher than normal, which poses a significant risk to the Australian barley. Lower yield is estimated to decrease the production of Australian barley by 30% YoY to 9.9 mmt in MY 2023/24.

Source: ABARES

The projected reduction in barley production has significant implications for Australian barley exports in MY 2023/24. The United States Department of Agriculture's Foreign Agricultural Services (USDA FAS) estimates that Australia's barley exports in MY 2023/24 will decline to 5.5 mmt, representing a significant decrease of 2 mmt compared to the previous year. This decline can be attributed to the limited availability of barley for export due to the lower production levels.

While the reduction in production and export volume poses challenges, there are potential opportunities for Australian barley exports in the global market. The disruption in production and logistics caused by the Russian-Ukraine war and the uncertainty of The Black Sea Grain Initiative may increase demand for Australian barley. As Ukraine is a significant barley exporter, the market disruptions could lead to other countries seeking alternative sources of barley, such as Australia.

Moreover, China’s demand for barley is on the rise. China imported 1.28 mmt of barley in May 2023, an increase of 60% YoY. Total imports in the first five months of 2023 amounted to 3.97 mmt of barley, up by 19% YoY. The news about the potential re-entry of China as a major barley buyer could further bolster export demand if the import tariff on Australian barley is lifted. China had previously been the largest export market for Australian barley. Australian barley exports to China were worth USD 1.1 billion in 2018, the highest exports in the all-time year. However, in May 2020, China imposed an 80.5% import tariff on Australian barley, severely limiting exports to the country. Consequently, over the past three years after China imposed import tariffs, the majority of Australian barley exports have been diversified to other markets, with Saudi Arabia being the primary destination, followed by Japan and Vietnam.

The industry may face challenges due to reduced production and export volumes resulting from lower yields. However, the disruptions in other major barley-exporting markets and the potential re-entry of China into the market are expected to create a firm demand for Australian barley exports. Despite Australian export volume being expected to reduce by 27% YoY to 5.5 mmt, export value for this year projects an upward trend to USD 2.42 billion, 7% higher than the previous year.