US bell pepper producers angry over the USMCA

The US Mexico Canada Agreement (USMCA), also known as the modernized version of 26-year-old NAFTA, is a trade agreement that includes, among others, agricultural provisions on market access, ag biotechnology, and trade distortions. In this agreement, the US mainly targets promoting fair trade and increasing exports of its agricultural products. Expressly, under the trade distortion avoidance condition, tariffs between the US and Mexico are set at zero, and all trade-distorting methods are banned unless in the form of domestic support measures.

Reasons behind US bell pepper producers’ anger

This new agreement has called in furious reactions from US bell pepper producers mainly in Florida and Georgia, the two major bell pepper producing regions. As reported on Tridge commentary, Florida’s Agriculture Commissioner is currently pushing for an investigation to be done on Mexican bell pepper imports. Over the years, US bell pepper producers repeatedly claimed that they were at an unfair market disadvantage, with most of the market dominated by Mexican imports.

In the case of Mexican bell peppers, it enters the US market at a price lower than Florida and Georgia’s production costs. This is possible due to lower labor costs in Mexico, which is estimated to be one-tenth of the U.S. The Mexican government also provides subsidies that equip the farmers with greenhouses and high tunnels for higher productivity. With the USMCA in force, US bell pepper farmers are demanding the agreement to include protective measures for them, most probably in the form of tariffs.

Source: Tridge, USDA

Current US bell pepper market

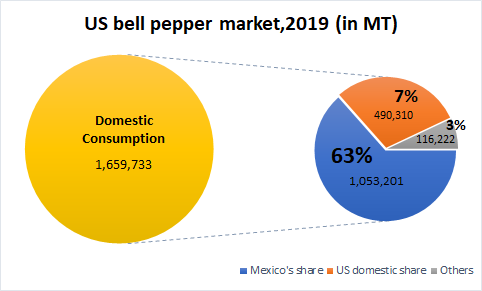

The U.S market shows high consumer demand for bell peppers, with 1.66 million MT consumed domestically in 2019, which includes both domestic production and imports. The amount of exported bell peppers constituted only 20% of the US's total production for 2019, leaving 80% for domestic consumption. However, the problem lies in the domestic bell pepper market’s over-dependence, where 63% of its share is dominated by Mexican bell peppers, with US bell pepper producers providing only 7% of the consumption share.

The decreasing market share of US bell pepper is evident in the change of acres of land harvested. From 2000 to 2019, the acre of land used for bell pepper harvest decreased by 38%, from 62,080 to 38,300 acres (USDA, 2019). As a result, the total production of bell pepper in the US declined by 28%, from 857K MT in 2000 to 616K MT in 2019 (USDA NASS, 2019). On the other hand, Mexico’s production area reported a compound annual growth rate (CAGR) of 28% from 2007–2017. This naturally led to a decrease in Florida and Georgia’s contribution to the market.

Two sides to the US bell pepper market

However, reduced total production may not be solely attributable to smaller harvested land. In 19 years’ time (2000-2019), the US’s yield per acre increased by only 16%, well below the average agricultural productivity growth of 20% (computed from USDA data). Considering bell pepper is one of the top 5 agricultural products in the US, the 16% increase was disappointing. Thus, the low productivity growth coupled with smaller land harvested could not compete with a 56% import increase from Mexico in a shorter period of time (IFAS, 2019). However, despite how devastating the situation sounds, the US remains a giant producer of bell pepper wherein 2019 bell pepper production of the US (616K MT) was ten times Mexico’s production (60.71K MT). Nonetheless, with the US farmers’ lives and the future of agricultural trade at stake, the US government is left with an important decision to make.

Possible Scenarios

Here are some scenarios based on government decisions and possible price implications:

Case A: US farmers’ demand accepted

Assuming the court accepts the US bell pepper producers’ accusations of Mexico’s anti-dumping practices, the most probable action would be imposing tariffs on these products. Although this may satisfy the US bell pepper producers at the moment, the tariffs will discourage Mexican producers from exporting to the US, and even the ones that continue to export will enter at a higher price due to the tariffs. Under this scenario, upward pressure is placed on bell pepper prices for US importers and consumers due to a decrease in supply and an increase in import prices. This is expected to intensify before and after the US’ peak bell pepper, from April to July, when local production slows down. However, with President Biden expressing positive sentiments over the USMCA and phase I, the implementation stage, being completed on December 31, 2020, this scenario is less likely to happen.

Case B: Retain current USMCA but provide domestic support and subsidies

Another scenario is to push through with the current USMCA conditions but with financial provision or subsidies for domestic bell pepper producers. Financial assistance from the government could help improve the productivity of local bell pepper producers, thus better preparing them to compete alongside Mexican products. Moreover, this could help upgrade the crops to premium products, such as organic bell peppers, and maximize US consumers’ tendency to favor these qualities. Increased productivity and product differentiation could help stabilize the US bell pepper market price by softening price tensions between the US and Mexico. Aside from price stabilization, this may also assuage the anger among US bell pepper producers.

Case C: No action taken

The last scenario entails the US government proceeding with the current USMCA. Under this case, there is a high chance of a more serious outroar from US bell pepper producers alongside different organizations such as the Florida Farm Bureau. Aside from potential social unrest, the US’s share of its bell pepper market will continue to decline, resulting in job losses and higher dependence on Mexican imports. This overly dependent market will leave the US bell pepper sector seriously vulnerable to supply disruption and other external risks in the long run.

Sources

- Naples Daily News. “Florida farmers continue to raise alarms as NAFTA rewrite nears passage”

- Tridge. Bell pepper produced in Mexico in MT

- Tridge. “US: Florida requests International Trade Commission to review bell pepper imports”

- University of Georgia. “Policy Brief: The impact of the USMCA on Georgia’s Small Fruit and Vegetable Industries”

- USDA NASS. Peppers,bell production measured in cwt

- USDA NASS. Peppers,bell land harvest in acre

- USDA Summary of Recent Findings