W16 2025: Wheat Weekly Update

.jpg)

In W16 in the wheat landscape, some of the most relevant trends included:

- In 2025, wheat acreage in Western Australia will decrease by 9%, down to 4.19 million ha, due to limited land availability and dry conditions in the northern regions. However, adequate rainfall in May-25 could help maintain planting levels similar to last year’s total.

- Egypt's wheat harvest will rise to 10 mmt in 2025, driven by improved yields and land reclamation. In contrast, Pakistan's wheat production will drop by 13% to 27.5 mmt due to reduced acreage and dry weather, impacting imports.

- In Russia, prices remained stable despite a decline in exports. US prices increased WoW, driven by adverse weather and strong global demand, while Ukrainian prices surged due to a reduced harvest forecast for 2024/25.

1. Weekly News

Australia

Western Australia Wheat Area Down 9% YoY in 2025

Wheat acreage in Western Australia will shrink by about 400 thousand hectares (ha), or 9% year-on-year (YoY), in 2025. The Grain Industry Association of Western Australia (GIWA) projects farmers will sow 4.19 million ha of wheat, down from 4.59 million ha in 2024. This drop mainly reflects the limited availability of lands, which many growers used in 2024 but cannot access for the new season. While soil moisture remains adequate in the state’s southern regions, the northern areas will face dry conditions. GIWA stated that with sufficient rainfall on May-25, farmers could plant up to 9 million hal.

In 2024, Western Australia harvested 12.45 million metric tons (mmt) of wheat, marking its third-largest crop. The state exports most of its grain, with sowing typically occurring between April and June and harvesting in the final months of 2025. Nationally, analysts expect Australia’s total wheat production for 2025/26 to fall by around 16% due to persistent drought in several major growing regions. They forecast output at 28.6 mmt, below the Mar-25 projection of 30.5 mmt.

Egypt

Egypt's Wheat Harvest Outlook and Agricultural Plans for 2025

Egypt’s Minister of Agriculture and Land Reclamation projected that the country would increase its wheat harvest for 2025, forecasting 10 mmt, up from 9 mmt in 2024. Improved crop yields and large-scale land reclamation projects will drive this growth. Farmers plan to cultivate 1.30 million ha of wheat in 2025, slightly smaller than the 1.34 million ha for 2024, indicating a potential minor reduction in the wheat-growing area. While wheat remains a staple crop, farmers find it less profitable than alternatives like beet.

To ensure food security, the Egyptian government plans to import 6 mmt of wheat and procure 4 mmt of local wheat to supply heavily subsidized bread to over 69 million people. The Agricultural Research Center's development of newer, high-yield wheat strains has boosted productivity, increasing wheat yields by 7 to 8.5% YoY and supporting overall growth in harvest expectations.

Pakistan

Pakistan’s Wheat Output to Drop 13% in 2025/26

Pakistan’s wheat production for the 2025/26 season will drop by 13% to 27.5 mmt, falling from the record 31.6 mmt produced in 2024/25. Farmers have reduced the cultivation area, and dry weather has further impacted yields. The government has also fueled the downturn by discontinuing wheat procurement at guaranteed prices. Analysts forecast domestic wheat consumption to rise slightly YoY to 31.9 mmt. Estimates place wheat imports at 1.7 mmt, although the actual volume will depend on the harvest’s outcome. As of Mar-25, the government maintains a ban on wheat imports; any future imports will require official approval and a decision on whether to involve the private sector or assign the task to the state-run Trade Corporation of Pakistan. Authorities continue to liberalize the wheat market by removing support prices and ending public procurement and distribution. Meanwhile, wheat and wheat flour prices in Mar-25 were 35% lower than the peak levels recorded a year earlier.

Ukraine

USDA Increases Ukraine’s Wheat Export Forecast for 2024/25

The United States Department of Agriculture (USDA) raised its forecast for wheat exports from Ukraine in the 2024/25 marketing year (MY) but downgraded its expectations for barley Apr-25. The USDA expects wheat exports to reach 16 mmt, nearly 500 thousand metric tons (mt) higher than Apr-25's preliminary estimates. The USDA’s wheat production forecast remains unchanged at 23.4 mmt. For the global wheat harvest in MY 2024/25 , the USDA projects a total of 796.85 mmt, a decrease of about 380 thousand mt. The USDA also forecasts wheat trade to reach 203.5 mmt, down by 3.8 mmt.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W16 2024 to W16 2025)

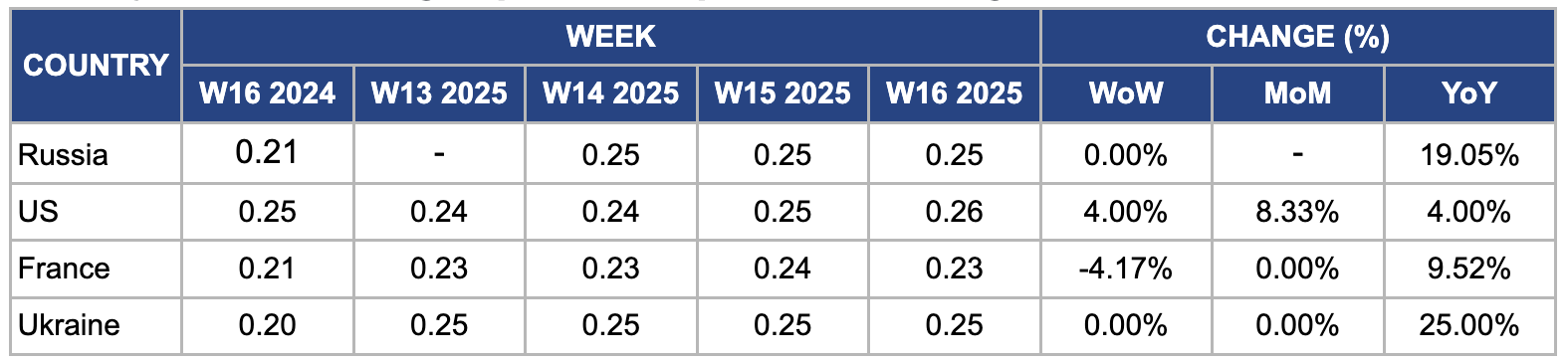

Russia

In W16, Russian free-on-board (FOB) wheat prices remained stable for the third consecutive week at USD 0.25 per kilogram (kg), with a notable 19.05% increase YoY. However, Russia's share of the global wheat market is expected to decline, with projections indicating a drop to 20% by the end of the 2024/25 agricultural season. This decrease is due to lower harvests, reduced profitability for exporters, and strong wheat yields from competing countries. Key challenges affecting Russia's wheat exports include a quota limit, a strong ruble, and farmers' reluctance to lower prices. These factors, combined with a downturn in export volumes, weighed heavily on the wheat sector. In Mar-25, Russia exported only 1.78 mmt of wheat, which is a significant decline, 2.9 times lower than the same period in the previous year. They observed a decrease in export volume in shipments to 21 countries, including key wheat buyers such as Egypt, Bangladesh, and Sudan.

United States

In W16, US free-on-board (FOB) wheat prices rose by 4% week-on-week (WoW), 8.33% month-on-month (MoM), and 4% YoY, reaching USD 0.26/kg. This price increase is primarily due to adverse weather conditions in key wheat-producing states like Kansas and Oklahoma, which have experienced drought and unseasonably warm temperatures, leading to concerns about reduced yields in the 2025/26 season. Moreover, stronger global demand, particularly from Egypt, Türkiye, and Sub-Saharan Africa, has further supported export demand, contributing to the upward price movement.

France

In W16, wholesale wheat prices in France averaged USD 0.23/kg, marking a 4.17% WoW decline due to tightening supply expectations and weather-related risks to the 2025 wheat crop. Persistent wet conditions in key wheat-growing regions like Hauts-de-France and Grand Est have delayed spring fieldwork, with only 80% of the planned soft wheat area planted by early April, compared to 95% at the same time last year. Moreover, concerns over fungal diseases caused by excess moisture have raised doubts about yield potential and quality. Despite these challenges, steady demand from North African countries such as Algeria and Morocco has helped maintain export activity.

Ukraine

In W16, Ukraine’s FOB wheat prices averaged USD 0.25/kg, unchanged from the previous week and month but reflecting a 25% YoY increase. This surge is mainly due to reduced wheat output in the 2024/25 season, with the Ukrainian Grain Association forecasting a decline to 19.2 mmt from 22.5 mmt in the previous year. The decrease is due to a reduction in sown area, estimated at 4.2 million ha in 2025, compared to 4.7 million ha in 2024, as farmers shifted to more resilient or higher-margin crops due to geopolitical and logistical challenges. Despite these factors, strong demand from traditional buyers like Egypt and Türkiye has helped maintain price stability. Meanwhile, Black Sea shipping risks and higher freight and insurance costs have supported firmer FOB prices.

3. Actionable Recommendations

Diversify Export Markets and Strengthen Strategic Partnerships

Russia and Ukraine, two major wheat exporters, experienced geopolitical tensions, unfavorable weather conditions, and reduced export volumes. Both countries should focus on diversifying their export markets to mitigate these risks. Expanding trade agreements with emerging markets, particularly in Africa and Southeast Asia, could provide stability as traditional markets like Egypt and Bangladesh face supply challenges. Strengthening relationships with existing trade partners through long-term contracts or bilateral agreements could also help stabilize wheat exports. Furthermore, both countries should invest in infrastructure improvements, such as port facilities and transport logistics, to ensure that wheat reaches global markets efficiently, despite challenges like Black Sea shipping risks.

Implement Advanced Weather-Resilient Farming Practices

In regions like France and Pakistan, adverse weather conditions such as drought, excess moisture, and irregular temperatures pose risks to wheat yields. To safeguard against these unpredictable weather patterns, it is crucial to implement advanced weather-resilient farming practices. For example, using drought-tolerant wheat varieties, optimizing irrigation systems, and employing precision agriculture technologies like satellite weather monitoring could help mitigate adverse weather impacts. In France, addressing fungal diseases caused by excess moisture could involve adopting disease-resistant wheat strains or enhancing crop rotation practices to reduce the risk of soil-borne infections. For Pakistan, improving water management techniques and introducing soil health initiatives could help farmers adapt to the effects of drought and maintain stable yields.

Incentivize Local Wheat Production and Improve Domestic Supply Chains

Despite an expected increase in wheat harvests, the Egyptian government still relies on local procurement and imports to meet national wheat demand, particularly for subsidized bread. To enhance food security and reduce dependency on imports, Egypt should incentivize local wheat production through subsidies, tax incentives, and providing access to improved seeds and farming technologies. The government could also invest in domestic supply chains, ensuring better storage, transportation, and distribution systems. These measures would enable farmers to achieve consistent yields, reduce post-harvest losses, and make local wheat more competitive against imports.

Sources: Tridge, Agri, UkrAgroConsult