.jpg)

1. Weekly News

India

India Considers Tighter Sugar Export Restrictions Amid Production Decline and Price Concerns

The government of India may further tighten the ban on sugar exports due to falling production and fears of price hikes induced by shortages. Initially, the 2022/23 sugar year (October-September) had a restricted export limit of 6 million metric tons (mmt), with 6.1 mmt already contracted. The new plan may halt the export of approximately 85 thousand mt yet to be shipped. As of W23, 6.02 mmt have been dispatched. Ex-mill sugar prices have stabilized after recent surges, but the government remains cautious amid reduced production estimates. India's sugar output is projected at 32.7 mmt, down from 35.9 in 2023, with significant drops in Maharashtra and Karnataka. The government prioritizes domestic availability, ethanol production, and buffer stocks, with no additional export quotas expected this year. India's sugar exports in FY-23 reached a record-high value of USD 577.1 billion, cementing its status as a top global producer and exporter.

Australia

Industrial Disputes Threaten Australia's Sugar Harvest and Production

Industry experts warn that disputes at industrial factories responsible for over half of Australia's sugar production could leave cane unharvested if unresolved soon. Strikes over pay at eight mills owned by Wilmar International and a ninth mill owned by China Oil and Foodstuffs Corporation (COFCO) have delayed cane crushing operations by up to 13 days. Despite Australia being the world's fourth-largest sugar exporter, a small production reduction would tighten Asian supply without significantly affecting global prices. The strikes, if prolonged, could shorten the processing season, reducing the time to harvest cane and threatening sugar content. Unions at Wilmar and Tully mills are demanding pay rises, with negotiations ongoing. The sugar industry remains concerned as the crushing season progresses.

Ukraine

Ukraine Exports 421.8 Thousand MT of Sugar in 2024, Reaching EU Quota Limits

Since the beginning of 2024, Ukraine has exported 421.8 thousand metric tons (mt) of sugar, with 301 thousand mt directed to European Union (EU) countries. The Acting Minister of Agrarian Policy and Food discussed sugar exports in a meeting, reviewing compliance with the Memorandum of Understanding between the Ministry and the National Association of Sugar Producers of Ukraine (Ukrsugar) and a government decree implementation establishing a zero quota for sugar exports to the EU effective June 1, 2024. Since the Memorandum's implementation in Sep-23, 665 thousand mt of sugar have been sold, with 158.5 thousand mt sold in May 2024 alone. Of this, 110.5 thousand mt were exported, including 72 thousand mt to the EU. The domestic market saw over 48 thousand mt sold at an average price of USD 0.61 per kilogram (UAH 24.6/kg).

A Memorandum of Understanding, signed in Nov-23, regulates sugar export volumes at 750 thousand mt per marketing year (MY). New rules for duty-free and quota-free trade in agricultural products with the EU came into effect on June 5, setting quotas for several products, including sugar. Ukraine has already exhausted its sugar export quota to the EU, which stands at 262 thousand mt.

South Africa

South Africa Sugar Tax Adversely Affects Small-Scale Farmers, Suppresses Market, and Causes 16 Thousand Job Losses

The South African Canegrowers Association (SA Canegrowers) reports that South Africa's sugar tax is adversely affecting small-scale farmers' livelihoods, suppressing the market for locally produced sugar, and resulting in over 16 thousand job losses in the industry. Implemented in 2018 as the Health Promotion Levy, the sugar tax targets drinks with more than 4g of sugar per 100ml. South Africa, a significant sugar producer ranking among the top 15 globally, relies heavily on the industry, with one million livelihoods dependent on it. Despite facing challenges such as prolonged drought and cheap sugar imports, the industry now contends with the sugar tax's economic impact. Canegrowers stress the need to remove the tax to foster investment and support the industry's transformation.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W23 2023 to W23 2024)

.png)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

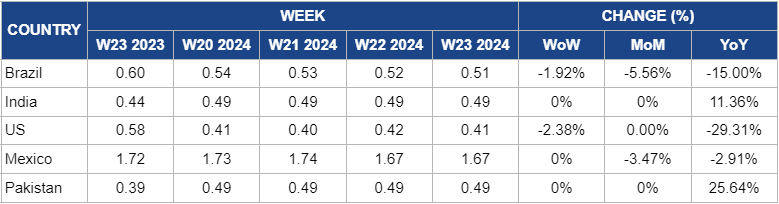

Brazil

Brazil's sugar prices slightly decreased by 1.92% week-on-week (WoW), reaching USD 0.51/kg in W23. Driven by the depreciation of the Brazilian real against the dollar, which encourages export selling by Brazilian sugar producers. In addition, a decline in crude oil prices to a 3-3/4 month low could further impact sugar prices, as weaker crude prices may prompt more sugar production instead of ethanol production, thereby increasing sugar supplies. Furthermore, increased sugar production in Brazil presents a bearish outlook for prices.

India

Sugar prices in India remained stable for the fourth consecutive week at USD 0.49/kg, with no WoW and month-on-month (MoM) changes, marking an 11.39% year-on-year (YoY) increase. This YoY increase can be due to India's ban on sugar exports to stabilize the domestic market in the 2023/24 season.

United States

The United States (US) experienced a price decrease to USD 0.41/kg in W23, marking a 2.38% WoW and a 29.31% drop in sugar prices. Sugar beet planting in the United States has had a promising start, with favorable conditions contributing to early crop development. As of mid-May, farmers growing in Minnesota had planted 97.5% of their 413,833-acre crop, thanks to early planting dates and timely rains which have replenished soil moisture and supported herbicide activation. In Colorado and Nebraska, growers faced strong winds and soil crusting, necessitating some replanting. Despite these issues, adequate snowpack from the past winter has ensured sufficient irrigation water. Overall, sugar beet crops across key growing regions in the US are developing well as of W23, setting a positive outlook for the season.

Mexico

Mexico's sugar prices remained unchanged in W23, at USD 1.67/kg. Sugar prices in Mexico fell by 3.47% MoM, marking the third consecutive month of declines. This drop brought prices to their lowest level since Jan-23. The decrease was attributed to the new harvesting season in Brazil, bolstered by favorable weather conditions that improved the global supply outlook.

Pakistan

Pakistan's sugar prices remained stable at USD 0.49/kg, with no changes in WoW or MoM, but experienced a 25.04% YoY increase from USD 0.39/kg in W23 2023. Furthermore, sugar prices are forecasted to increase in the coming weeks due to new crops and increased production.

3. Actionable Recommendations

Strengthen Export Controls and Production Monitoring

In response to India's potential tightening of the sugar export ban due to falling production and fears of price hikes induced by shortages, it is crucial to enforce stricter export controls to prevent the shipment of the remaining 85,000 metric tons. This will help ensure domestic supply stability. Additionally, closely monitoring sugar production levels in key regions like Maharashtra and Karnataka will allow for better anticipation and mitigation of potential shortages. Enhancing production monitoring and prioritizing ethanol production can further utilize sugarcane efficiently, supporting domestic sugar availability.

Review Sugar Tax Impact and Support Industry Transformation

In South Africa, the adverse effects of the sugar tax on small-scale farmers and the overall sugar industry need to be thoroughly reviewed. Conducting a comprehensive review of the sugar tax's impact can guide potential revisions or abolition to support the industry. Encouraging investment in modernizing sugar production practices will enhance competitiveness in the global market and foster industry transformation, helping to sustain livelihoods dependent on sugar production.

Promote Early Planting Practices and Ensure Adequate Irrigation

In the United States, the promising start to sugar beet planting, supported by favorable conditions, underscores the importance of promoting early planting practices. Early planting reduces risks associated with adverse weather conditions and enhances crop yields. Ensuring the efficient use of winter snowpack for irrigation needs is crucial for sustaining healthy sugar beet crop development and setting a positive outlook for the season.

Sources: Tridge, Reuters, Ukrinform, Beverage Daily, Business Standard