.jpg)

1. Weekly News

Europe

Europe's Wheat Harvest Expected to Be the Smallest Since 2020

Europe's 2024 wheat harvest is expected to be the smallest since 2020, despite Spain's recovery from drought and good yields in Bulgaria and Romania. The wheat harvest in France is accelerating, but persistent rains have significantly impacted the quantity and quality of wheat across Europe. Concerns are rising as the wheat crop's condition has deteriorated to its worst since 2016, with projections indicating it could be the lowest since the 1980s. In Germany, the wheat harvest decreased by 6.2% year-on-year (YoY) to 20.2 million metric tons (mmt) compared to the previous year, with concerns that continued rain could further affect wheat quality.

Argentina

Argentina's Wheat Sowing Nears Completion with Improved Crop Conditions

According to the Buenos Aires Grain Exchange (BAGE), Argentina's wheat sowing was completed on 98.5% of the planned 6.3 million hectares (ha) as of July 25. The current crop conditions show 55% satisfactory, 39% good to excellent, and 6% poor to very poor condition, representing an improvement from the previous year when 26% of crops were in good to excellent condition, 63% were satisfactory, and 11% were poor to very poor.

Brazil

Paraná, Brazil's 2023/24 Wheat Harvest Forecasted at 3.6 MMT

The 2023/24 wheat harvest in Paraná, Brazil, is now estimated at 3.6 mmt, about 200 thousand metric tons (mt) lower than the forecast from Jun-24, according to the Department of Rural Economy (Deral). This adjustment reflects a 1% YoY decrease from the previous year’s production, influenced by dry weather in Jun-24.

Egypt

Egypt Maintains Strong Wheat Import Reliance on Russia for 2024/25 Season

Egypt imported 12.2 mmt of wheat in the 2023/24 season, with 71% of this volume (8.7 mmt) sourced from Russia. Other sources included 1.7 mmt from Ukraine, 1 mmt from Romania, 450 thousand mt from France, 250 thousand mt from Bulgaria, and 100 thousand mt from the United States (US). Egypt is expected to maintain its import levels of around 12 mmt for the upcoming season. In a recent General Authority for Supply Commodities (GASC) tender on July 16, Egypt secured 770 thousand mt of wheat for delivery in the 2024/25 season, with 710 thousand mt sourced from Russia, underscoring Russia's ongoing dominance in Egypt's wheat supply despite global harvest fluctuations.

Hungary

Hungary's 2024 Wheat Crop Nears 5 MMT, Exceeding Domestic Demand

As the harvest concluded, Hungary's wheat crop for 2024 is close to 5 mmt, according to the state secretary of the Agriculture Ministry. This year's yield will exceed the domestic demand of around 3 mmt. In 2023, Hungarian farmers harvested slightly over 5.9 mmt of wheat, based on data from the Central Statistical Office (KSH).

United States

Illinois Winter Wheat Harvest Concludes Successfully Ahead of Five-Year Average

The US Illinois winter wheat harvest is complete, with a notably successful crop. The USDA's latest crop report indicates that the wheat harvest finished ahead of the five-year average. While there were some concerns about vomitoxin levels, overall yield was satisfactory, though quality was affected by late moisture.

2. Weekly Pricing

Weekly Wheat Pricing Important Exporters (USD/kg)

Yearly Change in Wheat Pricing Important Exporters (W30 2023 to W30 2024)

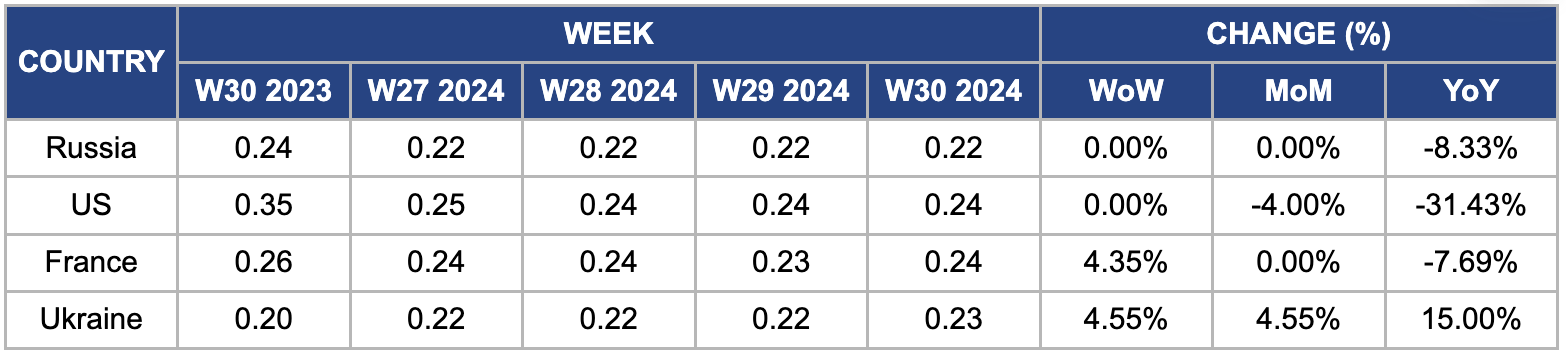

Russia

In W30, Russian wheat prices remained at USD 0.22 per kilogram (kg). However, prices declined 8.33% YoY, attributed to unfavorable global market conditions and a strengthening Russian ruble. The new wheat harvest is progressing smoothly, with seasonal increases in new wheat supplies as the peak harvest season approaches. Notably, Russia's share in world wheat exports has increased significantly. According to International Grain Council (IGC) estimates, Russia exported 55.3 mmt of wheat by the end of the 2023/24 season, exceeding the Jun-24 forecast of 53.1 mmt. This export volume is the highest in Russia's modern history and is almost 15% higher than the previous season. Consequently, Russia's share in world wheat exports rose to a record 26.1%.

United States

In W30, United States (US) wheat prices remained steady at USD 0.24/kg despite experiencing a 4% month-on-month (MoM) decline. The MoM drop is because the US wheat production outlook remains positive due to dry conditions that advanced harvest. By June 23, about 40% of the winter wheat crop had been harvested, with crop conditions improving to 52% from last year's 40%. Spring wheat conditions are also favorable, with 71% rated good or excellent, a 21% improvement from the previous year.

France

In W30, French wheat prices increased by 4.35% week-on-week (WoW) to USD 0.24/kg from USD 0.23/kg in W29. This increase is due to harvest damage from persistent rain in France in summer. Moreover, French soft wheat ratings fell again in the week to July 22, with only 50% in good or excellent condition, down from 52% the previous week, and harvesting remains well behind average, reducing yield. The latest estimates for this campaign's soft wheat output are between 26.2 and 29.5 mmt, compared to 35.2 mmt in 2023.

Ukraine

Ukrainian FOB wheat prices rose by 4.55% WoW and month-on-month (MoM) to USD 0.23/kg in W30, reflecting a significant 15% increase YoY. This price increase is due to high importer demand, limited producer supply, low transitional stocks, and adverse weather affecting late crop harvests. The agriculture ministry forecasts a 2024 wheat harvest of 19 mmt, down from 22.2 mmt in 2023, with expected wheat exports decreasing to 14 mmt from 18 mmt in the 2023/24 season. Additionally, farmers sowed a smaller area of winter wheat last autumn. Moreover, food wheat prices in Ukraine are expected to rise for the 2024/25 (July-June) season due to a reduced exportable surplus caused by a decline in harvest and carryover stocks. The Agrarian Council of Ukraine predicts a reduction in export potential by 2 to 3 mmt, leading to higher wheat prices.

3. Actionable Recommendations

Implement Advanced Weather-Resilient Farming Techniques

France, Germany, and Ukraine should focus on enhancing quality and yield management strategies to mitigate the impact of adverse weather conditions on wheat production. Investing in weather-resistant wheat varieties, improving harvesting techniques, and adopting advanced quality control measures can help address the challenges posed by persistent rains and adverse weather. These improvements will benefit global wheat markets, including major importers such as Egypt, which relies on stable wheat supplies. Enhanced quality and yield management in these key producing countries will help stabilize global wheat prices and reduce market volatility, ensuring consistent supply for importing countries.

Strengthen Regional Wheat Supply Chains

Egypt, Argentina, and Brazil should strengthen their regional wheat supply chains to enhance resilience against global harvest fluctuations. This includes building better storage facilities, improving transportation infrastructure, and establishing strategic reserves to buffer against supply disruptions and price volatility. Strengthened supply chains will benefit countries heavily reliant on wheat imports, like Egypt, by ensuring a more stable and reliable wheat supply. Additionally, Argentina and Brazil will benefit from reduced export constraints and improved market access.

Enhance Collaboration on Global Wheat Research

France, Russia, and Argentina should enhance collaboration on global wheat research to develop higher-yield and disease-resistant wheat varieties. Partnering with international research organizations and sharing knowledge can drive advancements in wheat breeding and farming practices. This collaborative research will benefit wheat-importing countries by increasing the availability of resilient wheat varieties and stabilizing global wheat supplies. It will also help mitigate the impact of climate change and adverse weather on wheat production.

Sources: Brownfield Ag, AgroForum, Portal Do Agronegócio, Zol, Milk News, UkrAgroConsult, Pleinchamp, Hellenic Shipping News, Farmer.pl