W36 2024: Maize Weekly Update

1. Weekly News

Argentina

Disease Outbreak Causes Major Corn Production Setback in Argentina

Argentina's corn production is experiencing a significant setback due to an outbreak of corn stunting disease caused by the bacterium Spiroplasma kunkelii, which is transmitted by the leafhopper. Originally contained in the northern regions, the disease has now spread southward, impacting corn crops in Central Argentina and parts of the Pampas region. This outbreak has led to delays in input sales and lowered planting expectations, potentially resulting in a production shortfall of around 18 million metric tons (mmt). Even with favorable weather conditions, most planting could face climatic risks, mainly due to potential rainfall shortages in the crucial Dec-24 to Jan-25 period. As of August 15, 2024, the Rosario Stock Exchange has projected Argentina's total corn production to be 49 mmt, marking an 18 mmt reduction from earlier estimates due to the disease outbreak.

Brazil

Brazil's 2024/25 Summer Corn Planting Progress Doubled in W36

As of August 29, the first 2024/25 corn crop sowing, also known as summer corn, has progressed to 8% of the expected area in the center-south region of Brazil. This represents a doubled progress compared to 4% in W35, but it remains below the 13% recorded during the same period in 2023. Rio Grande do Sul traditionally leads the planting efforts, but Santa Catarina and Paraná have also started sowing this year, aiding the region's overall progress. However, planting could have advanced more if it weren't for irregular humidity levels and low temperatures at the beginning of W35. While some areas observed frost formation, impact has been minimal, as most crops were still in the early emergence phase, with no significant damage reported.

Brazil's Corn Exports in Sep-24 Forecasted at 5.4 MMT

Brazil corn exports are forecasted to reach 5.4 mmt in Sept-24, marking a significant decline of nearly 4 mmt compared to Sep-23. This reduction is due to smaller harvests caused by adverse climate conditions and heightened competition from Argentina, which is witnessing a strong recovery in its export capacity. Despite the decrease, Brazil's 2024 corn exports remain noteworthy, especially compared to 2023, a record-setting year for the country's exports following its largest-ever harvests.

Nigeria

High Yields in Katsina Offset Declining Corn Acreage in Nigeria Amid Rising Input Costs

Despite rising input costs and ongoing instability, Nigeria's corn yields will offset the smallest planted area in nearly 15 years. The area under harvest for the 2024/25 agricultural season has fallen to 5.1 million hectares (ha), the lowest since 2010/11. However, corn yields in Katsina State, Nigeria's second-largest corn-producing region, in Aug-24 reached their highest levels since 2019. While crop health in other areas remains stable or slightly lower, overall production for 2024/25 is projected to remain comparable to last year despite the reduced planted area. Nigeria has been losing corn acreage to rising input costs and insecurity, but improved yields are expected to compensate. This production stability would be a positive outcome, especially as other African nations like Ghana and Southern Africa struggle with crop shortages due to drought.

Ukraine

Ukrainian Corn Export Potential Set to Decline by 11 MMT in 2024

Ukraine will see a significant decrease in agricultural exports in 2024, with corn exports expected to drop by 11 mmt compared to the previous year. The reduction stems from a nearly fourfold decrease in corn planting areas, driven by high investment costs per ha. Consequently, the export potential for corn this year is projected at 18.5 mmt, down from 29.5 mmt in 2023. Despite this reduction, substantial demand for Ukrainian corn will persist. China is anticipated to remain a key market for Ukrainian exports, followed by North Africa, Western Europe, Turkey, and the Middle East, despite ongoing risks in the Red Sea.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

* Varieties: US (feed grade), all others (overall average)

Yearly Change in Maize Pricing Important Exporters (W36 2023 to W36 2024)

* Varieties: US (feed grade), all others (overall average)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

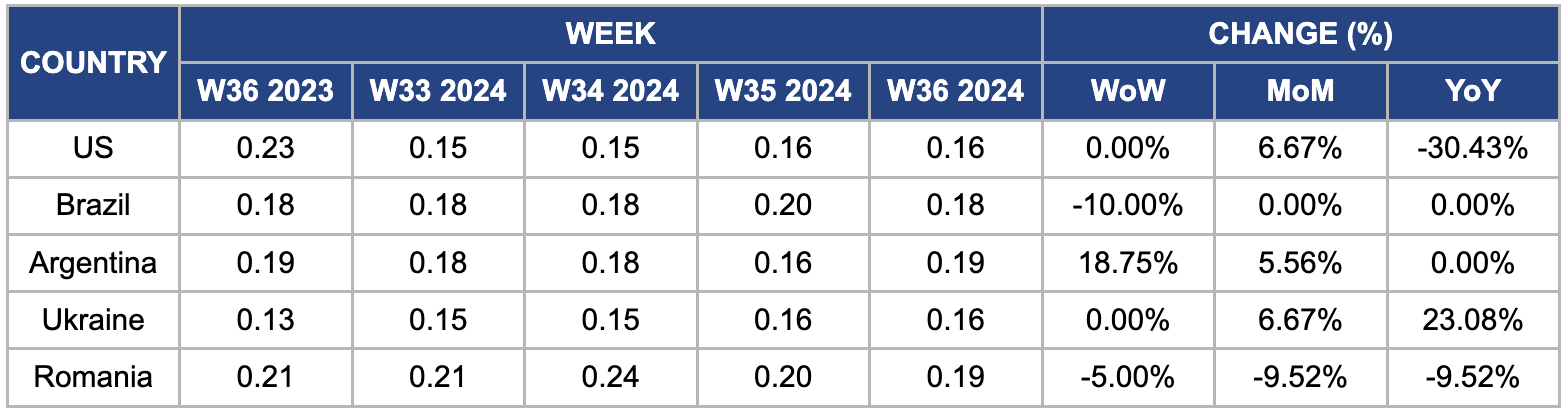

US

In W36, wholesale maize prices in the United States (US) remained stable week-on-week (WoW) at USD 0.16 per kilogram (kg). However, prices increased by 6.67% month-on-month (MoM). This price increase is due to higher demand following new export sales announced by the United States Department of Agriculture (USDA) and significant purchases by China and Colombia. Additionally, the US 2024/25 corn production forecast has been reduced to 15.127 billion bushels, a reduction from the previous forecast of 15.207 billion bushels, due to a decrease in the predicted corn planting area by 1 million acres. Despite this, the projected yield has been raised to 182.9 bushels per acre, up from 182.3 bushels per acre, although the actual yield remains lower than initially anticipated despite the increase.

Brazil

In W36, wholesale maize prices in Brazil fell significantly by 10% WoW to USD 0.18/kg, down from USD 0.20/kg. This price drop comes as Brazil projects its 2024/25 corn crop to reach 133.57 mmt, a 6% increase from the previous season. This increase in production occurs despite a slight reduction in the total area dedicated to corn cultivation, which decreased to 20.87 million ha from 20.99 million ha in 2023. The rise in production is due to improved average productivity, expected to increase to 6.4 metric tons per ha from 5.98 mt/ha due to recovery from previous weather-related issues. The production boost is anticipated to be driven primarily by the second harvest, while the summer harvest is forecasted to decrease.

Argentina

The wholesale price of Argentine corn surged 18.75% WoW and 5.56% MoM to USD 0.19/kg. This price increase is primarily due to significant setbacks in Argentina's corn production caused by an outbreak of corn stunting disease. The disease has spread from northern regions to central Argentina and parts of the Pampas, impacting corn crops. This outbreak has led to delays in input sales and reduced planting expectations, potentially resulting in a production shortfall of around 18 mmt. As of August 15, 2024, the Rosario Stock Exchange projected Argentina's total corn production at 49 mmt, an 18 mmt reduction from earlier estimates due to the disease outbreak.

Ukraine

The wholesale price of Ukrainian maize remained unchanged WoW but increased 6.67% MoM and 23% year-on-year (YoY), reaching USD 0.16/kg. This price surge is due to a severe heat wave in Jul-24, which is expected to impact Ukraine's corn production significantly. The Ukrainian Grain Association (UGA) forecasts a 2024 corn harvest of 23.4 mmt, down from 29.6 mmt in 2023. This reduction, potentially as high as 30% YoY in affected regions, could drive prices up in the coming weeks. Despite these challenges, the Ukrainian government remains cautiously optimistic, with the acting finance minister projecting a more moderate 15% decline in late crop yields.

Romania

In W36, Romanian maize wholesale prices dropped by 5% WoW and 9.52% MoM and YoY, reaching USD 0.19/kg. This decline is attributed to lower production estimates for the new crop, as dry weather since early July 2024 has negatively impacted yields. Market participants predict a 10 to 15% reduction in production for the upcoming Oct-24 to Sept-25 season, leading to expectations of tighter supply conditions. Combined maize production estimates for Romania and Bulgaria have decreased by 4.5 mmt for this period.

3. Actionable Recommendations

Optimize Planting and Harvesting Practices to Minimize Risks

Brazil's slower progress in summer corn sowing and the potential climatic risks underscore the need for optimizing planting and harvesting practices. To address these challenges, Brazil should encourage timely and efficient sowing practices, including using precision agriculture technologies to optimize planting conditions and reduce delays. Producers should employ advanced weather forecasting tools to anticipate climatic risks and adjust planting and harvesting schedules accordingly. Additionally, implementing contingency plans to manage irregular humidity and temperature fluctuations will be crucial. Supporting early-season crop management practices like irrigation and pest control will help ensure healthy crop development during critical growth periods. By adopting these measures, Brazil can better navigate the challenges of summer corn sowing and safeguard its production.

Mitigate Disease Impact and Enhance Disease Management

Argentina’s corn production setback due to the Spiroplasma kunkelii outbreak necessitates an urgent focus on mitigating the disease's impact and enhancing disease management strategies. To address the spread of corn stunting disease, Argentina should implement comprehensive disease management plans, which involve early detection, regular monitoring, and control measures for affected areas. Collaboration with agricultural researchers is essential to explore effective treatments and develop resistant crop varieties. Additionally, promoting Integrated Pest Management (IPM) is crucial for controlling the leafhopper vector responsible for transmitting the disease. This includes monitoring pest populations, using biological control agents, and applying targeted insecticides. Furthermore, providing support and training programs to farmers will be vital, focusing on best practices for managing disease outbreaks, such as using disease-resistant seeds and effective crop rotation strategies.

Diversify Export Markets and Strengthen Trade Relations

Given the projected decline in Brazil’s corn exports and the reduction in Ukraine’s export potential, both countries should prioritize diversifying their export markets and strengthening trade relations. Brazil should explore new and emerging markets with growing demand for corn, expanding beyond traditional buyers to mitigate the impact of reduced export volumes. Simultaneously, Ukraine should focus on fortifying trade relations with key markets such as China, North Africa, and the Middle East to secure export opportunities. Both nations should also enhance their trade agreements, negotiating and solidifying deals to ensure stable export channels and cushion against market fluctuations. Additionally, investing in infrastructure and logistics will be crucial for streamlining export processes, reducing delays, and improving competitiveness in the global market. Efficient logistics will support timely delivery and strengthen both countries' positions in international trade.

Sources: Tridge, Portal Do Agronegócio, Agroportal, UkrAgroConsult, NoticiasAgricolas, Pig 333, Agrotimes, Foodmate