In W46, global butter markets showed mixed short-term gains but continued YoY pressure, reflecting structural oversupply and evolving market dynamics. Germany experienced modest price increases likely driven by seasonal demand, while Belgium, France, and the Netherlands faced ongoing declines due to cooperative strategy shifts, ample cream supplies, and production surpluses. In the US, butter prices rose slightly WoW but declined over the month and year, reflecting higher milk production, increased cow productivity, and weaker export demand. Market trends at the GDT confirmed continued pressure, as strong competition from US and European suppliers limited recovery. Across Europe, cautious buyer behavior, ample inventories, and weak international demand kept the market tone restrained. In the US and Oceania, increasing butterfat supplies and strong competition point to continued price softness. Strategies to navigate the volatile butter market include product differentiation through specialty or value-added lines and strengthening cooperative governance.

1. Weekly Price Overview

Short-Term Gains Mask Persistent YoY Pressure Across European and US Butter Markets

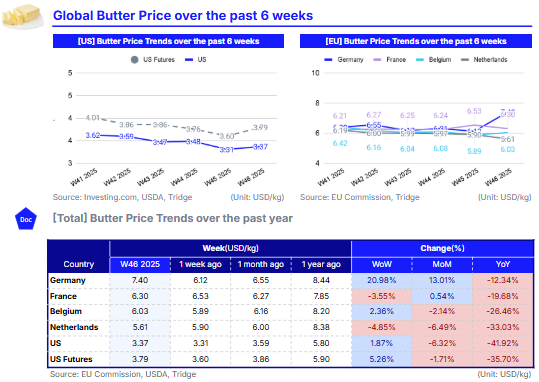

In W46, Germany’s butter prices averaged USD 7.40 per kilogram (kg), rising 20.98% week-on-week (WoW) and 13.01% month-on-month (MoM), but remaining 12.34% lower year-on-year (YoY). The WoW rise could be due to short-term seasonal demand and broader structural market factors. Belgium recorded a 2.36% WoW increase to USD 6.03/kg but continued to decline 2.14% MoM and 26.46% YoY, while French butter fell 3.55% WoW and 19.68% YoY to USD 6.30/kg, despite a modest 0.54% MoM rise. These mixed trends across Belgium and France were likely influenced by European-wide production surpluses, shifting cooperative strategies, and policy changes. Meanwhile, the Netherlands experienced consistent declines, with prices falling 4.85% WoW, 6.49% MoM, and 33.03% YoY to USD 5.61/kg. This reflects oversupply, structural market adjustments, and the growing disconnect between cooperative profits and farmer payments.

In the United States (US), butter prices averaged USD 3.37/kg, up 1.87% WoW but down 6.32% MoM and 41.92% YoY. Similarly, US butter futures stood at USD 3.79/kg, marking a 5.26% WoW increase but declining 1.71% MoM and 35.70% YoY. The pronounced MoM and YoY declines in the US reflect improved milk output, ample cream supplies, and weaker export demand, which have expanded domestic butter stocks and driven a correction from last year’s elevated levels. The modest WoW gains likely stem from short-term seasonal demand ahead of the holiday period.

2. Price Analysis

Cautious Buyers and Oversupply Keep Global Butter Market Under Pressure

At the fortnightly Global Dairy Trade (GDT) event on November 18, the average price for dairy commodities stood at USD 3,678 per metric ton (mt), reflecting a 3% decline from the previous auction. Butter recorded an average of USD 5,886/mt, down 7.6%, as rising global milk supply and particularly high butterfat output continue to weigh on prices. While export demand from Oceania remains steady, strong competition from the US and European suppliers has limited price recovery, keeping the market under pressure.

In the European Union (EU), ample cream availability and steady production are exerting further downward pressure on values. Buyers remain cautious, focusing on near-term needs rather than forward contracts, while export demand from the Middle East and Asia remains subdued. Domestic consumption shows little urgency, and inventories comfortably exceed immediate requirements, creating a cautious market tone ahead of contracting for early 2026.

In the US, the United States Department of Agriculture (USDA) indicates milk production reached 18.28 billion pounds (lb) in Sep-25, a 4.22% YoY increase. This growth stems from a rise in milk cow numbers, from 8.91 million heads in 2024 to 9.15 million heads in 2025, and a 1.52% YoY increase in per-cow productivity to 1,999 lb. As a result, the USDA expects US butter prices for 2025 to decline in the third and fourth quarters, driven by expanded milkfat supply and weaker market support.

3. Strategic Recommendations

Mitigate Risk and Capture Value in a Weakening Global Butter Market

In Europe, where Germany shows short-term seasonal gains but Belgium, France, and the Netherlands face consistent YoY declines due to structural oversupply and cooperative shifts, processors and farmers should consider targeted product differentiation and value-added production. This could include specialty butter, organic or grass-fed lines, and private-label partnerships that command premiums, helping offset pressure from commodity pricing. Strengthening cooperative governance and renegotiating supply agreements can also align producer incentives with processing profitability, reducing the disconnect between farmer payments and cooperative margins.

In the US, rising milk production and expanding butterfat availability are creating downward pressure on both spot and futures prices. Market participants should focus on inventory management and strategic timing of sales, leveraging short-term seasonal demand spikes to optimize margins while avoiding overexposure during periods of weak export interest. Expanding access to international markets where supply is tighter, such as Southeast Asia or the Middle East, through differentiated product offerings or flexible contract structures could help reduce reliance on saturated domestic demand.

For Oceania exporters, high butterfat output and strong competition from US and European suppliers suggest that price recovery is limited. Strategic recommendations include increasing operational efficiency to reduce production costs, exploring specialty and high-margin butter segments, and developing coordinated hedging strategies to protect against price volatility at GDT events.