In W4 in the maize landscape, some of the most relevant trends included:

- BAGE lowered Argentina's 2024/25 corn forecast by 1 mmt, projecting 49 mmt due to hot weather and insufficient rainfall. Despite challenges, planting is nearly complete, with 98.3% of the area planted.

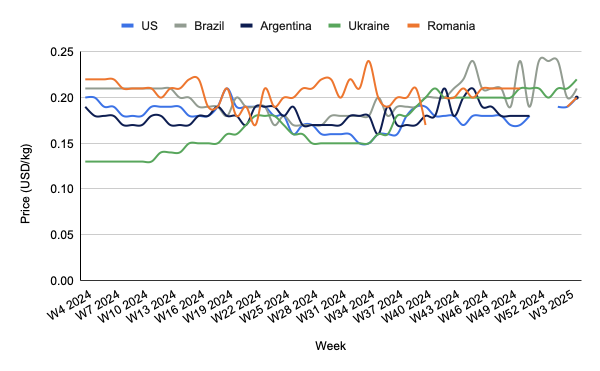

- Regarding pricing, corn prices in Brazil and the US rose WoW, driven by weather challenges. Meanwhile, Ukraine maize prices surged YoY to USD 0.22/kg due to severe drought and lower production forecasts.

- Bangladesh achieved a record corn production of 4.87 mmt in 2023/24, up 7% YoY. However, a shortfall remains, with the feed industry needing 6.5 mmt annually, pushing the country to import 1 to 2 mmt to bridge the gap.

1. Weekly News

Argentina

Argentina Reduced 2024/25 Corn Production Forecasts Due to Weather Challenges

The Buenos Aires Grain Exchange (BAGE) lowered Argentina's 2024/25 corn production forecasts by 1 million metric tons (mmt), citing hot weather and insufficient rainfall as key factors impacting yields. Corn is projected at 49 mmt, with dry conditions particularly affecting the southern farmlands and central-eastern Entre Rios province. Despite these challenges, planting progress has been strong, with 98.3% of the corn area planted.

Bangladesh

Bangladesh Corn Output Hits Record High but Demand Outpaces Supply

According to the Bangladesh Bureau of Statistics (BBS), Bangladesh has achieved a record corn production of 4.87 mmt in the 2023/24 marketing year (MY), reflecting a 7% year-on-year (YoY) increase. The agriculture ministry is targeting a production goal of 5.81 mmt for 2025 to meet growing demand, driven by its use in animal feed, especially for compound feed and silage. However, the Bangladesh Feed Producers Association (FIAB) highlights a shortfall as the industry requires 6.5 mmt annually, requiring 1 to 2 mmt imports to bridge the gap. Corn cultivation is gaining momentum among farmers, supporting the sector's growth.

Brazil

Stable Corn Estimates in Brazil Amid Weather Concerns and Ethanol Demand Growth

The 2024/25 Brazil corn estimate remains unchanged despite concerns about corn yields in Rio Grande do Sul and potential delays in Safrinha corn planting in Central Brazil due to persistent wet weather. Nationwide, the first corn crop was 1.3% harvested in W4, down from 5.1% in 2024. In Paraná, 94% of the first corn crop is rated as good, with most of the crop progressing well despite a drier pattern in western and southwestern areas since mid-Dec-24, which may affect later-developing yields. Pest and disease pressures have been minimal. The Safrinha crop has seen initial planting (less than 1%) from a total projected planting area of 16.59 million hectares (ha), up 1% YoY, supported by increased demand for corn-based ethanol.

Brazil Corn Exports Surge Beyond January Projections

According to the National Association of Cereal Exporters (ANEC), Brazil's corn exports are on track to surpass initial projections for Jan-25. Corn shipment estimates stood at 3.53 mmt, an increase from W3's forecast of 2.98 mmt. This highlights strong export momentum as Brazil continues to capitalize on robust global demand for its agricultural commodities.

Ukraine

Ukraine Grain Exports Climb 10% in 2024/25

As of January 22, Ukraine exported 24.47 mmt of the 2024/25 season's grains and pulses, representing a 10% YoY increase, according to the Ministry of Agrarian Policy and Food of Ukraine. However, corn exports totaled 11.60 mmt, showing a 3.4% YoY decline compared to the previous year. Despite the growth in overall grain exports, corn export performance has slightly weakened YoY.

2. Weekly Pricing

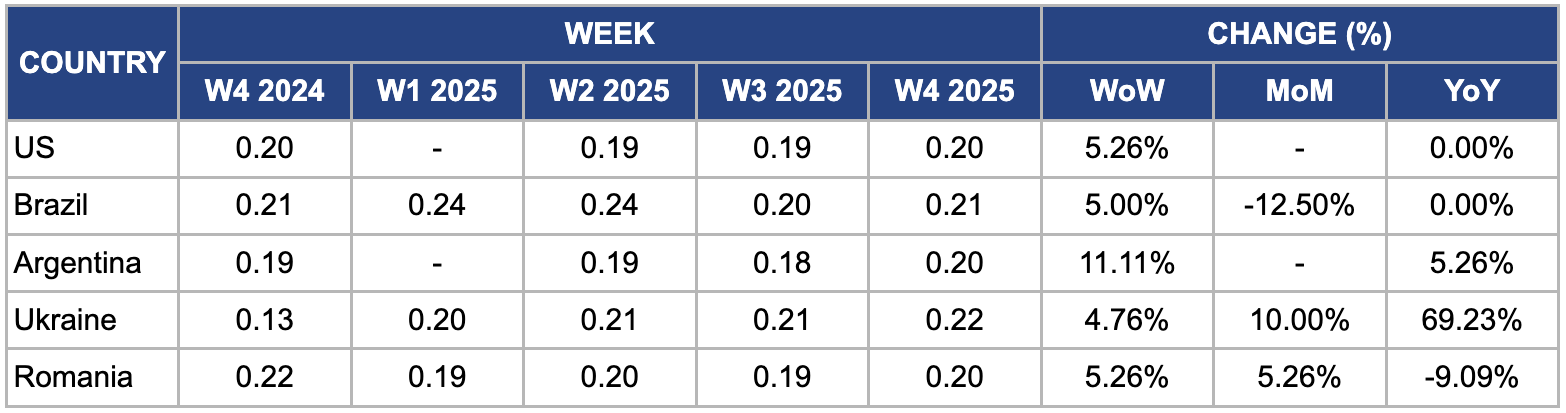

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W4 2024 to W4 2025)

US

In W4, wholesale maize prices in the United States (US) increased by 5.26% week-on-week (WoW), reaching USD 0.20 per kilogram (kg). This price rise comes amid a reduced global corn production forecast for 2024/25 by the International Grains Council (IGC). The forecast downgrade is primarily due to a reduction in the expected US corn crop, now estimated at 377.6 mmt, aligning with the revised figures from the United States Department of Agriculture (USDA).

Brazil

In W4, wholesale maize prices in Brazil increased by 5% WoW, reaching USD 0.21/kg. This price surge is due to the challenging conditions faced by corn producers in Mato Grosso, where heavy rains have delayed the harvest and exposed weaknesses in logistics and storage. The Mato Grosso Soybean and Corn Producers Association (APROSOJA MT) is closely monitoring the situation, as the weather disruptions have impacted operations.

Argentina

In W4, Argentinian maize prices increased by 11.11% WoW and 5.26% YoY, reaching USD 0.20/kg. This price increase is primarily due to adverse weather conditions, as hot temperatures and insufficient rainfall have affected the country's maize production. BAGE has revised its forecast for Argentina's 2024/25 corn crop, lowering it by 1 mmt to an expected yield of 49 mmt. The reduction is mainly due to high temperatures and dry conditions, particularly in the southern farmlands and central-eastern areas of Entre Rios province.

Ukraine

In W4, wholesale maize prices in Ukraine rose by 4.76% WoW, 10% month-on-month (MoM), and surged by 69.23% YoY, reaching USD 0.22/kg. This significant price increase is mainly due to a substantial reduction in maize production caused by severe drought conditions. According to USDA projections, Ukraine's corn output is expected to decline to 25 mmt in 2024/25 MY, a 23% decrease from the previous season and the lowest production level since 2017. The drought impacted crop yields, leading to a tighter domestic maize supply.

Romania

In W4, Romanian maize prices increased 5.26% WoW and MoM to USD 0.20/kg. This rise is primarily attributed to a significant reduction in maize production due to adverse weather conditions. Romania harvested only 4.88 mmt of maize from 1.8 million ha in 2024, marking the lowest since 2015. The United States Department of Agriculture (USDA) also projected Romania's maize output to drop to 7.8 mmt, the lowest level in 11 years. Moreover, many farmers have shifted from maize to more profitable crops like rapeseed, further decreasing maize cultivation areas. These factors have reduced maize supply, exerting upward pressure on prices.

3. Actionable Recommendations

Diversify Export Markets and Strengthen Trade Agreements

Significant corn producers like Bangladesh, Brazil, and Ukraine should diversify their export markets to reduce dependency on specific regions and minimize risks associated with fluctuating demand. For instance, Bangladesh should look into expanding its export capacity to neighboring countries in Southeast Asia or even the Middle East. With its strong export momentum, Brazil can continue to capitalize on opportunities in markets like China and the European Union (EU), where demand for animal feed and ethanol remains strong. Moreover, strategic trade agreements can help secure long-term commitments and market access, further boosting export volumes and stabilizing revenues for domestic producers.

Improve Supply Chain and Storage Infrastructure

The weather disruptions in Mato Grosso, Brazil, and Ukraine’s logistical challenges amid increased export volumes highlight the need for better storage and transportation infrastructure. In particular, improving grain storage capacity to avoid spoilage and investing in more efficient transportation networks would alleviate some logistical bottlenecks. This includes upgrading storage facilities, increasing transportation capacity, and reducing delays in loading ports. Brazil and Ukraine could benefit from modernizing their supply chains to reduce costs, enhance the shelf life of their products, and ensure a smoother transition from farm to export market.

Optimize Irrigation and Water Management

In light of the hot weather and insufficient rainfall affecting corn production in Argentina, Ukraine, and Brazil, producers in these regions must adopt advanced irrigation systems and water management techniques. These could include drip irrigation, rainwater harvesting, and soil moisture sensors to better manage water resources, especially in areas experiencing drought. Investment in such systems would mitigate the impact of unpredictable weather and enhance yield stability, reducing the risk of production shortfalls and the resulting price volatility. Moreover, governments and agricultural organizations could provide incentives for farmers to adopt these technologies to increase resilience in the long term.

Sources: Tridge, Hellenic Shipping News, NoticiasAgricolas, UkrAgroConsult