.jpg)

1. Weekly News

Brazil

Brazil's Sugarcane Sector Faces USD 440 Million Loss from Fires, 15% Drop in Productivity Projected

Forest fires across Brazil have severely impacted agribusiness, especially sugarcane production. The Organization of Associations of Sugarcane Producers of Brazil (ORPLANA) estimates losses could surpass USD 440.34 million (BRL 2.5 billion), with approximately 390 thousand hectares (ha) damaged in major states like São Paulo, Minas Gerais, and Goiás. Sugarcane productivity is forecasted to drop by around 15%, potentially affecting global sugar supply and ethanol prices. Efforts to combat and prevent fires were discussed in a webinar by the Brazilian Agribusiness Association (ABAG), featuring experts who detailed government and industry responses, including increased fire management training, a crisis cabinet, and significant investments in Conservation Units.

Egypt

Egypt Enforces Six-Month Sugar Export Ban to Stabilize Local Prices Amid Supply Challenges and Climate Impacts

The head of the Supply Committee for Egypt's General Importers Division endorsed the Ministry of Investment and Foreign Trade's recent six-month ban on sugar exports, as outlined in Ministerial Resolution No. 88 of 2023 and reiterated in Resolution No. 68 of 2024. This measure allows for the export only of surplus quantities, aiming to stabilize local prices following last year's spike when sugar prices reached USD 1.03 per kilogram (EGP 50/kg) due to supply shortages. Climate challenges in India and Thailand, the world's major sugar exporters, have constrained Egypt's sugar market. Despite producing 2.7 million metric tons (mmt) tons of sugar annually — covering only part of its 3.5 mmt demand — Egypt relies on 15 sugar factories, processing over 300 thousand acres of sugarcane and 650 thousand acres of sugar beets.

India

USDA Raises India’s 2024/25 Sugar Production Forecast by 4% Following Strong Monsoon Rainfall

The United States Department of Agriculture (USDA) has raised India’s 2024/25 sugar production forecast by 4% to 35.5 mmt of raw material basis, or 33.2 mmt after ethanol allocation. This increase is due to sufficient monsoon rainfall in major sugar-producing states, including Maharashtra, Karnataka, and Uttar Pradesh, which has improved soil moisture and groundwater for cane irrigation. The 2023/24 estimate remains steady at 34 mmt of raw material basis or 32 million tons after ethanol allocation.

Germany

Germany's 2024/25 Beet Sugar Production Forecast Raised 17% to 4.95 MMT

The German Sugar Association has raised its forecast for Germany's refined beet sugar production for the 2024/25 season to 4.95 mmt, up 17% from the previous season's 4.22 mmt. This increase follows an expanded beet planting area of 385 thousand hectares, an increase of 5.7% year-on-year (YoY), and favorable weather-boosting beet yields and sugar content. German farmers are forecasted to deliver 32.96 mmt of beets, with an estimated 85.5 mmt/ha yield and an average sugar content of 17.1%.

Netherlands

Early Netherlands Sugar Beet Campaign Yields High Sugar Content

In the first two weeks of the Netherlands sugar beet campaign, factories processed over 28 thousand metric tons (mt) daily. National sugar content in beets rose to 15.8%, with regional variations from under 15% in the Southeast Netherlands to 16.6% in Groningen. Beets harvested from lighter soils, particularly those with lower growth potential, were delivered in W41. The tare percentage dropped to 7.8% in W40, which was attributed to pre-rainy-season harvests. Leaf mold infections, driven by high early Sep-24 temperatures, have spread but slowed with recent cooler weather.

Vietnam

Vietnam's 2023/24 Sugar Production Rises 20% with Record Prices, Imports Expected to Decrease in 2024/25

The Vietnam Sugar Cane Producers Association reported that for the 2023/24 marketing year (MY), approximately 175 thousand hectares (ha) were harvested, yielding 6.79 mt of sugar/ha. In W41, farmers in Phú Yên Province are selling their cane at a record price of USD 52.02/mt (VND 1.3 million/mt). The International Sugar Organization (ISO) estimated Vietnam's sugar production for this season to be around 1 mmt, reflecting a 20% increase from the previous year. For the upcoming 2024/25 season, the ISO projects production could reach 1.1 mmt. To meet domestic consumption, Vietnam needs 2.3 mmt in 2024/25, and sugar imports are expected to be 1.4 mmt, a decrease of 6.5% from the previous year.

2. Weekly Pricing

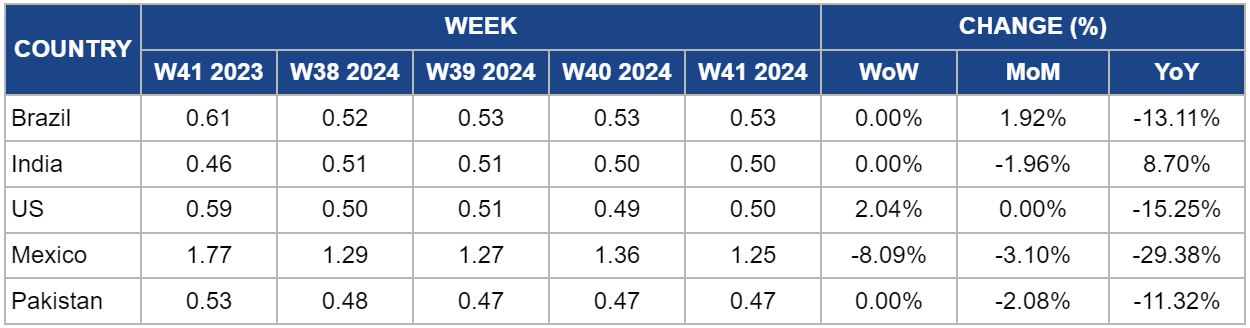

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W41 2023 to W41 2024)

.png)

Brazil

In W41, Brazil's refined sugar wholesale price remained steady at USD 0.53/kg for the third week, with a slight 1.92% month-on-month (MoM) increase from USD 0.52/kg in W38 and a decrease of 13.11% YoY from USD 0.61/kg. Brazil's recent sugar export surge, with a new record of 3.95 mmt shipped in Sep-24, suggests that international supply may temporarily stabilize, easing upward price pressures. This export increase was supported by dry weather in South-Central Brazil, which favored uninterrupted harvesting and sugar production and enhanced port efficiency due to fewer rain-related interruptions. However, global sugar prices have depreciated despite high export volumes, with declines in Mar-25 and May-25 raw sugar contracts on the Intercontinental Exchange Inc. (ICE), dropping to USD 0.2301 and USD 0.2127 per pound (lb), respectively. This dip could reflect a short-term oversupply sentiment and expectations of increased availability. While Brazil's record exports and favorable production conditions could temporarily temper global sugar prices, future pricing may depend on continued weather stability and Brazil's export consistency. Extended dry conditions could eventually reduce sugarcane yields, tighten supplies, and prompt higher prices, especially if other producers like India or Thailand face production issues. Thus, any adverse climate shifts in Brazil may impact future prices globally, reinforcing volatility in sugar markets.

India

India’s refined sugar prices remained stable at USD 0.50/kg in the second week of Oct-24, showing a modest MoM decrease of 1.96% from USD 0.51/kg. This stability comes amid an upward revision in India’s 2024/25 sugar production forecast by the USDA, which now estimates production at 35.5 mmt on a raw basis equivalent to 33.2 mmt after ethanol allocation, up 4% from previous forecasts. The revision is due to favorable monsoon rainfall, enhancing soil moisture and groundwater availability for irrigation, particularly in Maharashtra, Karnataka, and Uttar Pradesh. Increased production in India may contribute to sustained or declining prices if domestic supply remains strong and export restrictions persist.

United States

In W41, the wholesale price of refined sugar in the United States (US) increased to USD 0.50/kg, marking a 2.04% week-on-week (WoW) rise from USD 0.49/kg. Despite this recent price increase, sugar prices decreased by 29.38% YoY. Furthermore, USDA data shows that US sugar production is projected to reach a record high of 9.49 mmt for the 2024/25 season, driven by favorable yields from both beet and sugarcane crops. However, this projection does not yet factor in potential damage from hurricanes Helene and Milton, which could impact Florida's output as the state is the second-largest sugarcane producer after Louisiana. Any significant crop losses in Florida could tighten domestic supplies, potentially supporting or raising US sugar prices if disruptions reduce output below initial expectations.

Mexico

Mexico's refined sugar prices dropped to USD 1.25/kg in W41, marking a sharp weekly decline of 8.09% from USD 1.36/kg and a YoY decrease of 29.38% from USD 1.77/kg. These declines reflect the impact of the "Zafra" harvest season and stable yields in key sugar-producing regions such as Veracruz, San Luis Potosí, and Jalisco. Generating around USD 1.51 billion (MXN 30 billion) annually, the industry plays a crucial role in regional economies, with Veracruz alone contributing 50% of the country's production. The Mexican sugar industry is also adopting "Sugar 4.0" strategies to address long-term pressures, including volatile input costs, fluctuating exchange rates, and climate challenges. Automation, data-driven monitoring, and energy-efficient processes are expected to enhance productivity, optimize resource use, and stabilize production costs by upgrading outdated equipment with smart, connectable solutions. These efforts aim to make Mexico's sugar sector more resilient and adaptable, providing a future-ready foundation amid the complex global market.

Pakistan

Pakistan's refined sugar wholesale price remained stable at USD 0.47/kg in W41, marking a MoM decrease of 2.08% from USD 0.48/kg in W38. This stability follows the Sugar Advisory Board's (SAB) recent recommendation to allow an additional 0.5 mmt of sugar exports, pending Economic Coordination Committee (ECC) approval. This proposed export aligns with existing stock estimates and aims to balance local supply and export demand. Sugar stocks as of August 15 stood at 2.77 mmt, with recent data indicating consumption rates sufficient to leave a carryover surplus of around 0.704 mmt.

3. Actionable Recommendations

Strengthen Global Supplier Networks

To mitigate risks from Brazil’s reduced sugarcane yield, importers and refiners should diversify their sugar sources by establishing contracts with alternative suppliers, particularly from countries with growing production like India and Germany. Strengthening partnerships with these producers can stabilize supply, reduce dependency on Brazilian exports, and mitigate price volatility from climate disruptions.

Invest in Climate-Resilient Agriculture

Stakeholders in sugar-producing regions should prioritize investments in fire-resistant infrastructure, early warning systems, and sustainable farming practices. Collaboration with local governments and industry organizations to enhance fire prevention and management can reduce production losses, ensuring long-term productivity and supply stability in high-risk areas.

Sources: Akkerbouwbedrijf, Akhbarelyom, Ukragroconsult, Portal Do Agronegócio, Profit