W43 2025: Milk Powder

In W43, the global powdered milk market remained largely bearish, with both WMP and SMP prices declining across most regions due to abundant supply and subdued demand. The EU and Oceania recorded price drops for both products, reflecting strong milk output and cautious buying patterns. On the other hand, South America showed relative resilience, with WMP prices rising on steady demand and limited spot availability. At the GDT auction held on October 21, overall dairy prices declined, led by weaker WMP and SMP performance amid ample supply. Despite the soft market tone, export demand, particularly from North Asia and the Middle East, remained firm as buyers leveraged lower prices to secure volumes. Moving forward, EU and Oceania processors should adopt flexible pricing and diversify into value-added or fortified powders to sustain margins, while South American exporters can strengthen competitiveness through efficiency improvements and targeted market expansion.

1. Weekly Price Overview

Global Milk Powder Prices Weaken as Supply Outpaces Demand in Key Regions

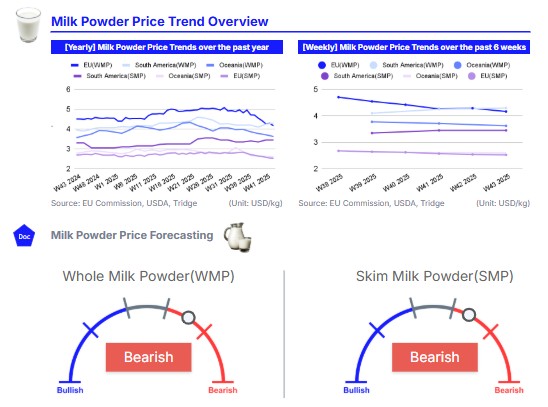

In W43, European Union (EU) whole milk powder (WMP) prices averaged USD 4.17 per kilogram (kg), marking a 2.28% week-on-week (WoW) decline, largely due to subdued demand as buyers limited purchases to short-term needs. Oceania also recorded a decline, with WMP prices down 2.36% WoW to USD 3.63/kg, reflecting increased milk output and record-high milk component levels that have led to abundant supply. In contrast, the South American market was bullish, with WMP prices rising 1.18% WoW to USD 4.30/kg, driven by steady demand and reduced spot availability as manufacturers focus on fulfilling contractual sales.

For skimmed milk powder (SMP), the EU market saw prices fall 1.79% WoW to USD 2.52/kg, as demand remained soft and buyers continued to exercise caution. In Oceania, SMP prices slipped 0.48% WoW to USD 2.60/kg, pressured by increasing milk output during the spring flush, which maintained high production levels. Meanwhile, South America’s SMP prices held steady WoW at USD 3.45/kg, supported by seasonally stronger milk production ensuring adequate supply, while production schedules ranged from steady to light depending on local market conditions.

2. Price Analysis

Powdered Milk Export Demand Remains Strong Despite Global Dairy Price Declines

At the fortnightly Global Dairy Trade (GDT) event held on October 21, the overall dairy price index declined by 1.4%, with the average winning bid price reaching USD 3,881 per metric ton (mt). Among the traded commodities, WMP prices fell by 2.4% to USD 3,610/mt, while SMP prices dropped by 1.6% to USD 2,559/mt. The decline in prices is largely attributed to ample global supply of milk powders.

Despite weaker prices, export demand, particularly for Oceania commodities, remained firm, supported by buyers taking advantage of lower price levels. During the GDT auction, North Asia emerged as the largest buyer of WMP, accounting for 58% of total volumes traded, followed by the Middle East at 20%. For SMP, demand was also steady, though prices declined as New Zealand SMP traded at a premium compared to European-origin SMP, making the EU more competitive. The majority of SMP sold at the event was destined for North Asia, followed by Southeast Asia/Oceania and the Middle East.

In the EU, WMP demand remains subdued as buyers continue to purchase only for immediate needs. Export interest is limited, prompting sellers to adjust offers to maintain competitiveness. SMP export demand is muted, and inventories are sufficient to meet current contractual obligations. In South America, demand for WMP remains steady, although contractual sales have constrained spot load availability from some producers. Meanwhile, SMP has consistent demand from both spot and contractual buyers.

3. Strategic Recommendations

Leverage Value-Added Opportunities to Stabilize the Milk Powder Sector

Given the current bearish conditions in the global powdered milk market, EU processors should adopt flexible pricing and contract strategies to stimulate export sales, especially in price-sensitive markets such as Southeast Asia, the Middle East, and Africa. Additionally, EU processors should explore value-added powder applications, such as fortified milk powders or blends tailored for infant formula, bakery, or confectionery use, to capture niche demand segments and improve margins.

In Oceania, manufacturers should mitigate downward price pressure by diverting surplus milk into high-margin categories, including specialized powders such as instant or enriched WMP and SMP or long-shelf-life dairy ingredients. Promotional pricing or longer-term supply contracts could also help stabilize offtake amid rising production.

For South American processors, the focus should be on maximizing export potential by capitalizing on limited global spot availability. Strengthening logistical efficiency and quality assurance systems can further enhance reliability and competitiveness in key import markets.