W44 2025: Wheat

.jpg)

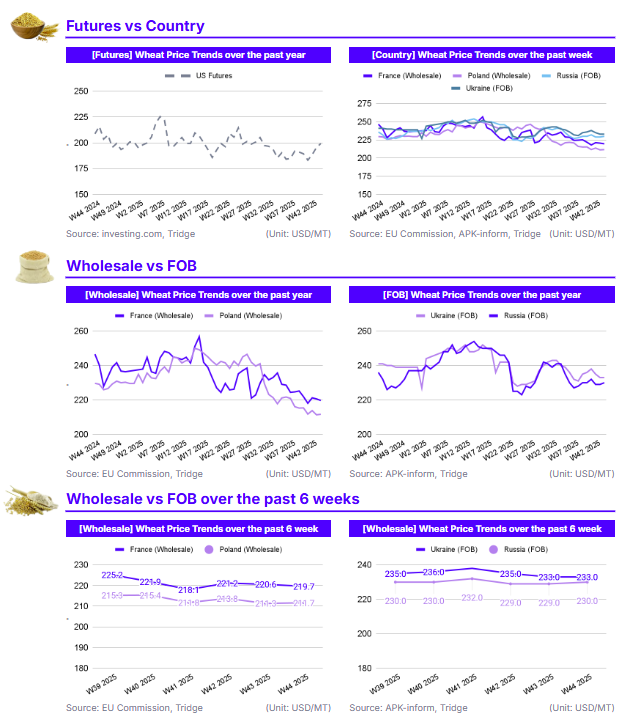

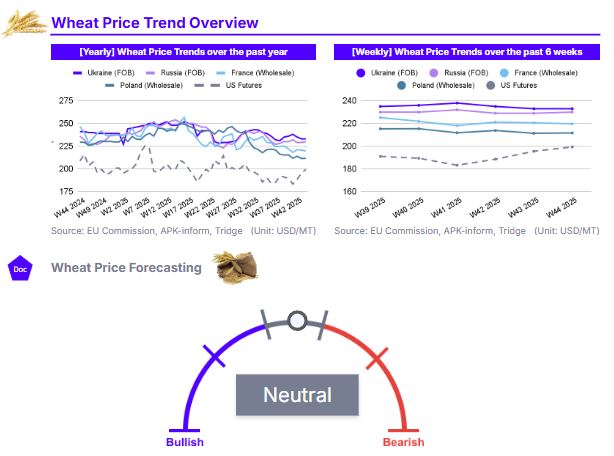

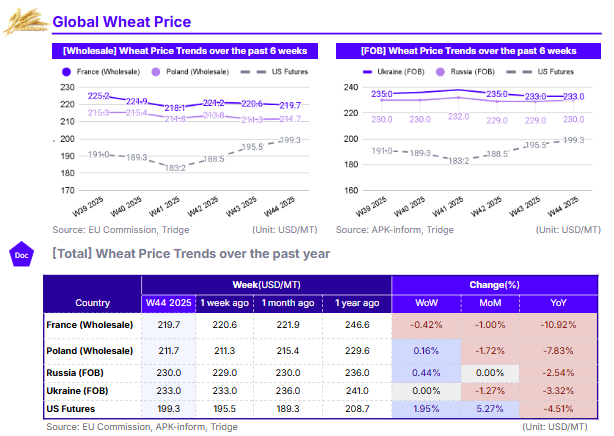

In W44 2025, US wheat prices rose WoW, while EU and Black Sea markets were stable. US Futures (USD 199.3/mt) increased 1.95% WoW, supported by strong exports. In contrast, French wholesale (USD 219.7/mt) dipped 0.42% WoW. Black Sea FOB prices were firm, with Russian FOB at USD 230.0/mt. The long-term outlook remains bearish, with most prices down YoY, including France (-10.92% YoY) and Poland (-7.83% YoY). This is driven by a global glut; the IGC raised its global production forecast to a record 827 mmt, pushing 2025/26 ending stocks to 275 mmt. The US was the outlier, rising 5.27% MoM. For EU buyers, Poland (USD 211.7/mt) offers the best price, but France (USD 219.7/mt) is recommended for high-volume procurement due to its strong 2025 harvest.

1. Weekly Price Overview

US Wheat Futures Lead Weekly Gains Amidst Broadly Stable Market

In W44 of 2025, US wheat prices showed weekly gains while other major markets saw minimal movement. In the United States (US), US Wheat Futures closed at USD 199.3 per metric ton (mt), a notable 1.95% increase week-on-week (WoW). This upward momentum is likely driven by strong annual export demand and market optimism surrounding potential new trade agreements with China, which offset news of a slowdown in weekly export inspections towards the end of Oct-25. In contrast, European prices were mixed but mostly flat. France saw its wholesale price decline slightly to USD 219.7/mt, down 0.42% WoW, as planting for the 2026 season progresses well and ahead of last year's pace. Poland's wholesale price saw a minor 0.16% WoW rise to USD 211.7/mt, supported by its ban on Ukrainian grain imports. Lastly, Black Sea prices also held firm. Russia's Free on Board (FOB) price increased 0.44% WoW to USD 230.0/mt, while Ukraine's FOB price was unchanged at USD 233.0/mt. Ukraine’s prices are supported by a decreased production volume in 2025 while Russia’s prices are supported by high export demand.

2. Price Analysis

Bearish YoY Trend Continues as Global Production Forecasts Pressure Markets

The long-term price outlook remains bearish as of W44 of 2025, with nearly all markets showing significant declines year-on-year (YoY) due to a high global supply outlook. The International Grains Council (IGC) has again raised its forecast for global grains production, weighing on prices. In its most recent monthly report, the IGC raised its global wheat production forecast by 8 million metric tons (mmt) to 827 mmt, a record high and up 1.1% from the prior season. The revised outlook is largely driven by upgraded production outlooks for Russia, the US and Argentina. Global wheat consumption is expected to be 7 mmt lower than production, leading to a build up of stocks to a three year high of 275mm at the end of the 2025/26 season.

This oversupply situation is most evident in France, where the wholesale price (USD 219.7/mt) is down 10.92% YoY, reflecting a 1.00% decline month-on-month (MoM). This significant YoY drop in France is linked to a strong domestic production recovery in 2025. Similarly, Poland’s price (USD 211.7/mt) is down 1.72% MoM and 7.83% YoY. Black Sea prices followed a similar, though less severe, long-term trend. Russia’s Free on Board (FOB) price (USD 230.0/mt) was stable MoM but down 2.54% YoY, while Ukraine's price (USD 233.0/mt) fell 1.27% MoM and 3.32% YoY. The US market was the only outlier, with Futures (USD 199.3/mt) rising 5.27% MoM, though still down 4.51% YoY. This monthly strength is supported by a high-quality domestic crop and strong cumulative export demand in 2025.

3. Strategic Recommendations

Secure Price-Competitive Polish Wheat, but Leverage French Volume for Large-Scale Needs

In a global market characterized by oversupply and bearish long-term price trends, European buyers are well-positioned to optimize procurement costs. As of W44, Poland offers the most price-competitive origin within the EU among major wheat producing countries. Polish wholesale wheat is priced at USD 211.7/mt, a clear discount compared to French wholesale at USD 219.7/mt. For price-sensitive buyers, this USD 8/mt spread makes Poland the immediate choice for cost-effective sourcing. This price is supported by domestic fundamentals, including Poland's ongoing ban on Ukrainian grain, which insulates its market.

However, for larger buyers seeking to secure significant, consistent volumes, France presents a strong strategic alternative. The French market is currently defined by its strong domestic production recovery in 2025, which is the primary driver of its 10.92% YoY price decline. This ample harvest translates to high liquidity and greater availability of free volumes. Therefore, buyers prioritizing the fulfillment of large-scale contracts may find the French market better equipped to handle such orders, despite the slightly higher headline price. According to Tridge Eye transaction data, are exporters of grain from France in recent months.