.jpg)

1. Weekly News

Europe

North-Western Europe Potato Harvest Progress

The potato harvest in Northwestern Europe's key producing countries is almost complete, with notable advancements in W45. The Netherlands harvested 97% of its French fry potato crops, surpassing the 84% achieved during the 2023 season during the same time. Germany reached 99%, up from 92% the previous week. France made the fastest progress, harvesting 97% of its record 177 thousand hectares (ha) of potato area, a significant jump from 85% in W44. Belgium and the United Kingdom (UK) followed closely, each completing 95% of their harvests, up from 87% the week before.

Brazil

Brazil's Potato Industry Poised for Record Highs in 2024

According to the Center for Advanced Studies in Applied Economics (CEPEA), Brazil's potato farming sector has performed strongly in recent years, with optimistic projections for 2024. Despite rising production costs and regional difficulties, 2024 is poised to be a standout year for the industry, with prices reaching record highs since CEPEA's monitoring began in 2001. A significant factor supporting these high prices is the increased focus on potato production for the pre-fried industry, which has constrained supply for the fresh market. Producers with more capital have prioritized investments in the industrial sector over the table market. Looking ahead, 2025 also shows promise with sustained industrial investments, but concerns over seed availability could limit production and productivity.

Egypt

Egypt Imported 6,882 MT of Potato Seeds for 2024/25 Season

According to the Ministry of Agriculture, Egypt imported 6,882 metric tons (mt) of potato seeds for the 2024/25 season as of November 9, 2024. The seeds were sourced from various countries, including 2,600 mt from the Netherlands, 1,971 mt from France, 1,701 mt from Denmark, 250 mt from Germany, 225 mt from Scotland, and 135 mt from Poland. The Head of the Central Administration for Agricultural Quarantine emphasized publishing regular reports to ensure transparency and support market stability. These updates aim to help farmers and importers make informed decisions about planting schedules and land preparation while maintaining a balance in the potato seed market.

Spain

Spain's Potato Production Declined by 1.4% in 2024

Spain's Ministry of Agriculture has reported a potato production of 1.95 million metric tons (mmt) for the 2024 season, marking a 1.4% year-on-year (YoY) decrease. The harvest area has been the second lowest on record at 60,799 ha. However, despite the decline in total production, the average yield increased slightly by 0.55 mt/ha to 32 mt/ha, the third-best yield since 2017. The late potato harvest saw a minor increase of 1.2%, while the mid-season crop yield dropped by 4.4%. On the other hand, early harvest yields rose by 8.8%. The ongoing potato crisis in Galicia has been exacerbated by heavy rains, leading to significant losses, with many potatoes stored in warehouses rotting due to excess humidity.

Ukraine

Potato Prices Surged in Lviv's Wholesale Market Due to Weather and Production Challenges

In W46, the average price of potatoes at the Shuvar wholesale market in Lviv has surged to USD 0.59 per kilogram (kg), a 170% YoY increase from USD 0.22/kg during the same period in 2023. This sharp rise is due to several factors, including crop failures caused by abnormal heat and drought in the summer of 2024, reduced cultivation areas due to economic and logistical challenges, and rising production costs driven by higher prices for fuel, fertilizers, and other inputs. These challenges have collectively tripled potato prices in Ukraine this year.

2. Weekly Pricing

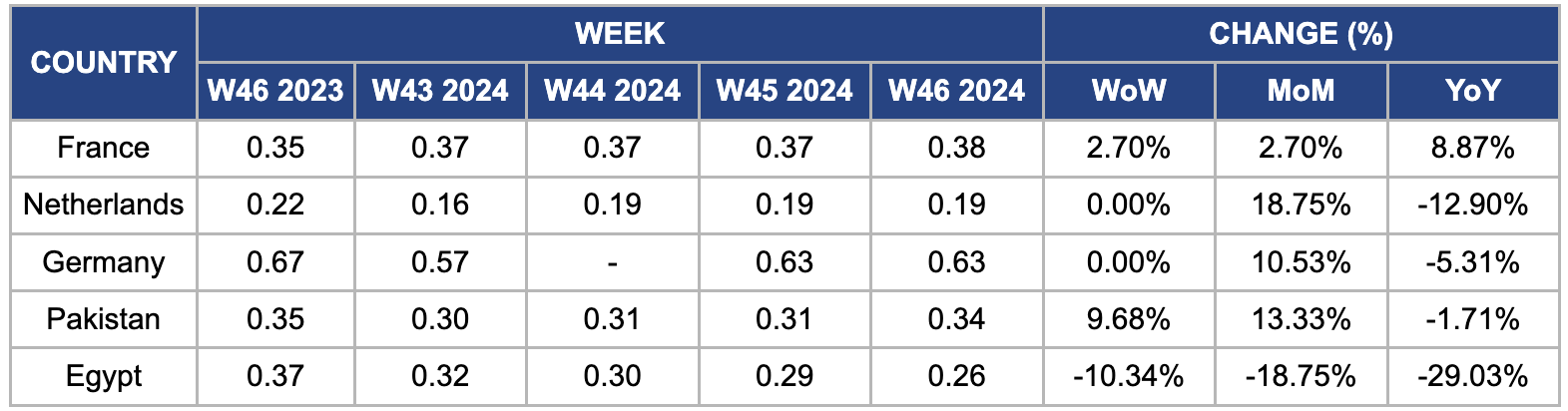

Weekly Potato Pricing Important Exporters (USD/kg)

Yearly Change in Potato Pricing Important Exporters (W46 2023 to W46 2024)

France

In W46, wholesale potato prices in France rose 2.70% week-on-week (WoW), reaching USD 0.38/kg, up from USD 0.37/kg in W45. This increase reflects a 2.70% rise month-on-month (MoM) and an 8.87% YoY jump. The price surge is due to several factors, including rising production costs, declining potato yields, and challenges like climate change, wireworms, and chemical bans. These factors led to the loss of 11 thousand ha of potato cultivation in the latest season. Moreover, heavy rainfall during the harvest season has downgraded yields and caused large quantities of potatoes to be discarded. France's potato supply has also been constrained by the completion of 97% of the harvest from a record 177 thousand ha, further tightening the market.

Netherlands

In W46, wholesale potato prices in the Netherlands remained stable WoW at USD 0.19/kg but experienced a notable 18.75% MoM increase from USD 0.16/kg in W43. This price surge is primarily due to limited supply, as planting has progressed rapidly and is almost complete, with only 10 to 20% of the area still pending. Favorable weather, featuring a mix of sunshine and showers, has supported potato growth, although some regions face challenges from heavy soil and lingering wet conditions. The 2024 growing season has been particularly challenging for farmers, including a seed shortage that resulted in higher prices and reliance on cut seed. Furthermore, persistent heavy rain extended the planting window beyond the usual 10-week period, severely affecting production in the southern Netherlands.

Germany

In W46, wholesale potato prices in Germany remained steady WoW at USD 0.63/kg but saw a significant 10.53% MoM increase. Rising production costs and declining output across key potato-growing regions in Germany, drive this price hike. Climate change, wireworm infestations, and chemical bans have compounded production challenges, with heavy rainfall further reducing yields and causing crop degradation. The processed food sector, which accounts for over 60% of Germany's potato consumption, has intensified competition for available supply. Despite the price rise, YoY prices have decreased by 5.31%, mainly due to a 9% increase in potato planting areas, which is expected to lead to a larger harvest and potentially lower prices in the coming months. However, challenges remain, especially with late-season diseases caused by adverse weather conditions. Moreover, potato consumption in Germany has fallen by 28% since 1990, as consumers increasingly prefer rice and pasta.

Pakistan

In W46, wholesale potato prices in Pakistan surged 9.68% WoW and rose 13.33% MoM to USD 0.34/kg. The price increase is due to several factors, including a 25% reduction in seed availability due to currency depreciation, which has escalated production costs. Additionally, rising export demand from regional markets such as Afghanistan and the Middle East has put further pressure on domestic prices. Logistical challenges have compounded localized supply shortages, driving the upward price trend. These issues reflect the harsh environment that potato producers in Pakistan face.

Egypt

In W46, Egypt's wholesale potato prices dropped to USD 0.26/kg, reflecting a 10.34% decrease WoW from USD 0.29/kg in W45. This decline is due to increased supply as the winter season begins and new crops come into production. The market is experiencing a surge in vegetable production, including potatoes, which is expected to further drive down prices as more winter crops become available. This drop follows sharp price increases in Aug-24 and Sep-24. Moreover, YoY prices have fallen by 29.03%, exacerbated by climate change impacts, a prolonged shortage of US dollars affecting potato seed imports, and broader economic challenges such as high inflation and currency depreciation. These factors have contributed to reduced yields, which dropped from 14 to 16 mt per acre in 2023 to 9 to 12 mt per acre in 2024.

3. Actionable Recommendations

Diversify Potato Seed Sourcing to Enhance Crop Resilience

Given the challenges related to seed availability and quality, Egypt and Spain should explore diversified sourcing strategies for potato seeds. This would reduce dependence on a single supplier and ensure consistent seed quality for future harvests. For instance, Egypt, which has experienced difficulties due to currency depreciation and limited imports, could form strategic partnerships with seed producers in countries with stable supply chains like the Netherlands, France, and Denmark. In Spain, where yields have dropped, and challenges in Galicia persist, diversifying seed sources can reduce the risk of crop failures caused by regional factors, such as soil quality or disease. This approach will help stabilize production levels and reduce the risk of future supply shortages.

Invest in Climate-Resilient Agricultural Practices

As climate change continues to impact potato yields, European countries should prioritize investments in climate-resilient agricultural practices. In Germany, the Netherlands, and France, where climate-related challenges such as wireworm infestations and heavy rainfall reduce yields, farmers can adopt more resistant potato varieties or improve water management techniques (e.g., irrigation systems to mitigate droughts or excessive moisture). In addition, integrated pest management (IPM) strategies should be encouraged to reduce the impact of pests and diseases, thereby stabilizing yields and production costs in the long term.

Invest in Improved Storage Solutions

Ukraine, Brazil, and Egypt can stabilize potato prices by investing in better storage infrastructure. Enhancing cold storage and warehouse capacities would help manage surplus potatoes during peak harvests and maintain supply during off-seasons. In Ukraine, storing potatoes for months could reduce price fluctuations, especially in winter when prices tend to spike due to scarcity. Similarly, Brazil and Egypt can stockpile potatoes during abundant harvests and release them when demand rises, avoiding market volatility. Modern storage solutions would also reduce spoilage, extend shelf life, and improve overall inventory management, leading to more consistent pricing and a more reliable supply chain.

Sources: Agro Times, Almal News, Nieuwe Oogst, Portal Do Agronegócio, Campocyl