W47 2025: Cheese

In W47, global cheddar markets showed mixed dynamics as EU and Oceania prices declined due to rising milk production and cautious buying, signaling potential downward pressure into early 2026. Meanwhile, US cheddar futures edged higher on seasonal demand expectations despite softer spot prices. The November 18 GDT auction also reflected weaker prices for key commodities, including cheddar and mozzarella, as increased milk output supported stronger cheese production in New Zealand and the US, where domestic milk volumes and exports remain robust. To navigate these conditions, EU and Oceania processors are advised to moderate bulk production or pivot to specialty and higher-value cheeses while utilizing storage strategies. On the other hand, US producers should hedge Q1-2026 prices, optimize production for holiday demand, and prioritize exports to high-demand regions. Across all regions, on-farm operations should focus on cost efficiency, feed optimization, and herd management to maintain profitability amid margin pressures.

1. Weekly Price Overview

Cheddar Markets Diverge as EU and Oceania Decline While US Futures Firm

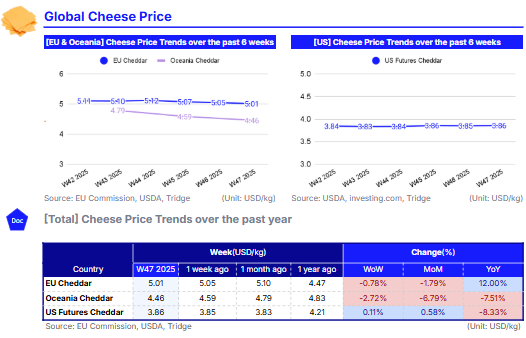

In W47, European Union (EU) cheddar averaged USD 5.01 per kilogram (kg), marking a 0.78% week-on-week (WoW) decline and a 1.79% month-on-month (MoM) drop, though still standing 12% higher year-on-year (YoY). The recent softening reflects growing supply driven by increased milk output, coupled with more cautious buying activity from both retail and food-service channels. This imbalance suggests that downward pressure on EU cheddar prices may persist into early 2026.

A similar trend is evident in Oceania, where cheddar prices fell to USD 4.46/kg, down 2.72% WoW, 6.79% MoM, and 7.51% YoY. The region’s spring flush has boosted milk availability, enabling strong cheese production. As a result, domestic prices have held steady while export prices have weakened, underscoring a market where supply continues to outpace demand.

In contrast, United States (US) cheddar futures edged up 0.11% WoW to USD 3.86/kg, a 0.58% increase MoM and 8.33% higher YoY. This relative firmness likely reflects seasonal expectations of stronger end-year cheese usage, including holiday-related consumption, and potential inventory drawdowns by processors ahead of year-end accounting. However, spot prices moved lower, with Chicago Mercantile Exchange (CME) block cheddar averaging USD 1.558/40-pound (lbs), down from USD 1.588/40-lbs the previous week, while barrels slipped to USD 1.605 from USD 1.661 in W46. With US milk production remaining elevated and processors needing to utilize recently added capacity, cheese output is expected to stay strong in the coming months, keeping the market under pressure despite firmer futures.

2. Price Analysis

Global Dairy Trade Sees Price Softening as Milk Production Rises

According to the fortnightly event, Global Dairy Trade (GDT), the November 18 auction recorded a softer outcome, with the average winning price falling 3% from the previous event to USD 3,678 per metric tons (mt). Most major commodities declined, including cheddar, which dropped 2.7% to USD 4,328/mt, and mozzarella, which fell 2.8% to USD 3,214/mt. North Asia purchased the largest volume of cheese, followed by Southeast Asia/Oceania and the Middle East. The overall downturn in prices reflects rising global milk production, which is boosting cheese output.

In New Zealand, milk production continued to expand. Output in Oct-25 reached 3.31 million metric tons (mmt), up 1.7% YoY, while milk solids production grew 2.8% YoY to 268.7 thousand mt. This growth is supported by increased use of feed inputs, especially palm kernel extract, whose imports have risen sharply this year. Pasture conditions remain favorable in the South Island, although the North Island is experiencing weak pasture growth.

In the US, milk production rose to an estimated 19.47 billion lbs in Oct-25, a 3.7% YoY increase driven by both herd expansion and higher yields per cow. Cheese exports strengthened as well, reaching 119.3 million lbs in Aug-25, up 28.1% YoY. Domestic demand is firm heading into the holiday season, with tighter barrel supplies, sufficient milk volumes, and improved retail buying. Spot opportunities tightened during the Thanksgiving week, yet both domestic and export demand continue to support key cheese varieties.

3. Strategic Recommendations

Manage Oversupply and Price Volatility in EU, Oceania, and US Cheese Markets

In the EU and Oceania, where milk production is high and cheddar prices are declining, processors should temporarily reduce bulk cheese production or shift output toward specialty cheeses, snack cheeses, or higher-value processed products to capture better margins. Implementing short-term storage strategies or using contract warehousing can help smooth inventory until demand recovers.

Facing firm futures but weaker spot prices, US producers should lock in Q1-2026 prices through futures or options contracts to hedge downside risk, while timing block and barrel production to meet holiday retail and food-service demand efficiently. Exporters should prioritize shipments to high-demand regions such as North Asia first, then Southeast Asia and the Middle East. They should also adjust volumes to avoid saturating markets where EU and Oceania supply is dominant. On-farm operations should focus on cost control and efficiency, including feed optimization, herd management, and minimizing energy and processing costs, to maintain profitability despite margin pressures.