In W17 in the avocado landscape, some of the most relevant trends included:

- Producers and exporters in Colombia, Guatemala, and Kenya are actively expanding avocado exports by investing in infrastructure, such as new packing facilities, forming strategic partnerships, and targeting new markets like the US and Argentina, while ensuring compliance with international quality and phytosanitary standards.

- Local growers and industry associations in Spain, Colombia, and Kenya are facing mounting challenges from external competition and logistical disruptions, including shipping delays caused by the Red Sea crisis, the US market’s high-quality requirements, and surging Moroccan imports. These pressures are forcing them to adapt marketing strategies, delay shipments, or call for consumer and government support.

- Regional authorities and producer organizations in the Canary Islands and Spain are promoting differentiation through certification and branding initiatives, such as the EU PGI status for Canary Islands avocados and the Aguacates CV quality seal in Valencia. These efforts aim to protect local production, enhance market appeal, and increase traceability and sustainability recognition.

- Growers in California and exporters in Mexico are responding to high global demand and limited US local supply by ramping up production. California is projecting its third-largest crop in a decade, and Mexican suppliers are maintaining export dominance, even as newer suppliers like Kenya and Guatemala seek to increase their share in the competitive global market.

1. Weekly News

Canary Island

Canary Islands Avocado Earns PGI Recognition for Unique Quality

The Canary Islands Avocado has been granted Protected Geographical Indication (PGI) status, becoming the first avocado in the world to receive this prestigious European designation. The PGI designation was officially published in the European Union (EU) Official Journal on April 22, 2025. The PGI seal guarantees that avocados grown in the Canary Islands meet rigorous quality standards and are closely linked to the region’s unique geographical and climatic conditions. The seal applies to Hass, Fuerte, and Pinkerton varieties and includes strict cultivation, harvesting, and packaging guidelines. This achievement marks a decade of growth for the avocado industry in the archipelago, where the cultivated area has reached 14.6 thousand tons in 2023. The PGI status is expected to support local farmers, improve production, and boost foreign trade by protecting producers from unfair competition. It also enhances the product's distinction in international markets, particularly its creamy texture and nutty flavor.

Colombia

Colombian Hass Avocados Gaining Ground in the US Market

Colombia’s avocado industry is growing, with the United States (US) emerging as an increasingly important market for Colombian Hass avocados. Green West, a vertically integrated avocado grower, packer, and exporter, saw its production grow by nearly 30% in 2024. That year, 30% of its exports were directed to the US, a notable increase reflecting the company’s strategic shift toward expanding its presence in this high-demand market year-round. However, Green West faces challenges in meeting the US market’s strict phytosanitary standards and ensuring consistent fruit quality, particularly in terms of oil content and flavor.

While Europe remains the primary market for Green West’s exports, the US offers significant opportunities due to its structured promotion efforts and high consumption rates. Yet, Colombian avocados must compete with Mexican avocados, which are better suited to the US market’s preference for higher oil content. To remain competitive, Colombian producers must ensure their avocados meet the specific quality standards required by US consumers, particularly regarding dry matter content, flavor, and ripening.

Guatemala

Guatemala Expands Avocado Exports with New Packing Plant

Guatemala is making significant progress in expanding its avocado exports with the opening of the Avo Pack packing plant in Santa Rosa. The government is actively pursuing new markets for Guatemalan avocados, targeting countries like Argentina and the US, alongside its existing export destinations, such as the Netherlands, the United Kingdom (UK), Spain, and Canada. The avocado industry, which supports over 6 thousand workers, is now the third fastest-growing crop in the country. The new packing plant will process millions of avocados, further boosting economic growth and reinforcing Guatemala's position in the global avocado market. With backing from the US government and private investors, Guatemala is solidifying its role as a strategic player in the avocado export industry, while the government continues to support producers, ensure access to international markets, and uphold high-quality standards.

Kenya

Kenya's Avocado Exports Struggle Due to Logistics Challenges

Kenya is entering its summer avocado export season, supplying the European market as Mediterranean producers like Spain and Morocco wind down. While demand and prices for Kenyan avocados have risen, exporters face significant logistical challenges due to the Red Sea crisis, which has extended shipping times to over 32 days and hindered competitiveness. Although air freight offers a faster alternative, its high costs and sustainability requirements from European retailers limit its viability. These challenges have led to a drop in export volumes and prompted some exporters to pause shipments.

However, this situation has also driven rapid growth in Kenya’s avocado processing industry, with nearly 30 oil extraction facilities now operating. Despite increasing competition from Peru, South Africa, and ongoing Mediterranean supplies, Kenya remains well-positioned early in the season. This is due to its high-quality fruit, favorable size distribution, and strong traceability.

Mexico

Mexico Dominates Global Avocado Production

Mexico remains the world’s leading avocado producer, with production for 2025 projected at 2.973 million tons. Strong global demand for its flavor and quality keeps it well ahead of competitors like Colombia and Peru. In addition to fresh exports, Mexico supplies a wide range of processed avocado products such as guacamole, frozen paste, and oils used in the cosmetics industry. Key producing states like Michoacán, Jalisco, and the State of Mexico rely heavily on avocado cultivation, which supports the livelihoods of thousands of families. While countries like Indonesia, Kenya, and Chile are expanding their avocado production, none currently rival Mexico’s dominant position in the global market.

Spain

Spain’s Avocado Industry Optimistic for 2025/26 as it Recovers from Drought

Spain’s avocado industry is gradually recovering after enduring up to five years of drought, especially in major producing regions such as Andalusia and the Valencian Community, which account for over 24 thousand hectares (ha) of cultivation and an annual yield of around 80 thousand tons. Recent rainfall has boosted reservoir levels, La Viñuela now stands at 50% capacity, bringing cautious optimism for the 2025/26 campaign. Still, producers emphasize that a full recovery may take another two to three years and highlight the need for long-term solutions, including infrastructure improvements like the proposed Axarquía desalination plant, to mitigate future water risks. Despite ongoing challenges, Spain remains the EU’s leading avocado supplier, contributing 10% to the market and exporting USD 506.5 million (EUR 445 million) worth in 2023, while areas like Valencia continue to grow production due to favorable coastal conditions and increasing investment.

Valencian Avocado Industry Faces Pressure from Rising Moroccan Imports

Spain’s avocado industry, particularly in the Valencian Community, is facing growing pressure as a sharp rise in Moroccan imports disrupts local markets during peak harvest season. The region, which cultivates 3.9 thousand ha of avocados, including 668 ha in Alicante, primarily grows the Lamb Hass variety, whose farmgate prices dropped by 29% in Mar-24, falling from USD 2.78 to 1.97/kg (EUR 2.44 to 1.73/kg). This decline is due to an 89% surge in Moroccan avocado imports in early 2025, with over 14 thousand tons entering in Jan-25 alone and overlapping with the local harvest.

Although avocado cultivation is expanding rapidly in Spain and generated more than USD 25.6 million (EUR 22.5 million) in revenue last season in Alicante, the influx of imports has raised serious concerns about profitability. In response, local associations have introduced the Aguacates CV seal to promote traceability, quality, and sustainability, starting with the Hass variety and extending to Lamb Hass, which represents over 60% of regional production. As import volumes continue to climb, producers are urging authorities and consumers to support domestically grown avocados to protect local investment and reduce the environmental impact of long-distance trade.

United States

California Projects Significant Avocado Crop Due to High US Import Dependence

California is expected to produce its third-largest avocado crop in a decade for the 2024/25 marketing year, with an estimated 375 million pounds (lbs), up 44% from the three-year average and a 3% year-on-year (YoY) increase. The Hass variety will comprise 95% of this total, further solidifying California’s role in US avocado production, though domestic supply still accounts for only about 10% of national demand. Despite the strong local harvest, the US remains heavily dependent on imports, which reached a record USD 3.8 billion in 2024, mainly from Mexico.

Earlier in the year, temporary supply constraints from Mexico and Peru, and a shortage of larger-sized Mexican avocados, drove prices higher. California’s early and fast-paced harvest, which had already reached 8% of the projected volume by early March, may lead to a shorter season, similar to 2022. Meanwhile, Mexican avocado shipments are expected to continue but could slow mid-year as harvesting shifts to higher-altitude regions.

2. Weekly Pricing

Weekly Avocado Pricing Important Exporters (USD/kg)

Yearly Change in Avocado Pricing Important Exporters (W17 2024 to W17 2025)

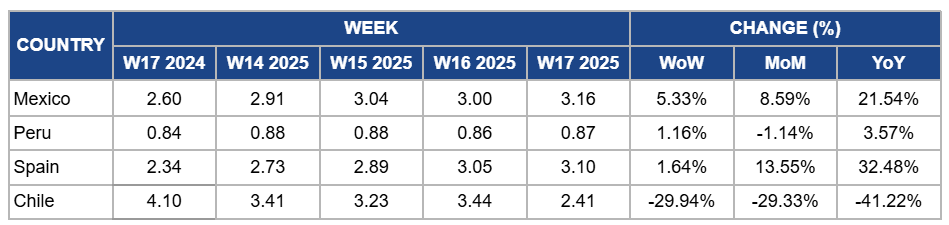

Mexico

In Mexico, avocado prices increased by 5.33% week-on-week (WoW) to USD 3.16/kg in W17, with an 8.59% month-on-month (MoM) and a 21.54% YoY surge. The price rise is due to tightening supplies from key producing states like Michoacán, where the main harvest season for Hass avocados, typically running from October to May, is entering its final stages. As the season winds down in April and May, volumes naturally decline, reducing availability in local and export markets. This seasonal tightening, combined with strong international demand, particularly from the US, has placed upward pressure on prices. Additionally, logistical challenges and increased production costs have contributed to the continued price growth. While expansion efforts in states like Puebla aim to boost long-term output, their current impact on market supply is still limited.

Peru

Peru's avocado prices increased slightly by 1.16% WoW to USD 0.87/kg in W17, reflecting a 3.57% YoY increase. This is due to limited early-season supply as the main harvest was still getting underway, alongside steady demand from key export markets like Europe and the US. The peak harvest months in Peru typically run from April to September, when the country's main export volumes of Hass avocados are available. However, there was a 1.14% MoM decrease, as harvest volumes have started to increase, helping ease the earlier supply constraints and exerting modest downward pressure on prices.

Spain

In W17, avocado prices in Spain increased slightly by 1.64% WoW to USD 3.10/kg, with a 13.55% MoM increase and a 32.48% YoY rise. This upward trend is due to the transition period between the winter and summer avocado supply seasons, which typically peaks around Easter. During this time, the supply from traditional winter origins such as Spain, Portugal, Morocco, Israel, and Chile diminishes, leading to an imbalance between supply and demand, thereby driving prices higher. Additionally, adverse weather conditions in Spain and Morocco have further constrained supply, contributing to the price surge. The market is expected to experience relief starting in W16, with increased volumes from Peru entering the market, although logistical delays due to Cyclone Yaku may temporarily affect this influx.

Chile

Chilean avocado prices dropped by 29.94% WoW to USD 2.41/kg in W17, with a 29.33% MoM decrease and a 41.22% YoY decline. The price decline was driven by increased harvest volumes during Chile’s peak avocado season, which typically runs from August to April, resulting in an oversupply in local and export markets. This surplus coincided with reduced demand from major importers such as Europe and the US, where avocados from competing suppliers like Peru and Mexico were also available. Additionally, favorable weather and improved logistics supported higher yields and more consistent shipments, further pressuring prices downward.

3. Actionable Recommendations

Expand Regional Market Access to Offset Shipping Delays

Avocado exporters in Kenya should actively diversify into regional African and Middle Eastern markets to reduce dependency on long-haul European routes affected by the Red Sea crisis. Targeting closer destinations like the United Arab Emirates (UAE), Saudi Arabia, and Egypt through shorter sea or road freight can maintain export momentum and minimize quality degradation. Exporters can also promote value-added products like cold-pressed avocado oil and frozen avocado pulp to these markets, where demand is growing and logistics are less constrained.

Stagger Harvest Timing to Extend Market Presence

California avocado growers should coordinate with handlers to stagger harvest schedules and avoid peaking too early in the season. Spacing out-picking, especially of mid to late-season Hass blocks, helps maintain supply through periods when Mexican volumes slow down, supporting stronger pricing and prolonged shelf presence. For example, delaying harvest in cooler microclimates or higher-elevation groves can help fill expected mid-year gaps and reduce price pressure caused by overlapping peak volumes.

Prioritize Drought-Resilient Varieties and Irrigation Efficiency

Avocado producers in Andalusia and Valencia should invest in drought-tolerant rootstocks and upgrade irrigation systems to improve resilience. Adopting varieties like Dusa or Toro Canyon, known for their better performance under limited water, can help stabilize yields during dry spells. At the same time, switching to a precision irrigation method, such as drip systems with soil moisture sensors, will optimize water use and reduce losses, ensuring better productivity during recovery and in future dry years.

Sources: Tridge, 20minutos, Agn, California Avocado Commission, Capitalpuebla, Freshfruitportal, Freshplaza, Gobiernodecanarias, Msn, Redagricola, Todoalicante