In W17 in the soybean oil landscape, some of the most relevant trends included:

- Argentina's soybean oil exports exceeded expectations in Mar-25, driven by strong demand from India and Nepal. Future processing capacity is expected to rise with the Vicentin plant's reopening.

- Brazil’s record harvest is cementing its role as a top global supplier, with rising Chinese demand reinforcing that position. However, stable domestic processing remains crucial to support prices under the 14% biodiesel mandate.

- US soybean oil prices rose on strong biodiesel demand, but escalating trade tensions with China are weakening export prospects, increasing domestic pressures and raising oversupply risks if high crushing levels persist.

- In Bangladesh, CAB alleged that a local soybean oil syndicate is inflating prices despite falling global rates, calling for stricter regulation. Domestic prices remain significantly above international benchmarks.

- Paraguay's soybean oil output is set to grow in MY 2025/26 due to improved weather and higher crushing volumes. However, high costs, credit constraints, and river transport delays hamper expansion, making export growth heavily dependent on external factors like Argentine supply and global prices.

1. Weekly News

Argentina

Argentina Surpassed Soybean Oil Export Forecasts in Mar-25

In Mar-25, Argentina's soybean oil exports exceeded forecasts, reaching 485,000 metric tons (mt), with India and Nepal accounting for over half the volume. The resumption of operations at the Vicentin plant is expected to further boost soybean and sunflower processing capacity this year. As of W17, Argentine crude soybean oil is priced at USD 998 to 1,000/mt free-on-board (FOB). Meanwhile, May-25 soybean oil futures on the Chicago Board of Trade (CBOT) rose 1% to USD 1,060/mt, marking a 14% month-on-month (MoM) gain amid optimism over increased United States (US) biodiesel production. However, global vegetable oil markets may face downward pressure due to rising seasonal supply and cautious import demand.

Bangladesh

CAB Urges Crackdown on Soybean Oil Syndicate Amid Price Manipulation and Supply Restrictions

The Consumers Association of Bangladesh (CAB) has called for immediate and strict government action against the soybean oil syndicate accused of artificially inflating prices and restricting supply. Despite policy support measures such as duty waivers and value-added tax (VAT) reductions, CAB claims that several dominant companies have created an artificial crisis, pushing for a further USD 0.058 per liter (BDT 7/L) price increase after an already approved USD 0.12/L (BDT 14/L). CAB highlighted the disconnect between falling global soybean oil prices, from USD 1,667/mt in 2022 to USD 1,022/mt in 2024, and rising domestic prices, with loose oil selling at USD 1.48/L (BDT 180/L) as of W17, above the official rate.

Brazil

Brazil to Expand Soybean and Soybean Oil Exports During US-China Trade Dispute and Record Harvest

Amid the ongoing US-China trade dispute, Brazil is set to expand soybean exports to China and increase soybean meal shipments to key markets in Europe, the Middle East, and Southeast Asia, according to the Brazilian Association of Vegetable Oil Industries (Abiove). A record harvest of nearly 170 million metric tons (mmt) is expected to strengthen Brazil's position as the world's leading soybean producer and exporter. Abiove also anticipates increased soybean oil exports, supported by strong domestic processing and the government's decision to maintain the 14% biodiesel blending mandate. These developments are projected to boost the agribusiness sector's gross domestic product (GDP) in 2025.

Paraguay

Paraguay's Soybean Oil Output to Rise in MY 2025/26 Following Rebound in Production and Crushing Capacity

Paraguay's soybean oil production is projected to rise in the marketing year (MY) 2025/26, supported by a rebound in soybean output to 10.9 mmt due to improved weather and a slight expansion in planted area. Increased crushing, forecast at 3.4 mmt, will boost soybean oil and meal output, with exports continuing to play a dominant role. However, growth remains limited by high input costs, restricted access to credit, and persistent shipping delays caused by low river levels restricting vessel passage. Export prospects will depend heavily on developments in Argentina, global prices, and seasonal weather conditions.

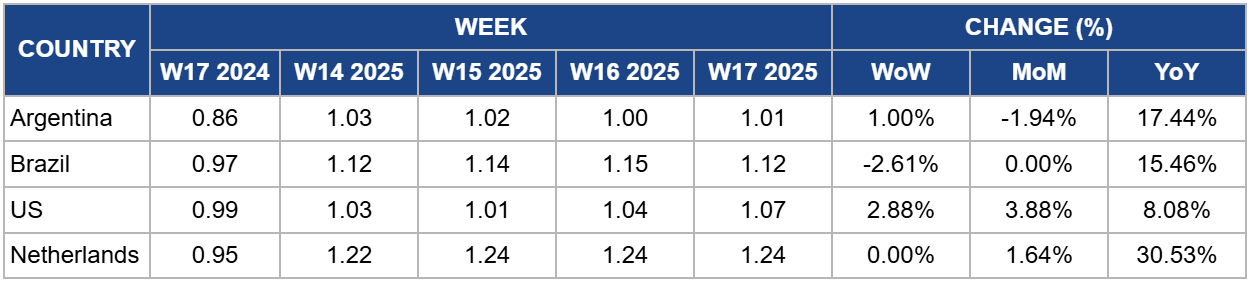

2. Weekly Pricing

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

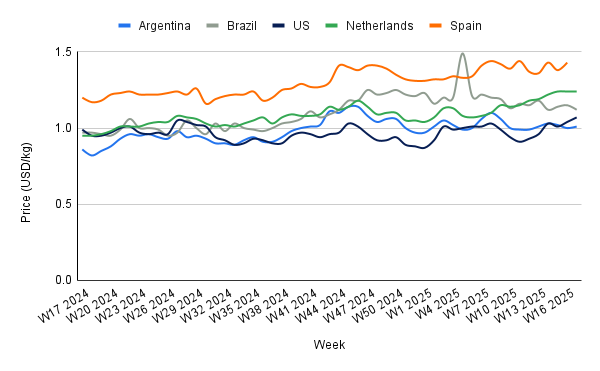

Yearly Change in Soybean Oil Pricing Important Exporters (W17 2024 to W17 2025)

Argentina

In W17, Argentina’s soybean oil prices rose to USD 1.01 per kilogram (kg), reflecting a 1% week-on-week (WoW) increase and a 17.44% year-on-year (YoY) gain. This price uptick comes amid weather-driven harvest delays, with heavy rains in Mar-25 and early Apr-25 pushing soybean harvesting below the five-year average. Although upcoming dry weather may accelerate harvesting, only 23.4% of the 2024/25 crop had been sold by mid-Apr-25, the slowest pace in ten years, limiting processing flow. Soybean processing is forecast to decline by 3.5% to 41.5 mmt for the current year, yet output remains strong relative to historical norms. Soybean oil production is estimated at 8.2 mmt for 2024/25, down from 2023/24 but still above the five-year average.

Despite this, sustained demand from key importers such as India, Bangladesh, China, Peru, and Mozambique, will be essential to stabilize prices. Without stronger international buying or disruptions among competitors, Argentine soybean oil prices are likely to remain constrained in the near term. However, robust export volumes and Argentina's dominant role in the global soybean oil market may offer moderate support in the medium term.

Brazil

Brazil's soybean oil prices declined to USD 1.12/kg in W17, reflecting a 2.61% WoW drop and a 15.46% YoY increase from USD 0.97/kg. Despite this short-term price correction, strong external demand—particularly from China—continues to underpin market fundamentals. China has ramped up purchases from Brazil as it shifts away from US suppliers in response to new tariffs, indicating a longer-term realignment in global soybean oil trade flows.

Abiove attributes this demand surge to geopolitical tensions and a record soybean harvest of nearly 170 mmt, which has reinforced Brazil’s export capacity. However, Abiove stresses the importance of sustaining domestic processing to ensure stable supplies of soybean oil and biodiesel, especially under the government’s 14% biodiesel blending mandate. International demand may support prices in the medium term, but weaker domestic processing or rising global supply could limit further gains.

United States

In W17, US soybean oil prices rose to USD 1.07/kg, an increase of 2.88% WoW and an 8.08% YoY rise, supported by firm domestic demand amid tightening export prospects. Trade tensions with China, marked by tariffs and import suspensions, have reduced US export potential, redirecting more supply to the domestic market and straining inventories. While renewable diesel demand continues to support prices, the market’s limited capacity to absorb surplus raises oversupply concerns if crushing remains high. Competitive pressure from Brazil and persistent trade friction may cap future gains, despite strong global oilseed prices and early export commitments.

Netherlands

Soybean oil prices in the Netherlands held steady at USD 1.24/kg in W17, with no weekly changes, experiencing a 30.53% YoY increase amid firm domestic and regional demand. As a key European Union (EU) import hub, the Netherlands may face supply risks following the EU's approval of retaliatory tariffs on US agricultural goods, including soybeans. If implemented, reduced US shipments could tighten crushing margins and maintain upward pressure on prices, especially given already constrained global supplies and elevated geopolitical uncertainty

3. Actionable Recommendations

Enhance Procurement Strategies Amid Shifting Trade Flows

With Argentina's strong export momentum and Brazil's rising dominance in the Chinese market, buyers in Asia, the EU, and the Middle East should diversify procurement beyond traditional suppliers. Establishing flexible contracts with both countries can help hedge against price volatility and mitigate risks from US-China trade tensions and seasonal supply surges.

Address Domestic Price Inefficiencies in South Asia

Given the disconnect between falling global soybean oil prices and persistently high retail prices in Bangladesh, local regulators and importers should improve transparency across the supply chain. Strengthening market oversight, implementing digital price-tracking tools, and ensuring fair competition can enhance price transmission and protect consumers from artificial markups.

Leverage Storage and Forward Contracts to Stabilize Supply

In light of seasonal harvest delays in Argentina and logistical challenges in Paraguay, major importers should expand regional storage infrastructure and secure forward contracts with key exporters. These measures would improve supply reliability and help buffer domestic markets against short-term disruptions and global price corrections.

Sources: Tridge, Dhaka Tribune, Yahoo! Finanzas, Grain Trade, Oil World