In W18 in the apple landscape, some of the most relevant trends included:

- Apple prices are rising in Europe due to strong demand and tight supplies, with countries like Germany and Poland showing notable increases. Meanwhile, apple prices in India have dropped due to transport disruptions and oversupply.

- Argentina’s apple consumption has declined due to economic challenges, subpar quality, and limited marketing efforts. The demand for imported apples in the US is down due to an ample domestic supply.

- In India, transport disruptions and unsold inventory in Kashmir's storage are creating challenges for apple growers. The US faces logistical uncertainties with imports and the potential impact of tariffs.

- Pennsylvania's apple harvest is on track for a smooth transition, supported by good weather conditions and stable demand despite ongoing economic pressures and tariff concerns.

1. Weekly News

Argentina

Argentina's Apple Consumption Declines Due to Economic Challenges and Quality Issues

According to the National Service of Agri-Food Health and Quality (SENASA), local apple sales in Argentina fell to 54.5 thousand tons in the first quarter of the year (Q1-25). This marks a 1.2% year-on-year (YoY) decline and a 5.9% drop compared to the 2020/24 seasonal average. Although total apple sales reached 116.2 thousand tons, up nearly 20% from the previous year, this growth was driven primarily by exports (over 18.4 thousand tons) and processing (43.18 thousand tons), rather than fresh market consumption. The decline in local demand is due to reduced consumer purchasing power, subpar fruit quality, with only 15% meeting expectations, smaller harvest volumes, and limited marketing efforts. Despite apples being a long-standing staple in the Argentine diet, ongoing economic challenges and stagnant spending are expected to keep domestic demand subdued through 2025.

Europe

European Apple Prices Rise Above Seasonal Averages

According to the European Commission (EC), the average apple price for European producers rose to USD 1.10 per kilogram (EUR 0.97/kg) in Mar-25. This represents a 4.5% YoY increase and a 22.7% rise compared to the five-year March average. Germany saw the strongest price momentum, with figures rising from USD 0.93/kg (EUR 0.82/kg) in Jan-25 to USD 0.98/kg (EUR 0.87/kg) in Mar-25. Meanwhile, Poland demonstrated a steady price recovery, increasing from USD 0.78 to 0.81/kg (EUR 0.69 to 0.72/kg) during the same period. France reported the highest prices despite a gradual decline since Sep-24, and Italy maintained stable levels, albeit slightly below last year’s figures. These price trends point to strong demand and tighter supplies in early 2025, keeping European apple prices above historical norms.

India

Apple Prices Drop in India Due to Highway Disruptions and Oversupply

India's apple prices have recently dropped due to transport disruptions on the Jammu-Srinagar National Highway caused by landslides following a cloudburst, which delayed shipments and created a sudden oversupply in wholesale markets. As a result, 10- to 15-kg apple cartons are selling for USD 1.80 to USD 2.40 (INR 150 to 200) below normal rates, affecting both farmers and traders. Although the season began strongly, around 6 million cartons, which are approximately 30 to 40% of the harvest, remain unsold in Kashmir’s controlled-atmosphere storage facilities, which now hold over 500 thousand metric tons (mt). The ongoing lack of refrigerated transport and reliable road access continues to challenge growers, who are hoping for improved logistics and market recovery soon.

United States

US Apple Imports Face Lower Demand Due to Ample Local Supply

Demand for imported apples in the United States (US) is projected to decline this year, due to high domestic supply from Washington, which maintains substantial inventory from the 2024 harvest despite a slightly smaller crop. While demand for Honeycrisp remains steady amid localized shortages, interest in staple varieties like Fuji and Gala has softened. Typically, imported apples from Chile and New Zealand arrive between May-25 and Jun-25, but lower-than-usual volumes are expected unless Washington accelerates its sales. Adding to the cautious import outlook, uncertainty over potential tariffs prompts US retailers to hold back on overseas purchases.

Pennsylvania Prepares for Smooth Apple Harvest Transition in 2025

Pennsylvania’s 2025 apple crop has reached full bloom, with recent warm weather supporting strong pollination and keeping growing conditions on pace with last year. The transition from the 2024 harvest is expected to be smooth, with steady summer supplies of popular varieties such as Red Delicious, Golden Delicious, Fuji, Gala, Pink Lady, and Granny Smith. Despite ongoing economic pressures and tariff-related uncertainties, demand for Pennsylvania apples remains firm, driven by their versatility, storability, and year-round consumer appeal. Pricing has remained stable despite rising production costs, as growers focus on streamlining operations and positioning for a successful new season.

2. Weekly Pricing

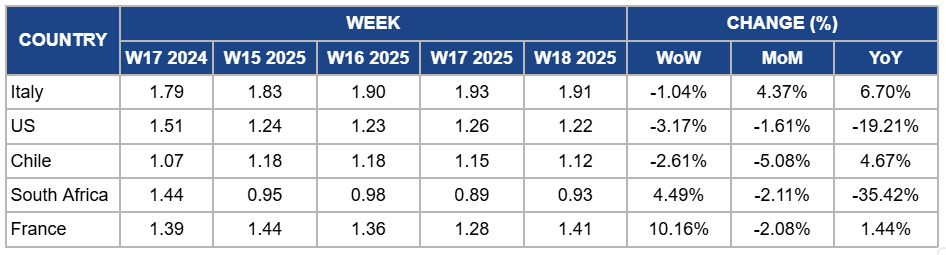

Weekly Apple Pricing Important Exporters (USD/kg)

Yearly Change in Apple Pricing Important Exporters (W18 2024 to W18 2025)

* Varieties: US and Italy (Gala), Chile, South Africa, and France (Granny Smith)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

Italy

In W18, apple prices in Italy declined by 1.04% week-on-week (WoW) to USD 1.91/kg, due to a slight dip in demand following the Easter holiday and the ongoing availability of stored apples from the 2024 harvest. This temporary oversupply and stable local consumption exerted downward pressure on prices. However, month-on-month (MoM) and YoY prices increased by 4.37% and 6.70%, respectively, driven by strong pricing trends in early 2025. Between January and March, Italian apple prices remained relatively stable at high levels, USD 109.88/100 kg (EUR 98/100 kg) in Jan-25, USD 108.76/100 kg (EUR 97/100 kg) in Feb-25, and USD 107.64/100 kg (EUR 96/100 kg) in Mar-25, slightly below the same period last year but still significantly above the five-year average, indicating continued strong market conditions for Italian apples.

United States

In the US, apple prices declined by 3.17% WoW in W18 to USD 1.22/kg, with a 1.64% MoM drop and a 19.21% YoY decrease. This downward trend is due to an oversupply in the local market, particularly from Washington state, which continues to hold substantial inventory from the 2024 harvest. Despite a slightly smaller crop in 2025, the carryover has led to softer demand for imported apples, especially staple varieties like Fuji and Gala, further exerting downward pressure on prices. Additionally, uncertainties surrounding potential tariffs have made US retailers cautious, prompting them to delay or reduce overseas purchases, thereby affecting overall market dynamics.

Chile

Chile's apple prices decreased by 2.61% WoW to USD 1.12/kg in W18, marking a 5.08% MoM decline. This downward trend is due to an anticipated 4.4% increase in apple shipments for the 2025 season, totaling approximately 573.6 thousand tons. The surge in supply, particularly of red varieties, has exerted downward pressure on prices. However, YoY prices have increased by 4.67%, likely due to improved fruit quality driven by favorable climatic and production conditions, which have enhanced the market value of certain premium apple varieties.

South Africa

In W18, South Africa's apple prices increased by 4.49% WoW to USD 0.93/kg, due to strong demand in European markets. This demand is driven by a 9.7% reduction in the European apple harvest and a 4.3% decrease in stocks as of Jan-25. South African exporters have capitalized on this opportunity, particularly in markets like Germany, where retailers are actively sourcing high-quality imports to fill the supply gap. However, prices dropped by 2.11% MoM and 35.42% YoY due to an anticipated 5% increase in South Africa's apple exports for the 2025 season, reaching approximately 51.3 million cartons. This surge in supply, bolstered by favorable weather conditions and the expansion of high-yielding orchards, has exerted downward pressure on prices.

France

Apple prices in France surged by 10.16% WoW to USD 1.41/kg in France, with a 1.44% YoY increase. This rise is attributed to a gradual recovery in prices during early 2025, as prices increased from Jan-25 to Mar-25, aligning closely with the previous year and consistently outpacing the five-year average, suggesting resilient market performance. However, there was a 2.16% MoM drop due to higher production levels or weakening consumer demand, leading to a gradual decrease in prices.

3. Actionable Recommendations

Prioritize Fresh Market Quality and Targeted Promotion

Apple producers in Argentina must focus on improving fruit quality and increasing fresh market appeal to recover declining local sales. This includes enhancing orchard management to deliver better-quality apples and investing in post-harvest handling to reduce bruising and defects. Producers should also implement targeted marketing strategies, such as in-store tastings, bundled family deals, or nutrition-based promotions, to reconnect with budget-conscious consumers. By aligning quality with demand and boosting visibility at the point of sale, producers can better compete with processed alternatives and revive interest in fresh apples.

Expand Cold Chain and Diversify Market Routes

Apple producers in India should invest in decentralized cold storage facilities and build relationships with alternative regional buyers to reduce reliance on single transport corridors. This includes setting up smaller cold rooms closer to orchards and collaborating with private logistics firms to create backup delivery routes during disruptions. Producers can also explore regional wholesale markets outside the main hubs to avoid sudden gluts. For example, selling to second-tier cities or institutional buyers like schools and hotels can help maintain cash flow and reduce storage overflow during delays.

Sources: Tridge, Australian Fresh Produce Alliance, Greater Kashmir, Freshfruitportal, Freshplaza, MASP, RU Interfax