1. Weekly News

United States

Vegetable Oil Price Index Reaches 13-Month High in Apr-24

The Vegetable Oil Price Index of the United States (US) Food and Agriculture Organization (FAO) averaged 130.9 points in Apr-24, rising by 0.3% (0.3 points) month-on-month (MoM) and reaching its highest level in 13 months. Global soybean oil prices decreased after a brief recovery, indicating the potential for significant South American supplies due to a favorable outlook for soybean production.

Soybean Oil Futures Prices in Chicago Surged by 3.2% in W19

In W19, soybean oil futures prices in Chicago surged by 3.2% week-on-week (WoW) to reach USD 980 per metric ton (mt). Simultaneously, on the Dalian Stock Exchange in China, the most actively traded contract for soybean oil experienced a 1.51% increase on May 7, 2024. Moreover, India's soybean oil imports substantially declined by 48% to 233 thousand mt in Apr-24. According to Trading Economics, the average price of sunflower oil dropped by 0.7% during the week to USD 851/mt.

USDA Anticipated Increase in Soybean Oil Usage for Biofuel Production

According to the latest World Agricultural Supply and Demand Estimates Report released by the United States Development of Agriculture (USDA) on May 10, 2024, soybean oil usage in biofuel production is anticipated to increase by 1 billion pounds (lbs) to 14 billion lbs for the 2024/25 season. This surge reflects a growing demand for soybean oil as a feedstock for biofuel production. Additionally, the overall outlook for US soybeans in the 2024/25 season indicates higher supplies, crushes, exports, and ending stocks than the previous year. Specifically, the US soybean crush for the 2024/25 season is projected at 2.43 billion bushels, marking a 125 million bushel increase from the 2023/24 forecast. This uptick is driven by the rising demand for soybean oil in the biofuel sector.

Argentina

Soybean Crushing in Argentina Reaches 7.4 mmt in Q1-2024

The Argentine Chamber of the Oil Industry and Cereal Exporters Center (CIARA-CEC) reported that soybean crushing in Argentina reached 7.4 million metric tons (mmt) in the first quarter of 2024. This was the second-highest level since 2016, when a record 10.3 mmt were crushed. In particular, the country processed 2.907 mmt of soybeans in Mar-24, an increase of 18.82% MoM compared to 2.36 mmt in Feb-24.

Egypt

Egypt's GASC Vegetable Oils Tender Results

On May 9, 2024, the Egyptian General Authority for Supply Commodities (GASC) conducted an international tender to acquire 40 thousand mt of vegetable oils slated for delivery in Jun-24. The plan included purchasing 30 thousand mt of soybean oil and 10 thousand mt of sunflower oil. Compared to the previous tender on March 28, 2024, there was a noticeable uptick in the bids received, particularly for soybean oil. Moreover, the bid prices for soybean oil decreased. Consequently, GASC finalized the purchase of 73 thousand mt of sunflower oil at USD 1,000/mt and 29 thousand mt of soybean oil at USD 994/mt

2. Weekly Pricing

Weekly Soybean Oil Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Oil Pricing Important Exporters (W19 2023 to W19 2024)

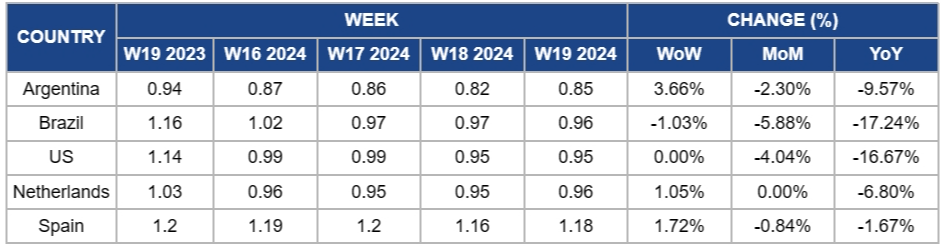

Argentina

Soybean oil prices in Argentina experienced a 3.66% WoW increase to USD 0.85 per kilogram (kg) in W19. The fluctuation can be attributed to increased future prices affected by negative production forecasts in Brazil. However, the prices are expected to fall again due to solid supply in South America and favorable production prospects.

Brazil

Brazil's soybean oil prices decreased by 1.03% WoW to USD 0.96/kg in W19. In addition, the prices dropped by 5.88% MoM and 17.24% year-on-year (YoY). The downward trend is driven by the demand deficit for biofuel blending and the favorable production prospects.

United States

In W19, soybean oil prices in the US remained unchanged from W18 at USD 0.95/kg. However, in this week, Jul-24 shipments futures in Chicago surged by 3.2% to USD 980/kg due to a potential production loss in Brazil.

Netherlands

Soybean oil prices in the Netherlands increased slightly by 1.05% WoW to USD 0.96/kg. However, the prices are unlikely to be sustained due to the country's regional oversupply and weak demand. In addition, biodiesel prices in the European region also declined due to the lower palm oil prices and regulatory changes in the European Union (EU).

Spain

Soybean oil prices in Span increased by 1.72% WoW to USD 1.18/kg in W19. However, based on monthly and yearly compassion, the prices declined by 0.84% MoM and 1.67% YoY respectively. This price fluctuation can be attributed to increased future prices affected by negative production forecasts in Brazil.

3. Other Outstanding Price Anomalies

Soybean Oil Prices in Shanghai Decreased by 4.27% YoY Amidst Decrease Imported Soybean Prices and Weak Demand

In W19, the wholesale price of first-grade soybean oil prices in Shanghai, China, decreased by 4.27% YoY to USD 1.59/kg compared to USD 1.66/kg in the same period last year. However, based on a weekly comparison, the price remained unchanged, and the current price trend is consistent with the prices in 2023.

The decreased imported soybean prices and weak demand are the primary reasons for the price drop. In the first three months of 2024, China's soybean imports reached 18.58 mmt, and the average import prices decreased by 15.8% YoY. Additionally, China's soybean oil futures prices have been declining since the beginning of 2024. In Jan-24, soybean prices dropped by 4.52% MoM and experienced a slight recovery in Feb-24 and Mar-24. However, the prices started falling again by the end of Mar-24. Considering the current sufficient supply and a good production forecast in Brazil and the US, the prices will likely decline.

4. Actionable Recommendations

Monitor International Price Trends

Given the recent increases in the FAO Vegetable Oil Price Index, soybean traders and producers should closely monitor international price trends to capitalize on favorable market conditions. Regularly tracking indices such as the FAO Vegetable Oil Price Index and commodity futures prices can provide valuable insights for decision-making.

Focus on Export Opportunities

With GASC in Egypt conducting an international tender to acquire vegetable oils, traders and producers should actively explore export opportunities in emerging markets. Participating in such tenders and securing contracts for delivery can help diversify revenue streams and expand market reach.

Monitor Imports Trends and Local Demand in China

Given the fluctuation in soybean oil prices and market dynamics in China, stakeholders should focus on monitoring China’s import trends and developing risk management strategies to mitigate price fluctuations and uncertainty. With the decrease in imported soybean prices and weak demand, it is essential to prepare for further price declines. In addition, the current soybean oil inventory in China has reached a low level and is expected to recover this month. The increased stock will bring further pressure on prices.

Diversify Supply Sources

To mitigate risks associated with supply chain disruptions or geopolitical uncertainties, traders and producers should diversify their supply sources. Establishing relationships with multiple suppliers across different regions can ensure a reliable and resilient supply chain.