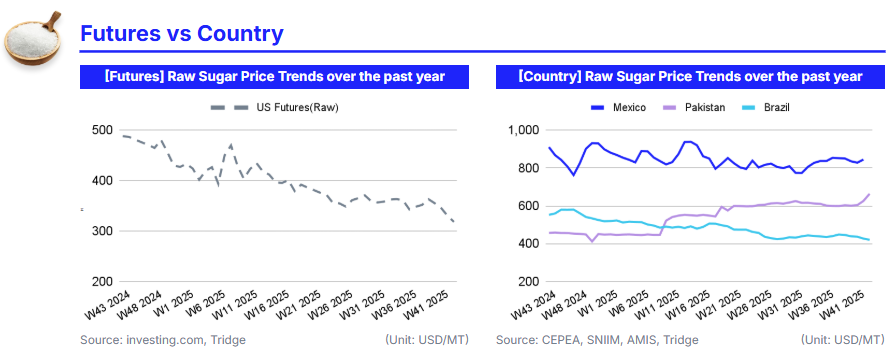

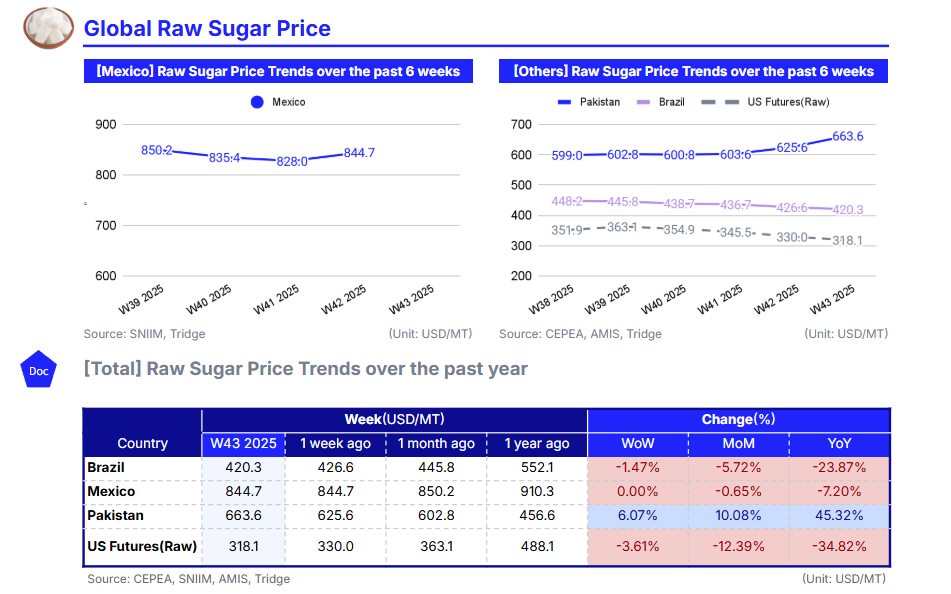

As of W43 2025, Brazil’s sugar market continued to weaken under pressure from record output and currency-driven export constraints. Domestic prices fell to USD 420.3/mt, down 23.87% YoY, as mills in the Center-South region maintained high sugar output shares despite reduced cane crushing. US raw futures reflected the same trend, declining 3.61% WoW to USD 318.1/mt, with New York raw sugar for Mar-26 closing at 14.32 cents/lb and London white sugar at USD 414.7/mt, near multi-month lows. Analysts expect the 2025/26 global surplus to reach 4.1–10.5 mmt, indicating that the current weakness is structural rather than temporary.

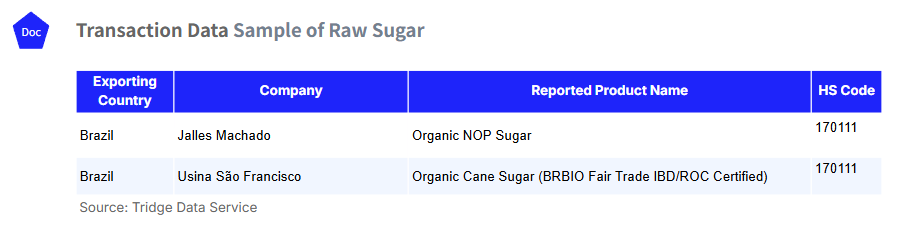

Global industrial food and beverage manufacturers sourcing sugar should take advantage of Brazil’s price decline by securing forward and fixed-price contracts below USD 430/mt. The core strategy is to secure medium-term supply while prices remain depressed, mitigating exposure to potential logistical or weather-related disruptions later in Q4-2025. For organic and sustainable sourcing, companies are encouraged to contract with exporters such as Jalles Machado (Organic NOP Sugar) and Usina São Francisco (Organic Cane Sugar, BRBIO Fair Trade IBD/ROC Certified), both known for reliable export volumes and traceable supply chains.

1. Weekly Price Overview

Global Sugar Prices Slide Further as Oversupply and Strong Real Weight on Brazilian Exports

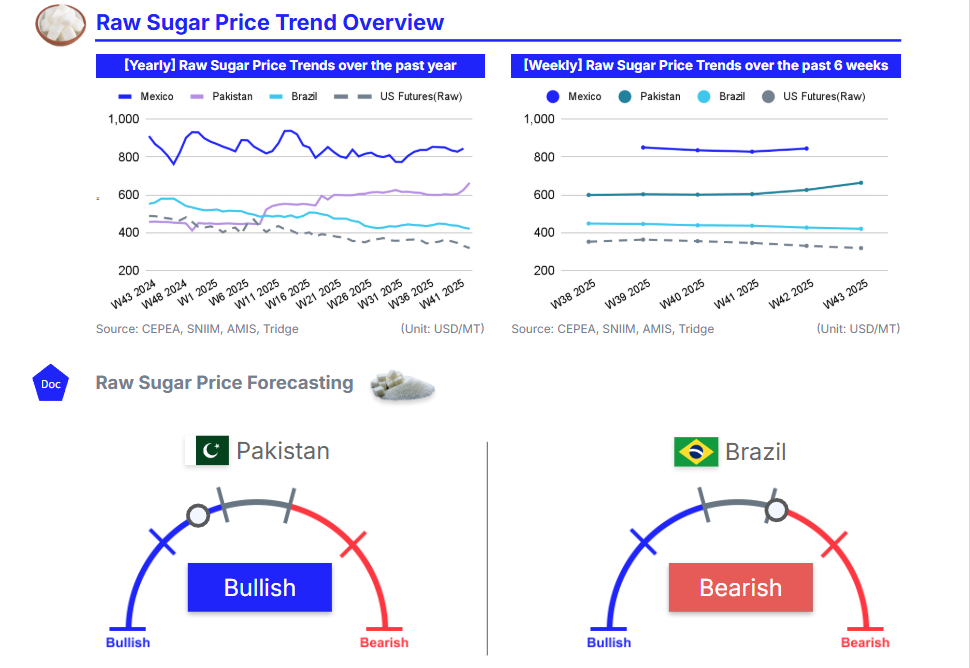

In W43 2025, global sugar prices remained under downward pressure amid rising supply and currency-driven adjustments. Brazil’s sugar prices declined by 1.47% week-on-week (WoW) to USD 420.3 per metric ton (mt), marking a 23.87% year-on-year (YoY) decrease. The fall reflects abundant supply and an anticipated global surplus of 4.1 million metric tons (mmt) for the 2025/26 season. In the domestic market, CEPEA/ESALQ reported a 1.01% decline in white crystal sugar prices in São Paulo to USD 21.58 per 50-kilogram (kg) bag (BRL 116.17/50-kg bag), as mill inventories built up and only Icumsa 150 sugar maintained price stability. The appreciation of the Brazilian real further weakened export competitiveness, prompting an increase in domestic availability and additional downward pressure on prices.

US raw sugar futures dropped 3.61% WoW to USD 318.1/mt, pressured by weak demand, uneven harvest progress, and falling global benchmarks. The Mar-26 contract fell 0.89% to 15.58 cents per pound (lb). The early-week decline followed renewed expectations of oversupply, although stronger Chinese demand and imports up 36% YoY in Sep-25 to 550,000 mt offered limited short-term support.

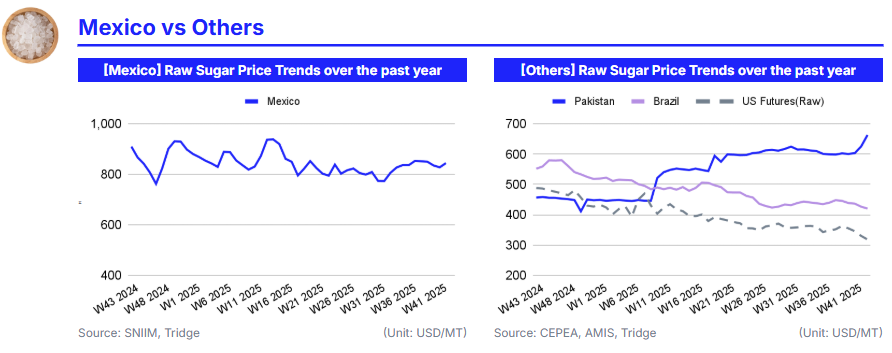

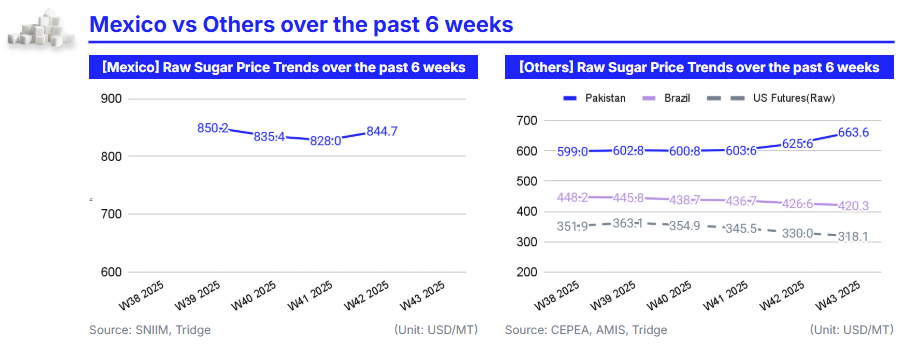

Mexico’s sugar prices held steady at USD 844.7/mt with no weekly changes, but experienced a decline of 7.2% YoY, as the government confirmed an unchanged export quota to the US at 199,251 mt for the 2025/26 cycle despite a negative Sep-25 adjustment in the WASDE report. Pakistan’s sugar market remained volatile, with prices surging 6.07% WoW to USD 663.6/mt, up 45.32% YoY, as delayed crushing and higher transport costs drove retail prices to record highs.

The sugar market remains bearish, weighed down by robust Brazilian output, a strengthening real, and forecasts of global surplus. However, strong Asian import activity and potential weather disruptions in the coming months could moderate the downward trajectory.

2. Price Analysis

Brazilian Sugar Falls as Record Output and Strong Real Deepen Global Oversupply

Brazil’s sugar prices declined to USD 420.3/mt in W43, down 5.72% month-on-month (MoM) from USD 445.8/mt, as strong production and export activity reinforced a supply-heavy global market. Data from the Brazilian Sugarcane Industry Association (UNICA) showed that sugar output in Brazil’s Center-South region rose 1.3% YoY in early Oct-25 to 2.484 mmt, despite a 2.78% decrease in total cane crushed. Mills maintained high sugar production shares in the output mix, contributing to an oversupplied domestic and international market. This persistent output strength, combined with the appreciation of the Brazilian real, which reduced export competitiveness, has increased local availability and limited price support.

Global fundamentals continue to signal a bearish tone. Forecasts by BMI Group and Covrig Analytics project a 2025/26 global surplus ranging from 4.1 to 10.5 mmt, suggesting that the recent price drop is more structural than temporary. Futures performance supports this trend, with New York raw sugar for Mar-26 closed at 14.32 cents/lb, and London white sugar at USD 414.7/mt, both near multi-month lows. The bearish momentum is reinforced by record supply from Brazil and improving production outlooks in India and Thailand, which together account for a substantial portion of global exports.

Looking ahead, sugar prices are likely to remain under downward pressure through Q4-2025, with limited room for recovery unless weather disruptions or ethanol price spikes alter Brazil’s production mix. Given that the 2026/27 Center-South crush is projected to reach a record 44 mmt (+3.9% YoY), the market is expected to stay supply-driven. However, temporary rebounds could occur if logistical bottlenecks or seasonal rains slow exports. Overall, the short-term outlook for Brazil’s sugar remains bearish, with global benchmark prices likely to hover between USD 400–430/mt through year-end before stabilizing modestly in early 2026.

3. Strategic Recommendations

Capitalize on Brazil’s Sugar Price Decline to Secure Low-Cost Supply and Protect Against Future Volatility

Global sugar importers and industrial users should capitalize on Brazil’s current price decline, as sustained oversupply and currency-driven export constraints continue to depress prices. With domestic prices falling to USD 420.3/mt in W43 2025 and global futures hovering near multi-month lows, this period presents a strategic procurement window before potential logistical or weather-related disruptions in late Q4-2025. UNICA reported continued production growth in the Center-South region, with mills maintaining a high share of sugar output, reinforcing structural oversupply across export markets. As a result, buyers can expect stable to lower prices in the short term, with limited upside potential unless ethanol demand strengthens or the real weakens.

Importers in Asia, the Middle East, and Africa should secure forward contracts for both conventional and organic sugar through Brazilian exporters while prices remain below USD 430/mt. According to Tridge Eye data, for high-value and sustainable segments, buyers should consider sourcing from Jalles Machado (Organic NOP Sugar) and Usina São Francisco (Organic Cane Sugar, BRBIO Fair Trade IBD/ROC Certified), both of which maintain consistent export volumes and traceability standards. Locking in multi-month supply agreements with these producers would hedge against potential freight cost increases and port congestion in Santos and Paranaguá.

Traders and refiners are advised to hedge against further downside through short futures or put options on ICE raw sugar for Mar-26 delivery, currently near 14.32 cents/lb. Conversely, industrial buyers seeking to secure low-cost inventory could use call spreads to protect against potential price rebounds if rains or ethanol price spikes shift Brazilian mills’ output mix. The current market offers a favorable environment for buyers to accumulate medium-term stocks at a discount, while producers should prioritize currency hedging to mitigate real appreciation risks through early 2026.