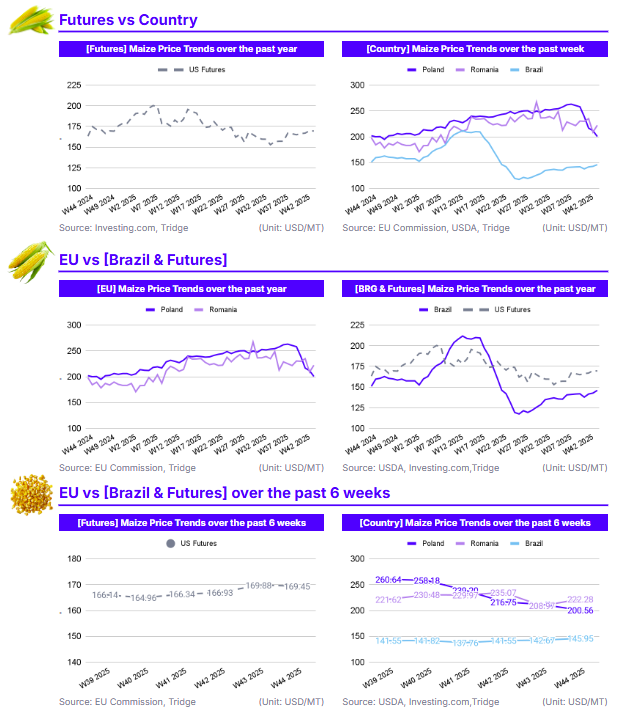

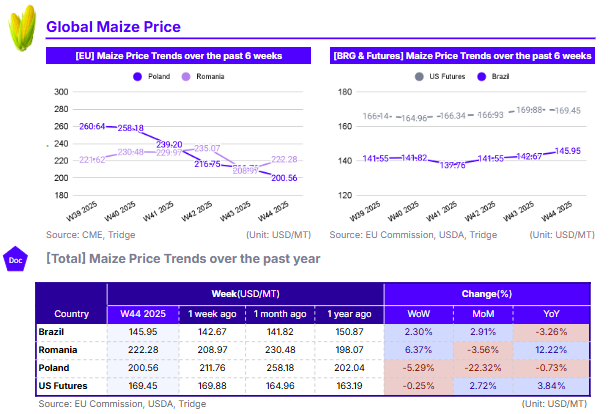

In W44 2025, maize prices showed significant divergence, especially in European markets, where harvest outcomes drove price movements. Poland’s price fell 5.29% WoW and crashed 22.32% MoM to USD 200.56/mt, as a large 9 mmt harvest pressured the market. Conversely, Romania’s price rose 6.37% WoW to USD 222.28/mt, with prices up 12.22% YoY due to a severe, drought-reduced harvest. In the Americas, prices were firmer. US Futures were stable at USD 169.45/mt, supported by export demand which balanced a massive 16.8 billion bushel crop. Brazil’s price rose 2.30% WoW to USD 145.95/mt amid strong export and domestic demand. Buyers are advised to target Poland for cost-effective EU supply and the well-supplied US for large-volume contracts.

1. Weekly Price Overview

Diverging Weather Emerges as Primary Price Driver in Europe

Major European maize producers have been experiencing diverging price trends in recent weeks. In Romania, the price of maize rose sharply by 6.37% week-on-week (WoW) to USD 222.28 per metric ton (mt). Conversely, Poland’s price continued to fall, declining 5.29% WoW to USD 200.56/mt. Meanwhile, in the Americas, Brazil’s price was USD 145.95/mt, a 2.30% increase WoW, while US Futures were nearly flat, declining 0.25% WoW to USD 169.45/mt.

The significant WoW divergence in the European Union (EU) is a direct result of conflicting harvest realities. Romania’s 6.37% WoW price spike is driven by severe supply concerns as a summer drought has slashed yield forecasts to near-record lows. Furthermore, heavy October rains have since hampered the harvest of the already diminished crop. In contrast, Poland’s 5.29% WoW price drop reflects sustained harvest pressure. Favorable weather is contributing to a large 2025 harvest, estimated at 9 million metric tons (mmt), which is 8.49% above the five-year average. This high supply levels is weighing on prices. Brazil's 2.30% WoW gain is supported by strong export demand coupled with downward revised harvest expectations as its 2025/26 planting (72% complete) progresses in line with last year. The United States (US) market remains relatively stable as it awaits the November WASDE report, the first official data in weeks following the government shutdown.

2. Price Analysis

Poland's Harvest Glut Triggers MoM Price Crash While Adverse Weather in Romania Supports YoY Gains

In Poland, the price of maize fell 22.32% month-on-month (MoM), bringing the W44 2025 price to USD 200.56/mt and resulting in a 0.73% year-on-year (YoY) decline. In Romania, the price was USD 222.28/mt, down 3.56% MoM but maintaining a strong 12.22% YoY gain. US Futures rose 2.72% MoM to USD 169.45/mt and are up 3.84% YoY. Brazil's price increased 2.91% MoM to USD 145.95/mt, though it remains 3.26% lower YoY.

The -22.32% MoM crash in Poland is the most significant long-term movement, directly reflecting the impact of its large 2025 harvest. An estimated 9 mmt of production (8.49% above the 5-year average) has hit the market, creating a supply glut that has erased the past year's price gains. In sharp contrast, Romania’s 12.22% YoY strength highlights its severe domestic supply shortfall. A summer drought is expected to reduce its 2025 harvest to only 6 mmt, 32.46% below the five-year average, creating a much tighter market compared to last year. The modest 3.56% MoM dip likely reflects a minor correction as harvest and demand expectations are adjusted.

The MoM gains in the US (+2.72%) and Brazil (+2.91%) are supported by strong demand. The US market is buoyed by persistent export demand balancing the expected large crop. Brazil's MoM rise is similarly linked to strong export expectations and growing domestic demand from its corn ethanol sector as 2025/26 planting progresses. Furthermore, national supply company Conab downgraded their maize harvest expectation in Brazil for the 2025/26 season, putting further upward pressure on prices.

3. Strategic Recommendations

Target Poland for Cost-Effective EU Maize Procurement

European buyers and importers seeking to secure maize within the EU should prioritize Poland as a primary sourcing origin. This recommendation is driven by Poland's strong 2025 harvest, which contrasts sharply with poor production in other key EU regions. Favorable weather has resulted in a large Polish harvest, estimated at 9 mmt, which is 8.49% above the five-year average. This influx of supply has created significant downward price pressure, with Polish prices collapsing 22.32% MoM to USD 200.56/mt. This makes Poland a highly cost-effective origin, especially when compared to its regional competitor, Romania, which is facing a 32.46% production deficit and whose prices are 12.22% higher YoY. Poland has solidified its position as the EU's second-largest maize exporter, and its current supply-driven price weakness presents a clear procurement opportunity.

Prioritize the US for Large-Volume Supply Based in the Americas

Global importers needing to secure large-volume contracts should continue to focus on the US as the primary procurement destination in the Americas. The fundamental driver for this strategy is the large 2025/26 crop. While the government shutdown has delayed the official October WASDE report, the last official forecast in September projected a near-record US corn production of 16.8 billion bushels on the largest harvested area since 1933. Private estimates confirm the harvest is over 90% complete, ensuring the market is well-supplied.

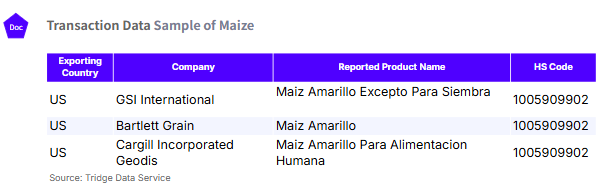

This immense supply ensures exceptional market liquidity for buyers fulfilling large tenders. While Brazil is also planting a large crop, its harvest is months away. The US, with its harvest nearly complete, offers readily available physical supply. This large supply volume has anchored US prices, making it the most reliable and stable source for immediate, large-volume procurement. This is evident in the current futures price of USD 169.45/mt, which remains highly competitive on the global stage. According to Tridge Eye data, US suppliers to consider for purchasing maize include GSI International, Bartlett Grain, and Cargill.