In W20 in the avocado landscape, some of the most relevant trends included:

- Brazil passed a Japanese audit for its Hass avocado production and secured progress toward access to Japan’s high-value market with confirmed full compliance.

- Morocco’s avocado exports nearly doubled to 110 to 120 thousand mt, but prices fell sharply due to oversupply and logistical challenges, which put pressure on established exporters.

- Kenya’s avocado season is in progress as demand grows from China and India. However, exporters face shipping delays and higher costs from Red Sea disruptions, so they adopt methods to preserve fruit quality.

- Mexico expects a record USD 4 billion in avocado exports in 2025 due to strong US demand and improved production, making avocados its third-largest agricultural export.

- South Africa’s Tzaneen region suffers from a growing crisis of organized avocado theft that causes financial losses and forces farmers to spend more on private security.

1. Weekly News

Brazil

Brazil Advances Toward Japanese Market Access Following Successful Hass Avocado Audit

Brazil hosted a Japanese technical mission in late Apr-25 to audit its Hass avocado production. The visit was part of efforts to finalize access to the Japanese market. The inspection was conducted in São Paulo and focused on key areas such as traceability, harvest control, training, and transportation. It concluded without any issues or violations, confirming Brazil's compliance with Japan's strict standards. This marks a strategic advancement in Brazil’s market diversification efforts and reinforces its reputation as a reliable supplier of fresh avocados. While Japan is a niche market with relatively low volumes, its high-value demand presents a promising opportunity for increased profitability among Brazilian exporters.

Morocco

Morocco’s Avocado Exports Surge to Record Levels Despite Price Decline

Morocco exported over 100 thousand metric tons (mt) of avocados in both the 2022/23 and 2023/24 seasons. For the 2024/25 season, estimates range from 110 thousand to 120 thousand mt, marking a continued upward trend driven by favorable weather that supported high-quality yields. However, the supply surge triggered a steep decline in average prices, falling 30 to 35% overall and by 50% in Dec-24 alone, as intense competition among exporters, including newer players with limited resources, drove prices down further. While growers generally maintained acceptable margins, long-established exporters struggled with financial strain due to fixed operational costs. Inconsistent logistical capacity also disrupted export flow, adding to price volatility. The industry must prioritize investment in modern machinery, expanded packing and cold-storage infrastructure, and more coordinated, strategic export planning to ensure sustainable growth and protect market value.

Kenya

Kenya’s Avocado Season Begins Despite Growing Global Demand and Logistical Hurdles

Kenya’s avocado season runs from April to October, with some harvests extending into December. Growing global demand, particularly from China and India, has led to projections that the market could double by 2030. Kenyan exporters mainly serve Europe, followed by the United Arab Emirates (UAE), India, and other Asian destinations, though the United States (US) market remains largely untapped for some producers. Consumer preferences vary, with larger avocado sizes popular among families and the hospitality industry. However, exporters are facing logistical hurdles, especially due to Red Sea disruptions that have increased shipping times and costs, leading to the adoption of ethylene extractors to delay ripening and maintain fruit quality during transit.

Mexico

Mexico Forecasts Record Avocado Export Revenues in 2025 Driven by Rising Global Demand

Mexico is expected to reach a record USD 4 billion in avocado exports in 2025, following a USD 3.78 billion export value in 2024. This 20.1% year-on-year (YoY) increase is due to a strong US demand, which accounts for over 80% of Mexico’s avocado exports. Export volumes are projected to rise 5% year-on-year (YoY) to 1.34 million metric tons (mmt), despite a 9% dip in 2024 due to harvest fluctuations and high logistics costs. Mexico still supplied approximately 88% of all avocados imported by the US, with peak shipments between December and February. Hass avocados continue to dominate exports for their superior quality and shelf life, making avocados Mexico’s third-largest agricultural export after beer and tequila. Locally, off-season demand is met with limited imports from Peru and Colombia. Production is forecasted to grow 3% in 2025 to 2.75 mmt, supported by favorable weather, improved farming practices, and environmental certification, with 256.5 thousand hectares (ha) of cultivation mainly in Michoacán and Jalisco.

New Zealand

New Zealand Expands Avocado Export Strategy to Boost Global Reach

New Zealand plans to diversify its avocado export markets in the 2025/26 season to reduce dependence on Australia by targeting North America and key Asian countries like South Korea, Japan, and Thailand. Currently, 50 to 60% of the avocado crop is exported while the rest is consumed locally. This revised strategy aims to align supply more closely with market demand, improve grower returns, and reduce pressure on the local market during peak periods. Although the upcoming crop is projected at 6.2 million trays, down from 7.2 million last season, improved fruit quality and pack-out rates are expected to maintain stable export volumes. New Zealand’s pest-free status, which grants access to over 80 countries, gives the industry a competitive advantage despite recent challenges from cyclones and weather disruptions. These events have affected fruit quality and local prices. Most avocados come from small-scale growers in the Bay of Plenty and Northland, with ongoing efforts in orchard management, such as nutrient balancing, pruning, and disease control, supporting sustainable production and export growth.

Peru

Peru Targets Growth in Avocado Exports Within Global Market Shifts

Peru is expecting higher avocado exports in the 2025 season, driven primarily by an increase in the number of producers rather than a significant rise in overall production. The avocado campaign runs from W4 to W36, peaking on Mar-25, with export markets increasingly diversified. In the early part of the season, Europe accounted for 60% of shipments and Asia 30%, while later shipments shifted to 45% Europe, 30% Asia, and 25% to the US, the United Kingdom (UK), and Latin America. Notably, US exports surged to 175 containers by W18, up from W38 2024r, despite a 10% tariff. Peru’s competitiveness is supported by high Mexican prices and improved logistics, especially the new port of Chancay, which has cut transit time to China from over 30 days to 23. Although Europe faces ongoing logistics challenges and high freight costs, shipments to Asia remain cost-effective, with stable pricing in markets like Japan providing predictability. Amid rising global demand, particularly in China, the US, and parts of Europe, Peru is also exploring value-added products like avocado oil from discarded fruit, reflecting a broader strategy to expand and strengthen its avocado export industry.

South Africa

Avocado Theft Crisis Escalates in South Africa’s Tzaneen Region

In South Africa’s Tzaneen area, avocado farmers are increasingly facing organized fruit theft, which has grown from a seasonal problem into a persistent issue throughout the Mopani region. Often involving seasonal workers and truck drivers, criminal syndicates are stealing avocados, even before official harvests, leading to significant financial losses and damage that renders the fruit unsellable. Since about 90% of thefts go unreported due to difficulty in proving cases once stolen fruit is mixed with legitimate stock, the problem remains widespread and hard to control. This criminal activity has also spread to crops like citrus and valuable farm infrastructure, such as irrigation cables. Despite the high cost, private security is vital for farmers, while consumers are advised to be cautious when purchasing avocados from informal vendors, as stolen fruit is often bruised, overripe, and missing stems, which increases the risk of spoilage.

2. Weekly Pricing

Weekly Avocado Pricing Important Exporters (USD/kg)

Yearly Change in Avocado Pricing Important Exporters (W20 2024 to W20 2025)

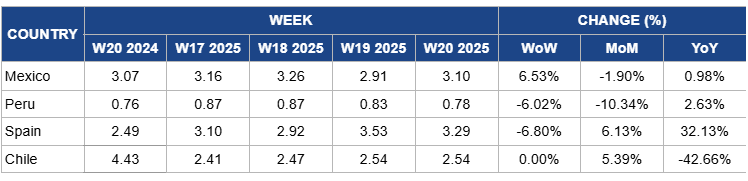

Mexico

In W20, Mexico's avocado prices increased by 6.53% week-on-week (WoW) to USD 3.10 per kilogram (kg), with a 0.98% YoY rise. This uptick is due to a 25% reduction in shipments to the US than last year, leading to tighter supplies in the primary export market. However, prices experienced a 1.90% month-on-month (MoM) decrease as production ramped up, with Mexico's 2025 avocado production forecasted to reach 2.75 mmt, a 3% YoY increase over 2024, driven by strong export demand and favorable growing conditions. Additionally, increased market presence from alternative sources like California and Colombia helped ease supply constraints, exerting downward pressure on prices.

Peru

Avocado prices in Peru decreased by 6.02% WoW to USD 0.78/kg in W20, with a 10.34% MoM decline, due to increased harvest volumes from coastal regions like La Libertad and Ica, which boosted local supply and exerted downward pressure on prices. However, there is a 2.63% YoY increase, reflecting a gradual recovery from last year’s weather-related setbacks. The previous year’s unusually cold conditions disrupted the biological cycle of avocado trees, leading to reduced productivity and smaller fruit sizes. This year, improved weather and better fruit development have supported a slight price rebound compared to the previous year. Although concerns over a potential La Niña event in the upcoming season may still pose risks to future production.

Spain

In W20, avocado prices in Spain dropped by 6.80% WoW to USD 3.29/kg, reflecting a 10.34% MoM decrease. This decline is due to increased imports from third countries, notably Morocco, which have exerted downward pressure on local prices. Additionally, the market is experiencing an oversupply due to a production increase of over 15 to 20% compared to the 2023/24 season. However, there is a 2.63% YoY price increase, reflecting the lingering effects of the previous year's unusually cold weather that disrupted the biological cycle of avocado trees, leading to reduced productivity and smaller fruit sizes. Despite a projected recovery in production for 2025, concerns over potential weather anomalies may limit growth, keeping prices relatively low in the short term.

Chile

Chilean avocado prices remained steady WoW at USD 2.54/kg in W20, with a 5.39% MoM increase due to strong demand in key export markets like Europe and China, where Chilean avocados have gained market share due to their quality and consistent supply. However, YoY prices dropped by 42.66% due to a significant 33% increase in local production for the 2024/25 season, leading to an oversupply that has exerted downward pressure on prices.

3. Actionable Recommendations

Expand Market Reach and Invest in Value-Added Avocado Products

Avocado producers in leading countries like Peru, Mexico, and Kenya should focus on diversifying export markets beyond traditional destinations by targeting growing demand in Asia, the US, and Latin America. Improving logistics, such as faster port access and better cold chain management, can help maintain fruit quality and reduce transit times, as seen with Peru’s Chancay port cutting shipping time to China. Producers should also invest in developing value-added products like avocado oil or dried avocado snacks to increase profitability and reduce waste from lower-grade fruit, enhancing overall competitiveness in the global market.

Optimize Logistics and Explore New Markets to Maximize Avocado Exports

Avocado producers and exporters in Kenya and other key growing regions should invest in advanced post-harvest technologies like ethylene extractors to extend shelf life and maintain fruit quality amid shipping delays. Expanding into underutilized markets such as the US and strong demand in Europe, India, and China will help diversify sales channels. For example, targeting larger-sized avocados favored by families and hospitality sectors can boost premium sales. Strengthening cold chain logistics and exploring alternative shipping routes can mitigate disruptions like those in the Red Sea, ensuring timely deliveries and competitive pricing.

Enhance Post-Harvest Handling and Market Diversification for Avocado Exporters

Avocado producers and exporters should prioritize investing in advanced post-harvest technologies like ethylene extractors and improved cold chain systems to maintain fruit quality during longer shipments caused by logistics disruptions, such as those in the Red Sea. Expanding into untapped markets like the US, while tailoring supply to meet consumer demand for larger fruit favored by families and the hospitality sector, can increase revenue streams. For example, exporters from Kenya and other producing countries can combine better ripening control with targeted marketing strategies in Asia and the Middle East to strengthen global market presence.

Sources: Tridge, Abrafrutas, Citizen, ECOMAC, Eleconomista, MAVA, SunLive, The Independant, USDA