.jpg)

In W20 in the soybean landscape, some of the most relevant trends included:

- Brazil’s 2024/25 soybean harvest is nearly complete at 97.8%, surpassing the previous year’s 95.6%, with strong yields. However, regional differences in export performance emerged, notably a decline in Paraná due to weaker demand from China.

- China sharply increased soybean imports from Brazil in early 2025, while US exports to China fell significantly amid ongoing trade tensions. Ukraine raised its 2025 soybean production and export forecasts despite some farmers shifting to other crops.

- Regarding prices, weekly soybean prices rose in Brazil due to expected acreage expansion and strong demand. In contrast, US prices declined due to ample supply and weak exports. Argentina and Uruguay experienced moderate price changes influenced by local harvest progress and global market pressures.

1. Weekly News

Brazil

Brazil’s 2024/25 Soybean Harvest Nears Completion with Above-Average Progress and Strong Yields

Brazil has nearly completed its 2024/25 soybean harvest in W20, reaping approximately 97.8% of the total cultivated area. This pace surpasses 2024’s rate of 95.6% and the five-year average of 96.6%, reflecting a strong and efficient harvest season. Farmers have reported excellent average yields nationwide, with only a few areas left to harvest. In Rio Grande do Sul, growers have already harvested about 90% of the planted area, totaling 6.18 million hectares (ha) out of the 6.87 million ha cultivated. This marks a notable improvement over the 75% completion rate during the same period in 2024. Moreover, farmers are almost finished harvesting in the Midwest and Southeast regions, with only residual areas remaining.

Brazil’s Q1-25 Soy Complex Exports Increased Slightly Despite Paraná Decline

In Q1-25, Brazil's soy complex, which includes soybeans, bran, oil, and related derivatives recorded a modest year-on-year (YoY) export increase, reaching 27.87 million metric tons (mmt) compared to 27.42 mmt in Q1-24. However, this overall growth masked regional disparities. The state of Paraná, Brazil's second-largest soybean producer, experienced a notable 18.7% YoY decline in exports, dropping to 3.37 mmt. The decline was due to weaker demand from China, a key trading partner. Despite the setback in Paraná, market analysts are optimistic about the second half of 2025 (H2-25). They expect a more favorable external environment, particularly if trade tensions between China and the United States (US) ease. A resolution in the tariff dispute could shift Chinese buying interest back toward Brazilian soy products, potentially reversing the export decline and leading to stronger performance later in the year.

China

China Boosts Soybean Imports from Brazil to Record Levels in Mar-25 to Apr-25

China has sharply increased its soybean imports from South America, especially Brazil. Between Mar-25 and Apr-25, Brazil shipped a record 21.9 mmt of soybeans to China, 3.1 mmt more than during the same period last year. Analysts expect China to maintain high import volumes in May-25 and Jun-25 from Brazil. In contrast, Argentina delivered only 70 thousand metric tons (mt) of soybeans to China in Apr-25, down from 165 thousand mt in Apr-24. However, a seasonal increase in shipments is expected soon. US soybean exports to China dropped significantly from Jan-25 to Apr-25. The US shipped 5.8 mmt, down from 9.4 mmt a year earlier. In Apr-25 alone, the US delivered just 550 thousand mt. If trade tensions between the two nations persist, these volumes may decline further.

Ukraine

Ukraine’s 2025 Soybean Harvest and Export Forecast Revised Upward

Ukraine’s 2025 soybean harvest is forecast at 6.11 mmt in May-25, up from 5.90 mmt in Apr-25, reflecting expectations of higher yields. As a result, the country’s soybean export forecast for the 2025/26 marketing year (MY) has also been revised upward to 3.69 mmt, compared to the earlier projection of 3.56 mmt. This upward revision comes despite a possible decline in sown area, as some farmers are shifting toward more profitable crops such as corn and sunflower. The global drop in soybean prices has prompted many Ukrainian producers to reassess their planting strategies. However, strong demand from domestic processors facing a shortage of sunflower seeds could sustain interest in soybean cultivation. As of May 9, Ukrainian farmers had sown 1.3 million ha of soybeans, representing 55.9% of the planned area.

2. Weekly Pricing

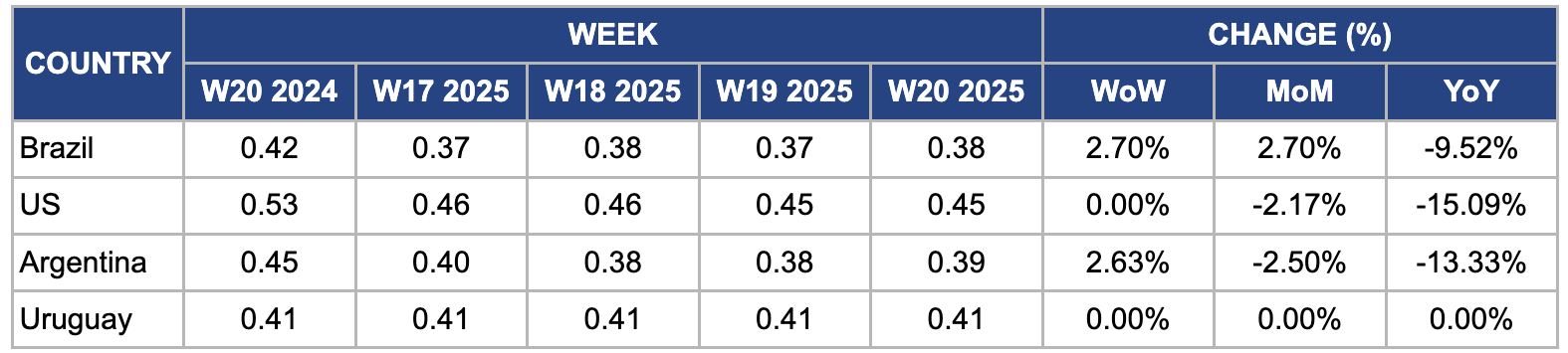

Weekly Soybean Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Pricing Important Exporters (W20 2024 to W20 2025)

Brazil

In W20, Brazil’s soybean prices rose 2.7% week-on-week (WoW) and month-on-month (MoM) to USD 0.38 per kilogram (kg), fueled by expectations that farmers will expand soybean acreage by about 500 thousand ha, in the 2025/26 season, marking the 19th consecutive year of growth. This expansion is expected mainly in the central-western and northeastern regions, which benefit from favorable growing conditions. While China remains the key market driving demand, the pace of acreage growth may slow compared to previous years due to changing market dynamics and environmental factors. Nonetheless, strong export demand and continued planting expansion support the recent price increase.

United States

In W20, US soybean prices remained steady WoW but fell 2.17% MoM to USD 0.45/kg. The accelerated planting progress in the US and favorable weather added downward pressure on prices. Weak export demand, especially from China, contributed to the decline amid renewed concerns about potential trade tensions following recent US tariff announcements. Moreover, large soybean supplies from Brazil, currently the world’s top exporter, kept US prices under pressure. Brazil’s record 2024/25 harvest and competitive pricing made its soybeans more attractive globally. On the domestic front, sluggish farmer sales and planting season activity limited market movement, reinforcing the downward pressure on prices.

Argentina

In W20, Argentina’s soybean prices increased by 2.63% WoW, rising to USD 0.39/kg from USD 0.38/kg, buoyed by steady progress in the ongoing harvest season. The Buenos Aires Grain Exchange (BAGE) reported that the soybean harvest had reached 64.9% completion, up from the previous week’s figures, indicating a steady pace of fieldwork despite some regional challenges. Yields also improved slightly to 32 bags per ha, marking an 8% increase compared to the last crop cycle. However, this yield level remains 5% below the five-year average, suggesting that while the crop is recovering, it has not yet fully returned to its typical productivity levels. Factors such as uneven rainfall distribution and soil conditions in certain growing areas contributed to this gap.

Uruguay

In W20, Uruguay’s soybean prices held steady WoW at USD 0.41/kg, reflecting a balance between a strong recovery in domestic production and ongoing pressure from subdued global market conditions. After the severe drought in 2023 that cut Uruguay’s soybean output drastically to around 700 thousand mt, the 2024/25 harvest bounced back significantly to an estimated 3.1 mmt. This rebound was driven by favorable weather and improved yields, bringing production closer to the five-year average. However, despite this recovery, Uruguay’s soybean prices remain pressured due to an oversupplied international market, fueled by record harvests across South America, especially in Brazil.

3. Actionable Recommendations

Encourage Diversification of Export Markets for Brazilian Soybeans

Brazil’s soybean exports are heavily concentrated toward China, which makes the market vulnerable to shifts in Chinese demand due to geopolitical tensions or tariff disputes. Brazilian exporters and government agencies should proactively explore and develop alternative markets. This involves conducting market research to identify emerging demand in Southeast Asia (beyond China), Europe, the Middle East, and Africa. Trade missions, participation in international agricultural fairs, and bilateral trade agreements can open doors to new buyers. Moreover, promoting Brazilian soybeans through marketing campaigns highlighting quality and sustainability credentials can help attract premium buyers. Diversification will reduce dependence on a single market, stabilize export revenues, and create buffers against sudden demand shocks, improving long-term resilience.

Support Ukrainian Farmers with Yield-Enhancing Technologies

Ukraine’s soybean production prospects have improved due to expected higher yields despite some reduction in planted areas. To capitalize on this trend and sustain growth, agricultural stakeholders should invest in providing Ukrainian farmers with access to advanced agronomic technologies and practices. This could include subsidizing high-yield and disease-resistant seed varieties, facilitating precision agriculture tools like soil sensors and GPS-guided equipment, and offering training programs on best crop management techniques. Public-private partnerships with agritech companies can help deliver these innovations at scale. Moreover, improving access to quality inputs such as fertilizers and crop protection products will boost productivity. By enhancing yields, Ukrainian farmers can maintain competitiveness even in a volatile global price environment and shift toward more profitable crop mixes with confidence.

Enhance US Market Competitiveness Through Supply Chain Efficiency

US producers and exporters should optimize the supply chain to reduce costs and improve efficiency. They can invest in modernizing port infrastructure, streamline logistics and transportation, and adopt digital tracking systems to minimize delays and spoilage. They can facilitate faster delivery and respond better to market demands by improving coordination among farmers, cooperatives, and exporters. Promoting non-genetically modified organisms (GMO), organic, or specialty soy products can help differentiate US soybeans and capture niche markets willing to pay premiums. Staying closely informed about trade negotiations and tariffs will allow them to anticipate demand changes and adjust export strategies, strengthening the US's position in the global soybean trade.

Sources: Tridge, Agrolink, Canal Rural, Grain Trade, UkrAgroConsult