In W22 in the tomato landscape, some of the most relevant trends included:

- Morocco exported 621 thousand mt of tomatoes in 2024/25, earning over USD 1.5 billion and surpassing Spain as the world’s third-largest exporter. However, producers face mounting pressure from labor shortages, water scarcity, and rising costs, with government subsidies covering less than 10% of production costs.

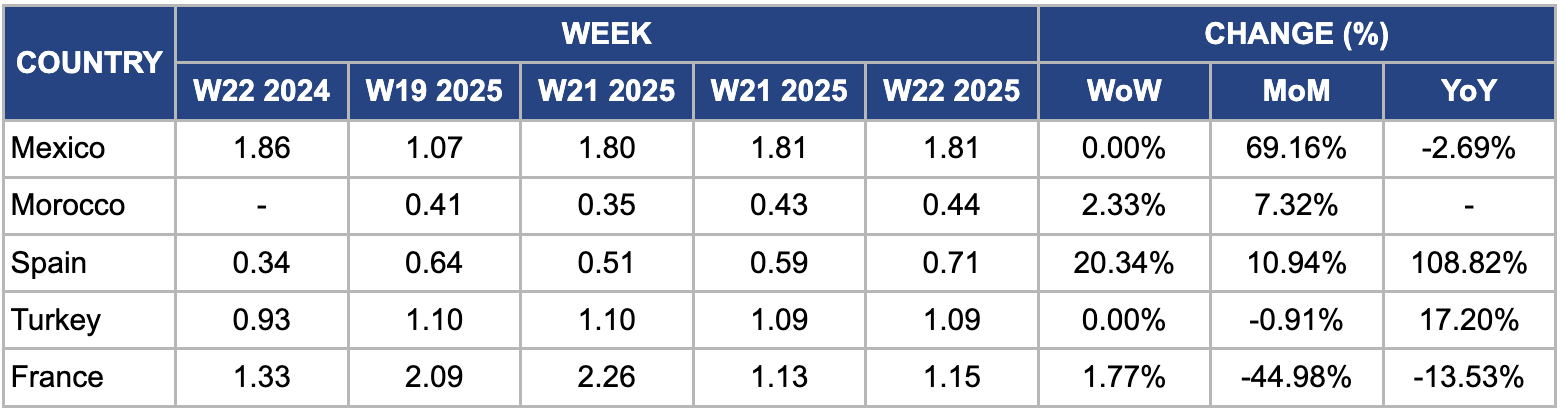

- In Nepal, wholesale tomato prices jumped 85.71% YoY, with retail prices reaching up to USD 1.12/kg, following a 36 to 44% drop in supply volumes. Spain experienced a 20.34% WoW price increase due to planting delays and a projected 22.5% YoY production drop.

- Mexico’s prices stayed flat WoW but surged 69.16% MoM amid looming 17.09% US anti-dumping tariffs, reducing export revenues to USD 859 million.

- Türkiye’s prices remained relatively stable at USD 1.09/kg, down just 0.91% MoM, supported by favorable weather and easing domestic demand.

1. Weekly News

Morocco

Morocco’s Tomato Sector Faces Labor and Water Crisis Amid Record Exports in 2024/25

Morocco’s tomato industry experienced mounting pressure due to labor shortages and prolonged drought, particularly in the arid Souss-Massa region. Many workers are shifting to the more profitable red fruit sector, retraining for blueberry and raspberry cultivation, intensifying labor scarcity during critical harvest periods. Sub-Saharan migrants in Agadir are helping to partially fill this labor gap. Despite government support programs offering subsidies of USD 4,000 to 7,000 per hectare (ha), these cover less than 10% of production costs. Water scarcity further exacerbates the strain on growers, yet exports remain a financial lifeline, enabling producers to stay afloat amid weak local market conditions. In the 2024/25 season, Morocco exported 621 thousand metric tons (mt) of tomatoes, ranking third globally and earning over USD 1.5 billion. European markets absorb most of the volume, helping Morocco surpass Spain in global export rankings.

Nepal

Tomato Prices Surge in Kathmandu Due to Supply Shortage

In W22, limited supply drove a sharp surge in tomato prices across Kathmandu Valley’s wholesale market. Nepali tomatoes jumped 85.71% year-on-year (YoY) to USD 0.49 per kilogram (kg), while Indian tomatoes rose 9.01% YoY to USD 0.38/kg. Smaller local tomatoes climbed 56.74% YoY, reaching USD 0.26/kg. Retailers raised prices even more steeply, selling large tomatoes for up to USD 1.12/kg and smaller ones at USD 0.74/kg, compared to the earlier range of USD 0.38 to 0.45/kg. Weather disruptions limited supply chains, and this imbalance between supply and demand primarily drove the price hikes.

At Kalimati market, suppliers reduced large tomato deliveries by 36.17%, bringing in just 15 mt monthly. Small tomato volumes also dropped 44.22% to 56 mt. However, current retail trends show a price correction from previous peaks of USD 0.60 to 0.67/kg, as the arrival of more seasonal vegetables has helped stabilize overall supply.

New Zealand

New Zealand to Review Biosecurity Measures as Australia Shifts Strategy on Tomato Virus

New Zealand’s Ministry for Primary Industries (MPI) will review its biosecurity controls following Australia’s decision to stop eradicating the Tomato brown rugose fruit virus (ToBRFV) and shift to management, as authorities there deemed eradication technically unfeasible. The virus, which can deform fruit and cut crop yields by up to 70%, poses no risk to humans but has spread in South Australia and Victoria since Aug-24. In response, New Zealand swiftly implemented border controls, including a ban on all Australian tomato imports and mandatory virus testing for tomato and capsicum seeds from Australia. MPI’s deputy director-general confirmed these measures have kept the virus out of New Zealand. The current protections will remain in place as MPI evaluates any potential adjustments.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W22 2024 to W22 2025)

Mexico

In W22, Mexican tomato prices held steady week-on-week (WoW) at USD 1.81/kg but jumped 69.16% month-on-month (MoM), remaining 2.69% below last year’s USD 1.86/kg. This volatility stems largely from trade uncertainties, notably the United States’ (US) decision to impose a 17.09% anti-dumping duty on Mexican tomatoes starting July 14, 2025. The looming tariff has triggered a 3.2% decline in overall Mexican agricultural exports and a 7.8% drop in tomato export revenues, down to USD 859 million in early 2025. With over half of Mexico’s tomato output destined for the US, which relies on Mexican supply for nearly 70% of its fresh tomatoes, these trade measures threaten price stability and regional economies like Baja California, which are deeply reliant on tomato exports.

Morocco

In W22, Morocco’s tomato prices increased 2.33% WoW and 7.32% MoM to USD 0.44/kg, up from USD 0.43/kg in W21. This rise was due to supply constraints and strong export demand. Prolonged drought conditions and high temperatures in key producing regions like Souss-Massa led to a 15% drop in production compared to 2024, reducing domestic availability. Furthermore, ongoing labor shortages, especially during peak harvesting periods, further slowed harvesting operations and limited market supply. At the same time, strong export demand from European markets supported elevated price levels as producers prioritized more lucrative overseas shipments.

Spain

In W22, Spain's tomato prices rose sharply by 20.34% WoW to USD 0.71/kg, driven by planting delays caused by wet spring conditions. According to the World Processing Tomato Council (WPTC), adverse weather, including cold spells and heavy rains in key regions like Andalusia and Extremadura, significantly disrupted planting schedules and reduced yields, prompting a projected 22.5% YoY decline in production from 3.1 million metric tons (mmt) in 2024 to 2.4 mmt in 2025. Alongside these setbacks, Spain is facing growing pressure from lower-cost competitors like Morocco and Türkiye, which are steadily eroding its market share.

Türkiye

In W22, Türkiye's tomato prices held steady WoW but edged down by 0.91% MoM to USD 1.09/kg, as post-peak domestic demand eased and early-season harvests gradually boosted supply. Favorable weather in key growing areas like Antalya and Mersin supported consistent crop development, helping stabilize market conditions. Despite the modest price decline, levels remained relatively high compared to W22 2024, mainly due to persistent challenges such as elevated input costs and logistical inefficiencies affecting supply chain operations.

France

In W22, France’s tomato prices rose slightly by 1.77% WoW to USD 1.15/kg, primarily due to constrained domestic supply amid seasonal and structural challenges. A cooler-than-usual spring delayed greenhouse production by 7 to 10 days in key growing regions such as Brittany and Provence, reducing early-season availability. Furthermore, the sector continued to face persistent labor shortages, particularly for harvesting and handling tasks, which limited the volume of tomatoes reaching the market. Meanwhile, demand remained firm from retail and food service outlets as the summer approached, tightening the supply-demand balance and supporting the moderate price increase observed in W22.

3. Actionable Recommendations

Expand Labor Incentives and Mechanization in Morocco’s Tomato Sector to Address Labor Shortages

As Morocco’s tomato industry faces acute labor shortages, especially in Souss-Massa, due to a shift toward the more profitable red fruit sector, producers and agribusiness stakeholders should invest in targeted labor retention strategies and mechanization. Practical steps include offering productivity-based bonuses, temporary housing, and transport support to attract and retain local and Sub-Saharan migrant workers. Moreover, co-investing in semi-mechanized harvesting tools (e.g., cart-mounted conveyors or automated sorters) for large-scale farms can reduce dependency on manual labor during peak harvest windows. Expanding partnerships with vocational training centers to fast-track skill development for tomato cultivation would further ensure a reliable workforce.

Introduce Dynamic Pricing Support and Forward Contracts for Nepali Tomato Growers

Nepal’s agricultural institutions and market facilitators should introduce forward contract models and dynamic pricing tools. Establishing digital platforms that allow growers to pre-sell tomatoes at agreed prices to wholesalers and retailers can hedge against losses during supply shortages or delays. For example, cooperatives in Kathmandu Valley can pilot mobile-based contracts supported by government-backed price stabilization funds to provide baseline income guarantees. Real-time supply chain monitoring and seasonal forecasting tools could help buyers and sellers align expectations and reduce retail price spikes. This will enhance market transparency, improve income predictability, and prevent consumer price shocks.

Boost Greenhouse Tomato Investment in Spain to Mitigate Climate-Induced Field Production Losses

Spanish tomato growers, particularly in Andalusia and Extremadura, should be encouraged to transition more acreage into greenhouse production. Targeted government grants, low-interest loans, and tax incentives can support small and mid-sized farmers in adopting protected cultivation techniques. Moreover, climate-smart infrastructure like drip irrigation, temperature-controlled tunnels, and vertical farming systems can shield crops from weather extremes and extend growing seasons. For example, regional agricultural chambers can run joint pilot programs with agritech firms to demonstrate yield stability and higher returns under greenhouse systems. These investments would reduce Spain’s dependence on-field production, stabilize export volumes, and reclaim lost market share from rising competitors like Morocco and Türkiye.

Sources: Tridge, Fresh Plaza, Krishak Jagat, RNZ