In W24 in the grape landscape, some of the most relevant trends included:

- In Chile, the construction of a new phytosanitary inspection center in Coquimbo will support table grape exports to the US under the 2024 Systems Approach. This development is expected to boost quality, ease port congestion, and aid small producers.

- The 2025 grape harvest has started in Yanqul, Oman. The Ministry of Agriculture is supporting farmers with irrigation, pest control, and improved seedlings to enhance quality and sustainability.

- Table grape exports from Peru rose 31% YoY in the 2024/25 season, reaching over 81.4 million boxes. This growth was driven by strong production from Ica and Piura and led by the White Seedless, Red Seedless, and Sweet Globe varieties.

- In Spain, the 2025 table grape campaign will begin around July 5 in Murcia, delayed by 10 days due to delayed spring weather. However, early varieties remain healthy, and national coordination is underway to address phytosanitary and sustainability challenges.

1. Weekly News

Chile

Chile Expands Grape Export Capacity with New Phytosanitary Inspection Center

Chile is strengthening its table grape export infrastructure with the construction of a new phytosanitary inspection center in the Coquimbo region, supported by the Agricultural and Livestock Service and the Ministry of Agriculture. This facility will enable compliance with the Systems Approach protocol approved in 2024, following two decades of negotiations. The protocol allows for direct export to the United States (US) without methyl bromide fumigation, improving both product quality and market competitiveness. With a capacity of up to 11 million boxes annually, the center will ease congestion at the Pan de Azúcar site and improve logistics by being strategically located near the port of Coquimbo. The initiative is also expected to support small producers, generate employment, and stimulate regional development across the grape supply chain.

Oman

Oman’s Grape Harvest Season Begins in Yanqul

The grape harvest season has begun in Yanqul, A'Dhahirah Governorate in Oman, where around 2.6 thousand grape trees are cultivated across 13 acres, producing a mix of local and imported varieties valued for their flavor and quality in traditional markets. The Ministry of Agriculture, Fisheries, and Water Resources is actively supporting farmers by providing technical guidance, modern irrigation solutions, pest control measures, and improved seedlings to enhance yields and sustainability. These efforts not only promote efficient water use and income growth but also help preserve Oman’s agricultural heritage. The diversity of grape varieties, including local black and white grapes and Taifi, American, and Turkish types, enriches the local market and reflects the country’s ongoing commitment to improving agricultural resilience.

Peru

Peru's Table Grape Exports Surge 31% YoY in 2024/25 Season

Peru’s 2024/25 table grape season recorded a 31% year-on-year (YoY) export increase, with over 81.4 million 8.2-kilogram (kg) boxes shipped between W34 2024 and W10 2025. This growth was driven by increased production from Ica and Piura, which contributed 49% and 36% of exports, respectively. Southern regions, including Arequipa, Moquegua, and Lima, accounted for 52.8% of shipments, while Northern regions accounted for 47.2%. Among grape types, White Seedless led with 40% growth, followed by Red Seedless (32%), Black Seedless (22%), and Red Globe (6%). The US remained the primary destination, with a 46% increase in exports, while shipments to Europe rose by 50%, offsetting a 35% decline in Asian markets. Peru, which now exports more than 58 grape varieties, highlighted Sweet Globe, Autumn Crisp, and Red Globe as top performers in this successful campaign.

Spain

Spain Prepares for Delayed but Stable 2025 Table Grape Campaign

Spain’s 2025 table grape campaign is expected to begin around July 5, 2025, in the Murcia region. This is ten days later than usual due to delayed spring conditions. However, early grape varieties show strong development, with no frost or hail damage due to effective protective measures. With a national production forecast of 320 thousand metric tons (mt), Spain remains the European Union’s (EU) second-largest producer after Italy. In 2024, the country exported 167.2 thousand mt worth USD 518 million (EUR 448 million), led by Murcia, the Valencian Community, Catalonia, and Andalusia. During a recent interregional meeting with France, Italy, and Portugal, producers discussed the limited availability of authorized phytosanitary products and committed to joint studies to sustain treatment options. The sector anticipates a stable season and is working to improve EU-wide coordination for long-term sustainability and competitiveness.

South Africa

South Africa Achieves Record Table Grape Exports in 2024/25 Season

South Africa’s 2024/25 table grape season concluded with a record 77.8 million cartons exported, a 5% YoY increase, driven by strong international demand and the country’s reputation for quality. The EU and United Kingdom (UK) remained dominant markets, accounting for 58% and 18% of exports respectively, while shipments to North America rose by 25%, including 3% of total volumes to the US, reflecting growing interest in South Africa’s counter-seasonal supply. Despite these achievements, the industry faces challenges such as higher tariffs compared to competitors like Peru and Chile, which could affect future competitiveness. To address this, South Africa is focusing on trade negotiations and market diversification, although access to new markets remains a slow process. In 2024, global table grape exports generated USD 730 million in revenue and contributed over USD 820 million to the national Gross Domestic Product (GDP).

2. Weekly Pricing

Weekly Grape Pricing Important Exporters (USD/kg)

Yearly Change in Grape Pricing Important Exporters (W24 2024 to W24 2025)

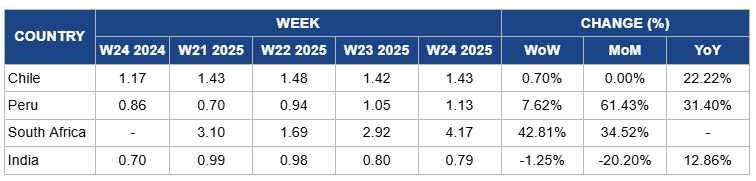

Chile

Chile’s grape prices increased slightly by 0.70% week-on-week (WoW) to USD 1.43/kg in W24 and held steady month-on-month (MoM), while showing a strong 22.22% YoY gain. The modest weekly and monthly uptick reflects sustained supply from stable harvests in regions like Valparaíso and O’Higgins. Meanwhile, the substantial YoY increase is driven by tighter overall export volumes (a slight 1% dip from prior projections), and improved quality via premium varieties and Systems Approach certification, boosting competitiveness in key markets like the US and Europe.

Peru

In W24, Peru's grape prices rose 7.62% WoW to USD 1.13/kg, building on significant gains of 61.43% MoM and 31.40% YoY. The weekly price increase reflects tightening local supply as the main export season winds down and volumes from late-season regions like Ica and Piura begin to decline. The strong MoM and YoY gains are supported by a record-breaking export campaign, with over 562 thousand tons shipped, a 7.4% increase, boosted by expanded market access in Japan and China and sustained demand from the US and Europe.

South Africa

South Africa’s grape prices surged sharply by 42.81% WoW to USD 4.17/kg in W24 and climbed 34.52% MoM as the harvest season wound down and high-quality table grapes, particularly white seedless varieties, became scarce in local markets. This shortage coincided with a record-breaking export campaign, 77.8 million cartons shipped, driven by strong demand from Europe, the UK, and notably North America, where shipments grew by 25% YoY. Improved logistics and port efficiencies, such as enhanced throughput at Cape Town, allowed faster delivery of premium-grade fruit, keeping export supply tight and boosting domestic prices.

India

Grape prices in India dropped slightly by 1.25% WoW to USD 0.79/kg in W24, with a 20.20% MoM drop due to increased late-season arrivals from regions like Pune and Sangli, which boosted domestic supply and exerted downward pressure on prices. However, YoY prices increased by 12.86% due to a significant drop in production, estimated at around 40%, caused by unseasonal rainfall in major producing regions like Nashik earlier in the season, tightening overall supply compared to the previous year.

3. Actionable Recommendations

Strengthen Market Position Through Differentiated Branding

Grape producers should work with exporters to build strong origin-based branding that highlights product quality, sustainability, and counter-seasonal availability to offset tariff disadvantages in key markets. For example, producers in South Africa, India, and Egypt can use branded packaging, QR code traceability, and sustainability certifications to appeal to premium retail chains in the EU, UK, and North America. These efforts help justify higher prices and secure shelf space, especially when competing with lower-tariff suppliers. Differentiated branding reinforces market loyalty and cushions the impact of trade barriers.

Adopt the Systems Approach Protocol to Improve Export Efficiency

Grape producers should coordinate with exporters and packing facilities to implement the Systems Approach protocol for US-bound shipments, reducing reliance on methyl bromide fumigation. This includes investing in on-farm pest monitoring, maintaining detailed phytosanitary records, and working with certified inspection centers to meet compliance. For example, producers in Chile, Peru, and Brazil can streamline packing operations and reduce post-harvest handling costs while preserving fruit quality. This approach not only improves shelf life and market appeal but also speeds up export logistics and enhances access to premium buyers.

Sources: Tridge, Agraria, Freshplaza, Frutas De Chile, Fruit Portal, Fruit Today, Nexonoticias, Oman News, Vinetur