In W24 in the tomato landscape, some of the most relevant trends included:

- Chinese scientists have developed a genetically edited tomato variety for vertical farms, reducing space needs by 85%, shortening harvest cycles by 16%, and boosting yields by 180%, significantly improving energy and land efficiency for sustainable urban agriculture.

- Tomato prices plunged in Mysuru, India due to oversupply.

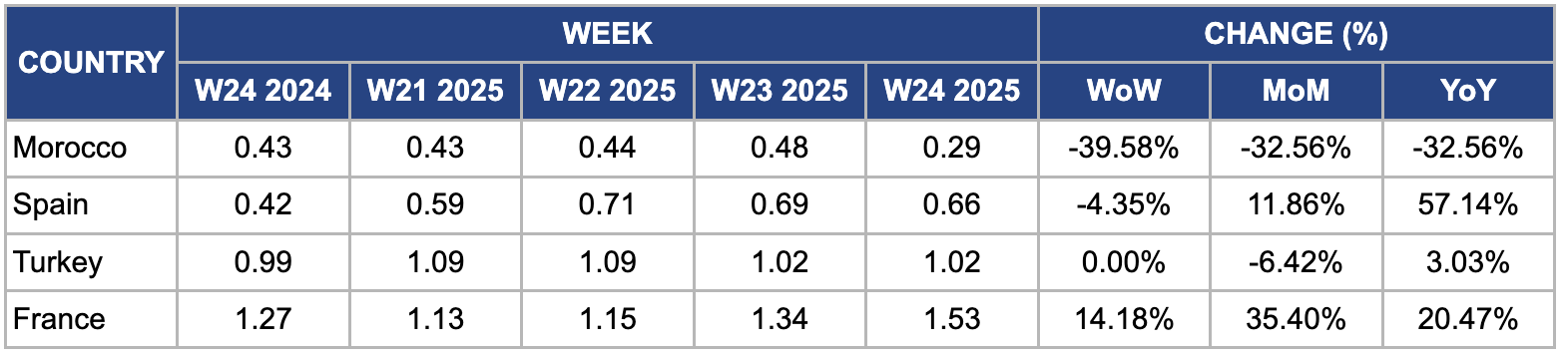

- Morocco saw a sharp WoW drop to USD 0.29/kg as peak harvests flooded markets. In contrast, prices surged in France amid delayed harvests. Türkiye maintained stable pricing at USD 1.02/kg, with Amasya’s harvest expected to fill seasonal supply gaps with 101,000 mt.

- Spain faces a long-term decline in tomato output and growing competition from lower-cost exporters like Morocco and the Netherlands.

1. Weekly News

China

China Develops High-Yield Gene-Edited Tomato for Vertical Farming

Chinese scientists have developed a genetically edited tomato "sp sp5g slga20ox1 mutant" that marks a breakthrough for sustainable urban agriculture. Engineered specifically for vertical farming systems, the new variety reduces the required cultivation space by 85%, shortens the harvest cycle by 16%, and boosts yield by 180% compared to conventional tomatoes. Moreover, the variety improves energy efficiency, offering higher productivity per square meter with lower energy inputs.

India

Tomato Price Crash in Mysuru Triggers Farmer Distress Amid Oversupply and Poor Infrastructure

A steep collapse in tomato prices has left farmers around Mysuru, India, in distress, with many resorting to dumping their harvest on roadsides and at the Agricultural Produce Market Committee (APMC) Yard as prices plunged to as low as USD 0.092 to 0.17 per kilogram (kg) due to oversupply. Despite earlier bulk purchases, prices failed to stabilize, making it uneconomical for growers to harvest or transport their produce. According to the district secretary of Raitha Mitra, cultivation costs range from USD 692.68 to 1154.54 per acre, but current market rates do not even cover labor and logistics. The lack of cold storage infrastructure for perishables like tomatoes has worsened losses, leaving farmers vulnerable to unpredictable weather and volatile market conditions.

Tomato Prices Rebound in Dharmapuri, but Farmers Still Struggle Amid Reduced Acreage and Moisture Disruptions

Tomato prices in Dharmapuri have risen due to seasonal monsoon impacts and reduced cultivation following six months of low prices caused by market oversupply. In W24, tomato prices stood at USD 0.17/kg in retail and USD 0.23/kg in wholesale markets. However, farmers reported that increasing moisture has disrupted cultivation, especially in the 4 thousand acres typically planted in Jun-25 out of the district’s annual 13 thousand-acre tomato area. As a result, many farmers have halted planting. According to a local farmer, past wholesale prices of USD 0.058 to 0.081/kg left many unable to recover their USD 230.91 per acre investment. While prices have improved, farmers say the situation remains economically challenging due to reduced yields.

Türkiye

Amasya Begins Tomato Harvest, Set to Supply 101 Thousand MT This Season

The tomato harvest has officially begun in Amasya, widely regarded as the vegetable hub of Türkiye’s Black Sea Region and nicknamed “Little Antalya” due to its prolific greenhouse production. The 2025 season’s first tomato price stood at approximately USD 0.77/kg in W24. According to Amasya’s Provincial Director of Agriculture and Forestry, the province expects to produce around 101 thousand metric tons (mt) of tomatoes across 1,250 hectares (ha) of greenhouse and open-field areas this summer. Amasya plays a critical role during Türkiye’s interim tomato season, which bridges the supply gap between the tail end of production in southern regions like Antalya and the onset of harvests in other provinces. This 45-day window positions Amasya as a key supplier, especially to the Black Sea Region, Istanbul, Ankara, and Eastern Anatolia, helping to stabilize national availability during a transitional supply period.

2. Weekly Pricing

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W24 2024 to W24 2025)

Morocco

In W24, Morocco’s tomato prices dropped sharply by 39.58% week-on-week (WoW), 32.56% month-on-month (MoM) and year-on-year (YoY) to USD 0.29/kg. This steep decline was due to a surge in domestic supply as the peak harvest season began in major production regions such as Souss-Massa and Marrakech. Favorable weather during the growing period led to higher-than-expected yields, flooding local markets with fresh produce. Moreover, reduced export volumes, especially to European markets due to stricter quality standards and increased competition from other suppliers like Türkiye and Spain, have limited external demand.

Spain

In W24, Spain’s wholesale tomato prices declined by 4.35% WoW to USD 0.66/kg from USD 0.69/kg in W23, following a modest increase in supply as planting advanced in key regions like Andalusia, supported by improved early Jun-25 weather. Despite the short-term boost, structural challenges persist. Spanish tomato production has dropped nearly 19% over the past decade, from approximately 4.89 million metric tons (mmt) in 2014 to about 3.97 mmt in 2024, signaling a long-term downtrend. Moreover, increasing import competition from lower-cost suppliers such as Morocco and the Netherlands, which now dominate Spain’s fresh tomato imports, continues exerting downward pressure on domestic prices.

Türkiye

In W24, Türkiye's tomato prices held steady WoW at USD 1.02/kg but fell 6.42% MoM as domestic demand softened after the peak season and early harvests began to increase supply. Favorable weather in major production areas like Antalya and Mersin supported stable crop development, balancing market conditions. Despite the monthly decline, prices remained 3.03% higher YoY compared to W24 2024, reflecting ongoing pressures from high input costs and logistical inefficiencies that continue to affect the supply chain.

France

In W24, France’s tomato prices jumped 14.18% WoW and 35.40% MoM to USD 1.53/kg, as delayed production met steady demand. A cooler-than-usual spring in key regions like Brittany and Provence pushed the greenhouse harvest back by seven to 10 days, limiting early-season supply. Ongoing labor shortages, particularly in harvesting and post-harvest operations, further reduced volumes entering the market. Meanwhile, demand from retailers and food service providers remained strong ahead of the summer season, tightening availability and driving the sharp price increase.

3. Actionable Recommendations

Promote High-Density Urban Varieties for Vertical Farming Expansion

Indian governments and agri-tech companies should scale up trials and commercialization of genetically edited tomatoes like China’s sp sp5g slga20ox1 mutant. Tailored for vertical farming, these varieties offer dramatic gains in yield and efficiency, making them ideal for integration into urban agriculture schemes. By providing grants or public-private incentives for rooftop or warehouse vertical farms, India could create local, controlled sources of supply less affected by monsoons, transportation disruptions, or gluts.

Establish Tomato Buffer Zones and Expand Cold Storage Infrastructure

Governments and cooperatives should invest in decentralized cold storage hubs and buffer procurement mechanisms in regions like Mysuru and Dharmapuri, where farmers suffer from price collapses due to oversupply and lack of storage. APMCs or local agri-marketing boards can facilitate price stabilization funds that buy tomatoes at pre-set minimum support prices during gluts and store them for off-season use. This can prevent wastage, smoothen supply fluctuations, and allow tomatoes to be directed toward processing when prices crash. Moreover, digital auction platforms could help growers reach buyers beyond their district or state.

Strengthen Export Readiness in Surplus Zones with Quality Compliance Support

With markets like Morocco and Spain facing export limitations due to quality and competition pressures, governments should invest in post-harvest handling, grading, and phytosanitary training programs to help producers meet European Union (EU) and Gulf market standards. Building export-certified packhouses in major production regions (e.g., Souss-Massa, Marrakech, Andalusia) and offering logistics subsidies or fast-track inspections for export shipments can help diversify market outlets and ease local oversupply. Simultaneously, exporters should be linked with retail chains and importers in under-served regions such as Eastern Europe or Sub-Saharan Africa to open new demand corridors.

Sources: Tridge, Abc, Agrolink, Kamu3, New India Express, The Hindu