W27 2025: Sugar Weekly Update

In W27 in the sugar landscape, some of the most relevant trends included:

- Brazil's wholesale sugar prices remained stable this week amid lower output and weak export momentum, with limited upside expected next week.

- Mexican sugar prices firmed slightly on the back of improved local availability, with forecasts pointing to short-term price stability.

- Pakistan’s wholesale sugar prices rose slightly but are expected to ease as duty-free imports begin arriving.

- Industry players are advised to secure flexible export contracts, expedite import clearance in Pakistan, and monitor global trends for Q4 procurement.

1. Weekly News

Brazil

Sugar Output Declines as Drought Weighs on Cane Yields

Brazil’s 2025/26 sugar production continues to feel the impact of last season’s adverse weather, with the Brazilian Sugarcane and Bioenergy Industry Association (UNICA) reporting a 14.6% year-on-year (YoY) decline in Center-South output through mid-June to 9.404 million metric tons (mmt). Companhia Nacional de Abastecimento’s (Conab) seasonal forecast now places total production at 44.1 mmt, down 3.4% YoY, as high temperatures and below-average rainfall earlier in the cycle affected cane weight and recoverable sugar content. Despite this, millers have prioritized sugar over ethanol in the production mix, offering some offset to volume losses.

Global Surplus and Asian Output Cap Price Gains

Even with Brazilian supply tightening, sugar futures markets remain under pressure from broader global surplus expectations, now pegged at 1.9 mmt for 2025/26. Additional pressure stems from strong exportable supply in India and Thailand, which are ramping up shipments. Although Intercontinental Exchange (ICE) No.11 futures gained 2.6% this week on short covering and real currency weakness, structural price upside remains constrained. Brazil’s constrained logistics, especially in ports, may further limit its ability to capture market gains in the short term.

India

Monsoon Support Improves Crop Outlook, But Surplus Keeps Prices Soft

The early arrival of the monsoon has benefitted cane planting and crop prospects, but the domestic dispatch remains tempered, with minimal off-take observed in central and southern markets. Industry groups like the Indian Sugar Mills Association (ISMA) are urging policy adjustments, specifically reverting to a 50:50 sugar-to-grain ethanol blending ratio, to help mills alleviate revenue pressure caused by low sugar prices and to enhance their financial resilience. With production rebounding toward a record ~35 mmt in 2025–26 and the monsoon delivering above-average rainfall, India is poised to generate a significant surplus, while export initiatives such as the 1 mmt liberalized exports continue to increase supply into global markets.

Mexico

Production Recovery Projected for the 2025/26 Season

Mexico’s sugar output is projected to rebound to 5.094 mmt in 2025/26, a 7% increase from the previous season’s drought-hit figures, according to the United States Department of Agriculture (USDA) June World Agricultural Supply and Demand Estimates (WASDE) report. This recovery is attributed to improved rainfall in key growing regions and better cane yield expectations. However, industry experts remain cautious, as mill profitability and grower payment delays continue to affect investment in field maintenance and varietal improvement.

Biofuel Diversification Strategy Gains Traction

In a bid to reduce reliance on raw sugar exports and hedge against volatile global prices, Mexican authorities and industry groups are advancing plans to convert sugarcane ethanol into sustainable aviation fuel (SAF). This policy shift is led by the National Committee for the Sustainable Development of Sugarcane (Conadesuca) and the Ministry of Energy. Though still in its early stages, it signals growing alignment between Mexico’s sugar sector and global decarbonization trends. While the SAF strategy won’t materially affect sugar pricing in the short term, it reflects a longer-term industrial transformation aimed at increasing value chain resilience.

Pakistan

Government Launches Import Drive to Curb Soaring Prices

Facing retail sugar prices nearing USD 0.70 per kilogram (PKR 200/kg), the Pakistani government this week waived all duties and taxes on sugar imports and approved the public-sector procurement of 500,000 metric tons (mt). The move follows weeks of pressure from consumers and wholesalers amid tight domestic supply. These emergency imports aim to ease price spikes in urban markets, particularly in Punjab and Sindh, though logistical execution will determine the timing and scale of price relief.

Competition Commission Reopens Sugar Cartel Probe

Pakistan’s Competition Commission (CCP) resumed legal proceedings against major sugar mills for alleged collusive pricing and market manipulation. Hearings are scheduled for August following a tribunal ruling that revived the case. The investigation could lead to fines or policy changes in the way sugar prices are set and monitored, reinforcing regulatory scrutiny in a historically opaque sector. Industry stakeholders now face dual pressures: import-induced market softening and heightened legal risk.

United States

Domestic Balance Sheet Stable Despite Slight Supply Dip

The USDA’s latest figures show that the United States (US) sugar supply for 2025/26 is marginally lower, now projected at 13.77 million short tons raw value (STRV), primarily due to reduced beet sugar output. Cane sugar production remains relatively steady, with imports covering the minor shortfall. Supply-use ratios remain within historical norms, keeping the domestic market fundamentally balanced. No major weather or planting disruptions have been reported.

Futures Gain Slightly as Import Flows and Global Moves Stir Markets

While physical fundamentals in the US remain stable, ICE No. 11 sugar futures rose to around US¢ 16.5 per pound (lb) this week, driven in part by international developments, including Pakistan’s import announcement and Asian export activity. Short-covering and speculative flows contributed to the price uptick, although trading volume and open interest remain subdued, indicating that the US remains more of a price taker than a driver in the global sugar market.

2. Weekly Pricing

Weekly Sugar Pricing Important Producers (USD/kg)

Yearly Change in Sugar Pricing Important Producers (W27 2024 to W27 2025)

.png)

Brazil

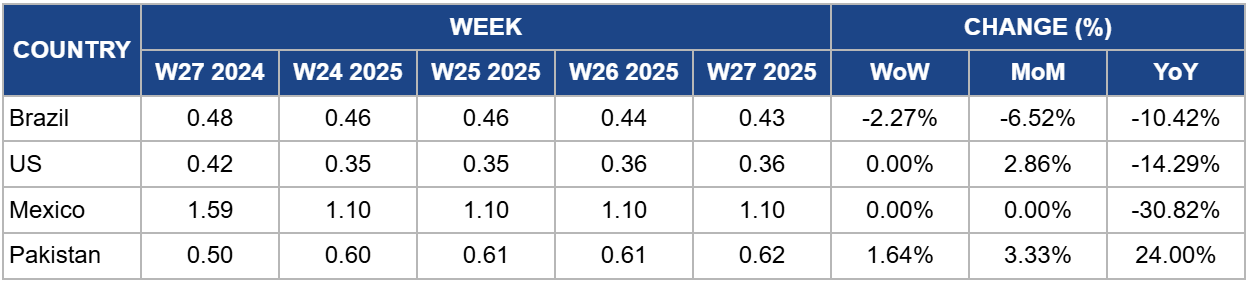

Brazilian white sugar wholesale prices averaged USD 0.43/kg, a 2.27% week-on-week (WoW) decrease. Over the past month, prices have shown slight softness due to subdued domestic demand and slow export bookings, dropping by 6.52% month-on-month (MoM). Free on Board (FOB) Very High Polarization (VHP) raw sugar at Santos ports reflected a mild negative basis in July, indicating weak local pricing power despite currency tailwinds.

Wholesale prices are expected to remain subdued unless ICE futures break decisively higher. A lack of fresh export demand and steady internal supply should keep price movement modest. However, if global fundamentals firm up, for example, tighter Indian/Thai supply or ICE strength, Brazil could see a slight upward drift in bases and domestic prices.

United States

In W27, prices remained flat at USD 0.36/kg. Domestic wholesale sugar prices have remained relatively stable throughout the month, rising by a slight 2.86%, anchored by a balanced supply-use ratio and steady beet and cane output. Physical market activity stayed low, with traders awaiting direction.

US wholesale sugar is likely to track sideways in the coming week. Without further supply shocks or import volume surprises, futures will likely remain modestly elevated. Additionally, market sentiment suggests consolidation ahead of the next WASDE and import data.

Mexico

Mexican wholesale white sugar prices remained flat at USD 1.10/kg, a trend that has persisted throughout the month. Improved cane yields and stronger local milling operations have lifted spot availability, though upstream policy signals, including SAF ethanol planning, continue to shape expectations.

Prices are expected to remain flat in W28, barring any major policy shifts or trade disruptions. Domestic supply remains sufficient, but any export tender activity or logistical delays could push prices modestly higher. Overall, stability seems likely against a backdrop of seasonal production recovery.

Pakistan

Pakistan’s wholesale sugar prices remained steady at USD 0.62/kg, slightly above USD 0.61/kg from the previous week, driven by tight domestic supply and speculative hoarding. The government’s duty-free import announcement stemmed weekly price escalations but hasn't yet relieved wholesale price stress.

Wholesale prices are expected to ease slightly in the coming week as imports start landing and regulatory pressure increases. But delays in cargo clearance or cartel resistance could sustain price plateaus. Price relief may materialize more clearly by late July once shipments begin hitting market supply chains.

3. Actionable Recommendations

Secure Flexible Export Contracts to Hedge Against Flat Domestic Prices

Given the range-bound pricing in Brazil and moderate upward movement in Mexico, exporters and cooperatives should consider signing forward or flexible export contracts with pricing tied to ICE No.11 futures. This approach allows sellers to capitalize on potential international price recovery while protecting against continued domestic price stagnation. Leveraging Brazil’s favorable currency dynamics or Mexico’s production rebound, players can boost margins by targeting niche buyers in deficit regions like North Africa and the Middle East.

Accelerate Import Clearance and Diversify Supply Channels

To contain the current price spike, Pakistani government agencies and importers should fast-track customs clearance and coordinate with port authorities to expedite public-sector sugar imports. At the same time, stakeholders should diversify sourcing, exploring origins like Thailand, Egypt, and the United Arab Emirates (UAE), to reduce dependence on limited channels. Clearer import timelines and diversified supply chains will help calm wholesale market sentiment and preempt hoarding or speculative buying.

Monitor Global Import Trends and Prepare for Q4 Coverage

Although the US sugar market is currently balanced, futures movement suggests early warning signs of external disruption, particularly from Asia and Latin America. US buyers, especially industrial users, should begin monitoring Q4 sourcing options now, locking in forward contracts if prices remain below US ¢ 17/lb. With global volatility increasing, pre-emptive procurement planning will reduce exposure to end-of-year cost spikes.

Sources: Tridge, ChiniMandi, Financial Express, The Economic Times, Reuters, Investing.com, USDA