In W3 in the tomato landscape, some of the most relevant trends included:

- Shipping 500 thousand mt annually, which is double the agreed-upon quota, Morocco surpassed Spain as the top tomato exporter to the EU in 2024. This surge has severely affected the Spanish tomato sector, causing a 50% reduction in cultivated area and export capacity over the last 20 years.

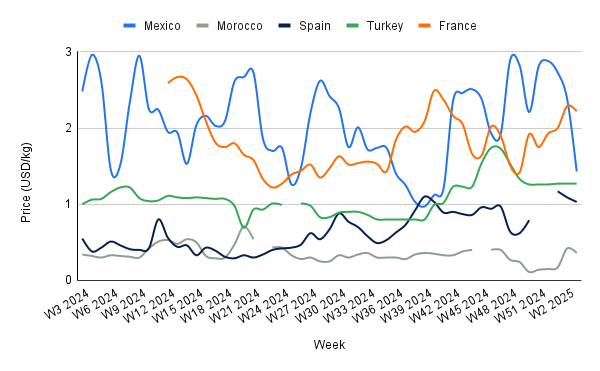

- Tomato prices in Mexico fell sharply WoW due to favorable domestic weather and reduced export demand. Morocco's prices dropped, driven by lower production.

- Türkiye's tomato prices rose YoY due to reduced domestic supply from adverse weather and increasing export demand. Meanwhile, varying prices in Spain, France, and Ukraine reflected changes in production levels and seasonal factors.

1. Weekly News

Morocco

Moroccan Tomato Imports Avoid USD 75 Million in EU Tariffs Since 2019

The Committee on Agriculture (COAG) estimates that Moroccan tomato imports into the European Union (EU) have avoided tariffs worth USD 75.08 million since 2019, labeling this a fiscal crime and considering legal action. COAG notes that Moroccan importers annually avoid paying at least USD 14.64 million in tariffs by exceeding the 285 thousand metric tons (mt) quota for tariff-free imports allowed between October and April. This quota applies if entry prices exceed USD 48.10 per 100 kilograms (kg). According to COAG, Morocco exports 500 thousand mt annually, leaving 230 to 240 thousand mt subject to unpaid customs duties.

COAG Raises Alarm Over Moroccan Tomato Exports Impact on European Markets

According to COAG, Morocco surpassed Spain as the leading tomato exporter to the EU in 2024 and now exports more tomatoes than the entire EU combined. COAG claims that Morocco exports double the agreed-upon quota, with 500 thousand mt of tomatoes shipped annually. Of this figure, 300 thousand mt go to France, which acts as the gateway for Moroccan tomatoes to Europe. COAG highlights that European companies, primarily French and Spanish, operating in Morocco are driving this trend. This surge in Moroccan exports has severely impacted the Spanish tomato sector, which has seen a 50% reduction in cultivated area and export capacity over the last 20 years. Particularly affected are regions like Andalusia, where tomato acreage has dropped from 12 thousand hectares (ha) to 8 thousand ha, and the Canary Islands, which have nearly lost their tomato export surface.

Peru

Peru’s Tomato Exports Surge by 124% YoY in Dec-24

Peru exported 384 mt of tomatoes in Dec-24, marking a significant increase of 124% year-on-year (YoY) compared to the 171 mt shipped during the same month in 2023. During this period, Peruvian tomatoes were exported to 11 countries, with Ecuador as the top destination, accounting for 38% of the total exports, followed by Colombia with a 22% share.

Ukraine

Greenhouse Tomato Prices Rose in Ukraine Amid Supply Shortages

In W3, wholesale prices for greenhouse tomatoes in Ukraine rose to USD 2.01 to 2.48/kg, a 10% increase week-on-week (WoW), driven by reduced supply due to adverse weather in Türkiye, the country’s primary supplier. Current prices are 36% higher than mid-Jan-24 levels, but weak demand discouraged sellers from raising prices further. Analysts believe this price surge is temporary and expect prices to decline as supply stabilizes in the coming weeks.

2. Weekly Pricing

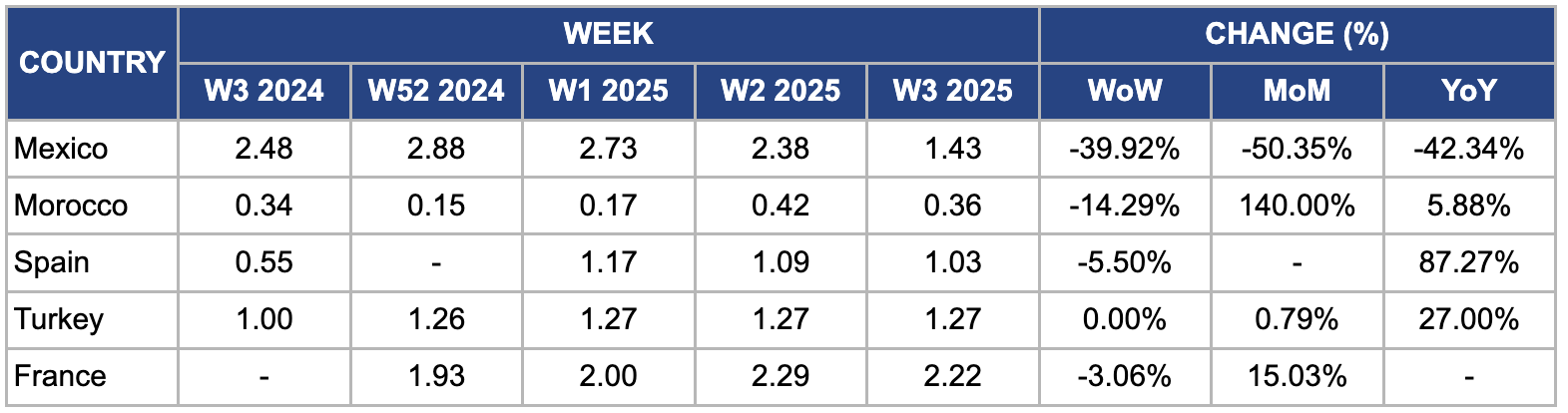

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W3 2024 to W3 2025)

Mexico

In W3, Mexico's tomato prices declined sharply to USD 1.43/kg from USD 2.38/kg, reflecting a 39.92% decrease WoW, 50.35% month-on-month (MoM), and 42.34% YoY. This significant price drop is due to a surge in domestic supply, driven by favorable weather conditions in key production areas like Sinaloa and Baja California, resulting in higher yields. Reduced export demand, especially from the United States (US), due to seasonal adjustments and ample domestic supplies, has also helped alleviate price pressures. The recovery in production levels after earlier supply chain disruptions has also played a role in stabilizing prices compared to the previous year.

Morocco

In W3, Morocco’s tomato prices declined 14.29% WoW, dropping to USD 0.36/kg from USD 0.42/kg. This decline was due to a lower-than-usual Moroccan production following the high supply from Oct-24 to Dec-24, significantly impacting global supply, particularly for round, cherry, and plum tomatoes. At the same time, demand has been increasing, as is typical after the Christmas period, which is putting upward pressure on prices. Cold weather has slowed down harvests across all products, contributing to higher prices, and temperatures are not expected to rise in the coming weeks, which could further influence market conditions.

Spain

In W3, Spanish tomato prices dropped by 5.50% WoW, falling to USD 1.03/kg from USD 1.09/kg. This decline is primarily due to an oversupply driven by record production levels. Between Jan-24 and Sep-24, Spanish tomato exports increased by 18.61% YoY. However, despite the increase in export volumes, the price of exported tomatoes has decreased by 23.9% during this period. The total volume of tomatoes exported by Spain during these nine months reached 499,990 mt, reflecting an 18.61% YoY increase. The average export price for tomatoes has declined by 23.9% YoY in 2024, further contributing to the price reduction in the domestic market.

Türkiye

In W3, Türkiye's tomato prices remained relatively stable WoW but increased by 0.79% MoM and 27% YoY, reaching USD 1.27/kg. The slight price increase is primarily due to reduced domestic supply caused by cold weather that negatively affected greenhouse production in Antalya, the country's top greenhouse production region. Crop yields in Antalya have significantly dropped due to low temperatures, heavy rainfall, floods, and storms. Moreover, rising export demand from neighboring countries and the Middle East has placed upward pressure on prices. Increasing transportation costs and logistical challenges have further hiked prices, elevating overall distribution expenses.

France

In W3, France's tomato prices declined by 3.06% WoW to USD 2.22/kg. This decrease is primarily due to reduced greenhouse tomato production, which reached 436,236 mt in 2024, a 9% YoY decline. The decline in production volume is mainly attributed to a drop in greenhouse production, while outdoor production has seen a 19% increase over the previous year. Furthermore, the scarcity of good-quality tomatoes has increased competition among processors seeking superior stocks.

3. Actionable Recommendations

Implement Strategic Price Management

Morocco and Mexico should collaborate with agricultural associations to develop strategic price management frameworks. By implementing mechanisms such as strategic storage during periods of abundant production, farmers can regulate supply levels in the market. This approach helps control supply shortages or surpluses, ensuring prices remain stable and sustainable. For example, farmers could store excess tomatoes during peak harvest times and release them gradually when supply is lower, preventing drastic price drops and stabilizing their income throughout the year. These strategies can be coordinated through local agricultural cooperatives or marketing boards to provide better market signals and prevent extreme price volatility.

Enhance Supply Chain Resilience

Given the impact of extreme weather conditions like cold weather, floods, and storms, countries like Türkiye and Spain should prioritize investing in advanced agricultural practices that improve weather resilience. This includes adopting climate-smart farming technologies such as high-tech greenhouses, irrigation systems, and temperature-controlled storage. For example, greenhouse farming could protect crops from the harsh effects of cold weather and allow for more controlled production. Moreover, improving irrigation systems can help mitigate droughts or water shortages, ensuring consistent crop yields year-round. Strengthening logistics networks by optimizing transportation and storage solutions can also reduce losses from supply disruptions, ensuring that supply levels are maintained even during adverse weather events.

Diversify Export Markets

To reduce dependency on saturated markets like the EU and mitigate the risks posed by tariff evasion and fluctuating demand, tomato exporters from Morocco and Peru should focus on identifying and penetrating emerging markets in regions such as Asia and Africa. Growing populations and increasing demand for fresh produce represent untapped potential. Exporters can explore countries developing infrastructure and evolving consumer preferences for high-quality tomatoes. Establishing new trade relationships and navigating these markets with tailored marketing and distribution strategies will help maintain consistent demand, stabilize prices, and reduce reliance on traditional markets that may be impacted by oversupply or regulatory issues.

Sources: Tridge, Agromeat, Agraria, Fresh Plaza, Unian, PEefeagro