1. Weekly News

Global

Global Dairy Industry Faces Diverse Challenges Impacting Milk Production

The European Union (EU) milk yield increased slightly by 1% year-on-year (YoY) to 62.79 million metric tons (mmt) in the first five months of 2024. Western Europe’s milk production peaked in Jun-24 and started to decline due to extreme heat and wet weather in crucial dairy-producing countries, including Ireland, the Netherlands, Denmark, and Britain. Milk processors in Western Europe are experiencing a shortage of cream due to strong butter demand in the European market.

Similarly, milk production in the United States (US) dropped by 5% month-on-month (MoM) and 0.8% YoY to 8.51 mmt in Jun-24. The decrease was observed in most regions of the country due to heat in the southern states and increased humidity in the Midwest and East. In addition, floods caused by Hurricane Beryl led to road closures in Vermont and New Hampshire, causing logistical problems in the east of the country.

Additionally, milk production in New Zealand decreased by 1% YoY to 228 thousand mt in Jun-24. The cumulative production in the first half (H1) of 2024 dropped by 1.5% YoY to 8.37 mmt. High production costs and reduced Chinese imports have decreased the country's milk production. Conversely, Australia experienced an increase in milk production. Still, it faces significant challenges, such as rising production costs, labor shortages, and adverse weather conditions. These varied challenges will continue influencing the global dairy market in the coming months.

Global Milk Production Expected to Decrease Slightly by 0.1% in 2024

According to the independent dairy online community Bullvine, global milk production is projected to decrease by 0.1% YoY in 2024, following a slight growth of 0.1% YoY in 2023. In particular, milk production in Argentina is projected to decline by 7% YoY due to economic instability, while other countries like the United Kingdom (UK), New Zealand, and the US are also expected to experience minor decreases. In addition, the global shift towards plant-based milk alternatives due to rising interest in healthy lifestyles will likely lead to a 6% YoY rise in their sales, further impacting traditional dairy production. Despite these challenges, milk production in Australia is forecasted to increase by 2% YoY due to improved weather conditions, stabilized production costs, and increasing profits.

South Korea

Milk Price Freeze and the Rise of Alternatives

Due to decreasing domestic milk consumption, South Korean dairy producers and processors have agreed to freeze milk prices at USD 0.79 per liter (L). Despite this effort, domestic milk products struggle to compete with cheaper imports, prompting dairy processors to diversify their product lines by including plant-based milk alternatives. As these alternatives gain a stronger foothold in the South Korean market, Tridge predicts that dairy farmers may protest and lobby the government for stricter regulations to protect the local dairy industry.

Argentina

Argentina Eliminates Export Tariffs on Dairy Products to Support Local Industry

On August 6, 2024, the government of Argentina permanently eliminated export tariffs on dairy products. This move removed the 9% tax on powdered milk and the 4.5% tax on cheese for foreign markets. These measures aim to support the local dairy industry by boosting profits and promoting productive activities. They align with the government's larger strategy to bolster the rural population and expand sales in international markets.

Belarus

Belarus Expands BUCE Trading List to Include Dairy Products

Belarus expanded the list of food products companies must sell through the Belarusian Universal Commodity Exchange (BUCE), which started on August 9, 2024. This change is published on the National Legal Internet Portal of the Republic of Belarus and primarily affects dairy products. Key additions include whole milk powder, butter with more than 72% fat content and less than 80%, endocrine-enzyme raw materials, and several other items. Under the new regulation, these products must now be traded wholesale exclusively through BUCE, ensuring greater transparency and regulation. This move aims to standardize pricing and improve market efficiency for these essential goods within Belarus.

2. Weekly Pricing

Weekly Powdered Milk Pricing Important Exporters (USD/kg)

Yearly Change in Powdered Milk Pricing Important Exporters (W32 2023 to W32 2024)

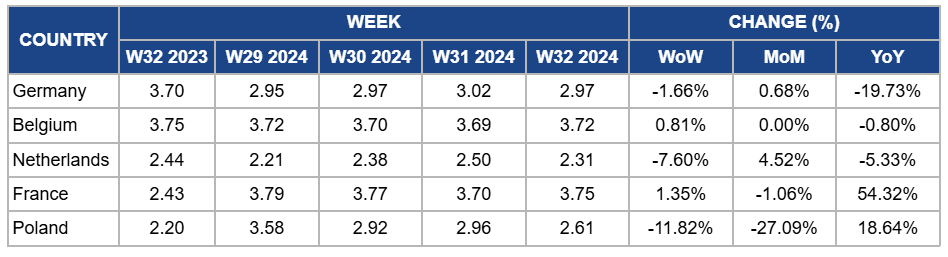

Germany

Germany’s powdered milk prices decreased by 1.66% week-on-week (WoW) to USD 2.97 per kilogram (kg) in W32 2024. The yearly comparison also observed a similar trend, with the prices declining by 19.72% YoY from USD 3.7/kg in W32 2023. This price decline is mainly due to decreased export demand, especially from China, which led to many European companies cutting milk powder production. Despite the decrease in the price of milk powder, cheese, and butter, prices are rising due to increasing demand during the tourist season.

Belgium

In Belgium, powdered whole milk prices increased slightly by 0.81% WoW to USD 3.72/kg in W32 2024, compared to USD 3.68/kg in W31 2024 due to increased raw milk prices. Despite this short-term price fluctuation, Belgium’s dairy industry faces challenges from Infectious Bovine Rhinotracheitis (IBR), a disease affecting cattle, with two cases identified in East Flanders, one case in West Flanders and an outbreak in a dairy farm in Antwerp. Poor biosecurity practices contribute to this infection. Belgium's animal health organization urges farmers to ensure strict biosecurity and only purchase animals under necessary circumstances.

Netherlands

Skimmed milk powder prices in the Netherlands decreased significantly by 7.6% WoW to USD 2.31/kg in W32 after a 5.04% WoW increase in W31. The price decline is due to low demand during the holiday season. Despite the price fluctuations in milk powder prices, the country’s raw milk supply is experiencing shortages due to extreme heat and wet weather, leading to a shortage of cream and raw materials for cheese production, affecting export markets and demand.

France

In W32, France's semi-skimmed milk powder prices increased by 1.35% WoW to USD 3.75/kg compared to USD 3.70/kg in W31. The price increase is due to the reduced raw milk production and the increasing demand for cheese during the tourist season. Milk yields in Western Europe peaked in Jun-24 and began to decline in Jul-24, which caused a supply shortage in many dairy processing factories. In addition, the heat has reduced the cow’s productivity and brought upward pressures on raw milk prices.

Poland

In Poland, skimmed milk powder prices decreased by 11.82% WoW to USD 2.61/kg in W32. The monthly price change was more significant, dropping by 27.09% MoM from USD 3.58/kg in W29, reflecting a weak powder market due to low demand. Poland’s milk powder exports declined due to decreasing demand from China, negatively affecting local production and prices. Consequently, many milk processing factories in Poland are cutting milk powder production to avoid losses.

3.Actionable Recommendations

Promote Local Dairy Products and Strengthen Market Position

With the rise of plant-based milk alternatives, South Korea's dairy industry needs to enhance its market position by promoting local dairy products' nutritional benefits and unique qualities. Dairy producers should consider launching marketing campaigns highlighting the health benefits of milk, such as its calcium content and essential vitamins. Furthermore, the industry should innovate by developing new dairy-based products such as sugar-free yogurt and cereal yogurt that cater to health-conscious consumers.

Expand Dairy Export Markets and Improve Production Efficiency

After eliminating the export tariffs on dairy products, Argentine dairy producers should focus on expanding their presence in international markets. Companies should conduct market research to identify high-demand regions and tailor their product offerings to meet specific consumer preferences in these markets. Additionally, improving production efficiency through adopting advanced breeding can help Argentine producers remain competitive on a global scale.

Maximize the Benefits of the BUCE Trading Platform

Belarusian dairy producers should fully leverage BUCE to enhance market transparency and efficiency. Producers must familiarize themselves with BUCE's trading mechanisms and ensure compliance with the new regulations. Additionally, they should explore opportunities to use the platform for bulk sales, which could lead to better pricing and more consistent demand. The government can monitor the platform's impact on the dairy sector and provide ongoing support to ensure a smooth transition and maximize the benefits for producers

Sources: Tridge, MilkUA, Rosng, Milkpoint, Milknews, Veeteelt