In W33 in the milk landscape, some of the most relevant trends included:

- A global increase in milk production, particularly from the EU and the US, is outpacing demand and putting downward pressure on dairy commodity prices. This trend is creating a challenging market outlook for the latter half of 2025, despite localized production declines in places like Australia.

- The UK dairy industry faces a severe labor shortage post-Brexit that threatens the national milk supply, prompting calls for government visa reform. In a positive development, the UK has secured smoother export access to Egypt by preventing a costly halal certification requirement, which is expected to boost trade.

- Dairy farming in the Netherlands is seeing a significant shift towards year-round indoor housing, with nearly a third of the national herd no longer having access to pasture. This move towards more intensive systems contrasts sharply with the organic sector, where outdoor grazing remains a key practice.

- Despite a strong supply forecast, New Zealand dairy prices are rising, driven by aggressive purchasing from China and Southeast Asia to replenish low stock levels. This high demand is creating unique market dynamics, including price premiums for certain products like WMP and AMF.

1. Weekly News

Global

Global Milk Surge Threatens Dairy Market Stability

Global dairy commodity prices are coming under increasing pressure as a surge in milk production across key exporting regions threatens to outstrip demand, according to an Aug-25 report from Maxum Foods, one of Australia and New Zealand's principal suppliers and manufacturers of dairy ingredients. This dynamic is weakening market fundamentals and pushing product values lower, creating a challenging environment for the second half of 2025. The primary drivers of this supply increase are the European Union (EU), where earlier constraints are now easing even as a hot, dry summer threatens future feed availability, and the United States (US), where strong milk and cheese production is outpacing sluggish domestic demand and export growth. Adding to the global surplus, New Zealand is also experiencing favorable production conditions, with its output projected to grow. This collective increase in supply from major players is creating a bearish global market sentiment. The situation in Australia provides a stark contrast, where ongoing feed shortages have led to increased culling and a forecast 2% decline in milk solids production for the upcoming season. However, this localized drop is not enough to offset the broader global trend of expanding supply, which is expected to pose a significant challenge for the international dairy community.

France

France Grapples with Fatal Listeria Outbreak Linked to Soft Cheeses

A deadly Listeria outbreak in France, linked to soft, pasteurized cheeses, has resulted in 21 infections, along with two fatalities, and is now spreading internationally, with cases confirmed in Belgium. The source has been traced to cheeses, including Saint-Nectaire and Saint-Marcellin, produced by Fromagerie de la Tour, prompting a wide-scale product recall. French health authorities have confirmed the presence of the Listeria monocytogenes strain at the company's production site in the Auvergne-Rhône-Alpes region and are conducting a full investigation. The outbreak, with cases dating back to Apr-25, poses a significant public health risk, particularly for vulnerable populations. This incident places the French cheese industry under intense scrutiny, highlighting the critical importance of stringent food safety protocols in the dairy sector.

Netherlands

Trend Towards Indoor Housing Grows in Dutch Dairy Sector

A new report from Statistics Netherlands (CBS), the central statistics bureau of the Netherlands, reveals a growing trend towards year-round indoor housing for dairy cows in the Netherlands. In 2024, the number of cows kept permanently indoors increased by 12%, meaning over 460,000 animals, or 31% of the national herd, no longer have access to pasture. This shift is occurring despite long-standing initiatives like the Grazing Agreement, which offers financial incentives to promote outdoor grazing. The organic sector stands in stark contrast to this trend. While making up only 3% of the national herd, organic cows spent an average of 202 days outside last year, 52 days more than their non-organic counterparts. This highlights a significant divergence in farming practices, with a growing portion of the conventional sector moving towards more intensive, indoor-based systems.

New Zealand

Chinese Demand Fuels New Zealand Market

Global Dairy Trade (GDT) prices are defying expectations, rising despite forecasts of a strong New Zealand supply season, driven by robust international demand. The primary catalyst is renewed and aggressive buying from China, particularly for Whole Milk Powder (WMP). This surge is fueled by low in-market stocks in China, seasonal purchasing ahead of the Chinese New Year, and a tighter-than-usual price spread between New Zealand and Chinese spot prices. Southeast Asia is also actively purchasing, supported by strong regional demand and low stock levels. A two-tier system is emerging for Skim Milk Powder (SMP), with different price points for high-spec and standard grades depending on the buyer. Meanwhile, a significant price discount has made New Zealand's Anhydrous Milk Fat (AMF) exceptionally attractive to European buyers, with the Netherlands now the second-largest destination after China. This arbitrage opportunity exists even after tariffs, creating strong demand for New Zealand fats. Logistical challenges, such as a shortage of specific 1-tonne packaging bins for AMF, are also creating premiums for certain formats, adding another layer of complexity to the market.

Major Shake-up in New Zealand's Dairy Processing Landscape

New Zealand's dairy processing sector is undergoing a major shake-up, with two large milk plants changing hands in a series of strategic deals. The a2 Milk Company is acquiring Yashili’s Pokeno facility for approximately USD 172 million (NZD 282 million), a move that secures crucial access to the lucrative Chinese infant formula market. Simultaneously, a2 Milk is divesting its 75% stake in the struggling Mataura Valley Milk plant for USD 61 million (NZD 100 million). The buyer, Open Country Dairy, New Zealand's second-largest processor, will acquire 100% of the high-tech facility, significantly boosting its capacity to produce higher-value products. While milk supply agreements for existing farmers will remain unchanged, these transactions signal a significant consolidation and strategic realignment within the industry, as major players optimize their assets to target key international markets.

United Kingdom

UK Dairy Sector Faces Labor Crisis, Threatening Milk Supply

The United Kingdom (UK) dairy industry is facing a severe labor crisis that is threatening the nation's milk supply and food security. According to a recent survey by the Royal Association of British Dairy Farmers (RABDF), 40% of producers are struggling to recruit staff, with nearly two-thirds of those who have recently tried to hire describing the process as very difficult or impossible. As a result of the ongoing labour shortages, 13% of farmers said they will leave farming altogether in the next 12 months if the situation does not improve. The crisis is largely attributed to the end of free movement of labor following Brexit, which has created a critical shortage of skilled workers. In response, industry bodies are urgently calling on the government to add dairy technicians to the skilled worker visa list. Without this intervention, the sector warns of a potential decline in domestic milk production, which could lead to increased reliance on imports and higher prices for consumers.

UK Secures Smoother Dairy Export Access to Egypt

British dairy farmers are set to benefit from continued access to a major international market thanks to a breakthrough with Egypt that will prevent a trade barrier due to come into effect next year. Following UK Government engagement, Egypt will not impose its proposed trade barrier requiring halal certification on all dairy imports. This change means British favourites like cheese and butter can continue to reach Egyptian shelves more easily and affordably, benefiting both UK farmers and international consumers. Preventing the trade barrier that was due to come into force in Jan-26 will protect an estimated USD 312.5 million (GBP 250 million) in additional export opportunities for farmers over five years. This development protects the existing USD 32.5 million (GBP 26 million) in annual dairy exports to Egypt and makes it easier for new businesses to enter the market. The removal of mandatory halal certification also cuts over USD 1,250 (GBP 1,000) in certification fees per shipment, directly boosting the competitiveness of British dairy products.

2. Weekly Pricing

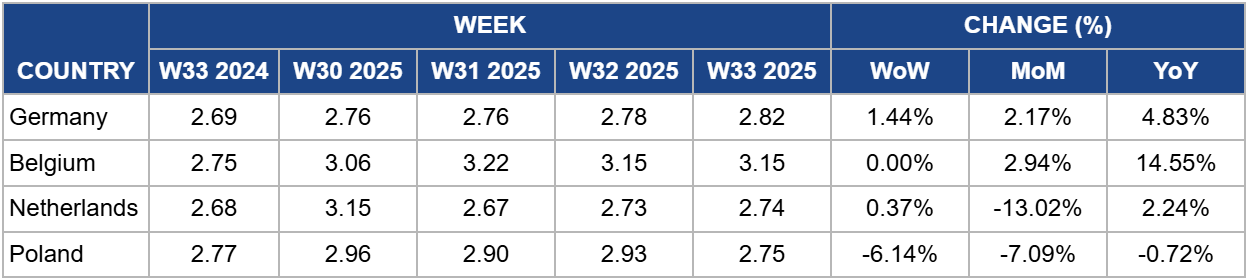

Weekly Powdered Milk Pricing Important Exporters (USD/kg)

Yearly Change in Powdered Milk Pricing Important Exporters (W33 2024 to W33 2025)

Germany

In Germany, the price of SMP was USD 2.82 per kilogram (kg) in W33, an increase of 1.44% week-on-week (WoW). This contributes to a 2.17% month-on-month (MoM) rise and a significant 4.83% year-on-year (YoY) increase. The German SMP market is showing renewed strength as the seasonal milk production peak subsides. The positive WoW and MoM price movements are driven by a tightening supply of raw milk. While Germany’s SMP production was up 4.9% in the first half of the year, this was achieved with a 2.5% decline in milk deliveries, indicating processors were heavily converting the spring flush. With that seasonal peak now over, the underlying scarcity of raw milk is reasserting upward pressure on prices. The significant YoY increase is a direct consequence of the broader structural supply constraints facing the EU dairy sector. Reduced cattle herds from disease and environmental pressures have created a fundamentally tighter raw milk market compared to the same period last year, supporting a higher price floor for storable commodities.

Belgium

In Belgium, the price of SMP was USD 3.15/kg in W33, stable WoW. This contributes to a 2.94% MoM rise and a significant 14.55% YoY increase. The Belgian SMP market is holding firm at a high price point, reflecting severe domestic and regional supply constraints. The WoW stability suggests the market has found a temporary equilibrium during the summer slowdown, after a period of upward momentum. The positive MoM trend is a direct result of a domestic supply squeeze, with SMP production down a substantial 8.9% and raw milk deliveries falling 3.8% in the first half of the year, tightening available stocks. The dominant long-term trend remains the 14.55% YoY price increase. This reflects the fundamental supply tightness across the EU, where reduced cattle herds have constrained overall milk production. The fact that Belgian SMP is among the most expensive in the EU underscores the severity of its domestic production shortfall, which keeps prices at a significant premium compared to last year.

Netherlands

In the Netherlands, the price of SMP was USD 2.74/kg in W33, a slight increase of 0.37% WoW. However, the price is down a significant 13.02% MoM but remains up 2.24% YoY. The Dutch SMP market is showing signs of stabilizing after a period of extreme volatility. The slight WoW increase suggests the market is finding a floor after a recent sharp correction, while the large MoM decline is a direct result of that same correction from a previous price spike. The market is likely still well-supplied from the seasonal peak, preventing a significant short-term rally. The YoY price increase, though modest, is supported by a tighter domestic supply situation, with both raw milk deliveries (-1.7%) and SMP production (-1.3%) down in the first half of 2025. This underlying scarcity, part of a broader EU trend of constrained milk production, is keeping prices above the levels seen at the same time last year.

Poland

In Poland, the price of SMP was USD 2.75/kg in W33, a sharp decrease of 6.14% WoW. This contributes to a 7.09% MoM decline and has flipped the YoY comparison to a 0.72% decrease. The Polish SMP market has experienced a significant bearish correction after a period of strength. The sharp WoW and MoM declines are likely driven by a combination of the typical summer slowdown in trading and the market reacting to Poland's increased raw milk supply, which rose 1.3% in the first half of the year (H1-2025). The reversal to a negative YoY comparison is a major development. It suggests that despite broader EU supply constraints and Poland's own significant reduction in SMP production (-7.5% in H1-2025), the increased availability of raw milk and potentially softer export demand are now pushing prices below the levels seen in 2024. The market appears to be correcting from previous highs, with the increased milk supply currently outweighing the reduced SMP output in influencing prices.

3. Actionable Recommendations

Counteract Price Pressure by Shifting to Specialized Products and New Export Markets

For producers and exporters in oversupplied regions like the EU and the US, relying on bulk commodity powders is a high-risk strategy in the current market. Instead of competing on volume, focus should shift towards diversifying into higher-value, specialized products such as specialty cheeses, milk protein isolates, or specific fat fractions that are less susceptible to global price declines. Simultaneously, companies must aggressively pursue market expansion beyond traditional channels. The UK's success in Egypt and New Zealand's strong demand from Southeast Asia highlight the immense potential in emerging markets. This requires investing in dedicated market intelligence to understand regional consumer preferences, dietary needs, and regulatory landscapes. By tailoring products and packaging to these specific markets, producers can build resilient revenue streams and mitigate the impact of regional oversupply scenarios.

Exploit Global Price Spreads to Maximize Import Margins

For importers, the current global supply glut is creating significant price disparities between exporting regions, presenting a clear opportunity for arbitrage. Actively exploit these differences by investing in real-time market intelligence platforms to monitor not just commodity prices, but also freight costs and tariffs from the EU, US, and New Zealand. The attractive discount on New Zealand's Anhydrous Milk Fat (AMF), for instance, should prompt a full landed-cost analysis against European sources. Adopt a more agile procurement strategy, blending spot-market purchases with shorter-term contracts to capitalize on fleeting price advantages. Importers should act decisively on this data, as the windows for these arbitrage opportunities are often narrow. By shifting from a static to a dynamic procurement model, importers can directly leverage market volatility to protect and enhance their profit margins during this period of oversupply.

Leverage Farming Systems as a Key Brand Differentiator

The growing divergence between indoor and pasture-based dairy farming, as seen in the Netherlands, requires producers and brands to make a clear strategic choice. Attempting to occupy the middle ground is a losing strategy, as they risk being out-competed on price by high-efficiency indoor systems while failing to meet the value-based demands of consumers who prioritize animal welfare. Companies should conduct consumer research to identify which attributes their target market values most—cost-effectiveness or welfare and sustainability credentials. Following this, they must align their operations and brand story with that choice. If a company pursues efficiency, it should communicate the technological and safety benefits. If it chooses pasture, it should invest in certifications and transparently market the advantages. By turning the farming system into a core part of a brand's identity, a producer can capture a dedicated consumer segment and defend its market position.

Sources: Tridge, UK Government, The Scottish Farmer, Rural News Group, Dairy News 7x7, NL Times, Euractiv, Dairy News Today