W33 2025: Palm Oil Weekly Update

In W33 in the palm oil landscape, some of the most relevant trends included:

- Indonesia's palm oil exports for MY 2024/25 are projected to decline to 22.8 mmt due to weaker demand from India, China, and the US, alongside higher domestic biodiesel use under the B40 mandate. However, production is expected to rise 3% in 2025/26 to 47 mmt, supported by favourable weather and sufficient fertiliser application.

- Malaysian CPO export duties will rise to 10% in Sep-25 following higher benchmark prices, reflecting the maximum rate under the country’s tiered tax structure and potentially limiting near-term export competitiveness.

- Global palm oil prices have been supported by tight vegetable oil markets, including firmer soybean and sunflower oil prices. Meanwhile, India’s shift toward record soybean oil imports may temper palm oil demand.

- Indonesia’s palm oil prices remain elevated, with YoY gains of over 28% despite recent minor dips, driven by sustained export demand, EU market access improvements under CEPA, and trade policy revisions. However, volumes exceeding EU quotas or slower global demand may moderate future gains.

1. Weekly News

Indonesia

Indonesia's Palm Oil Exports Decline in 2024/25 as Production Outlook Strengthens for 2025/26

Indonesia's palm oil exports for the marketing year (MY) 2024/25 are projected to decline to 22.8 million metric tons (mmt), primarily due to weaker demand from India, China, and the US, alongside higher domestic biodiesel use under the B40 mandate. However, production is forecast to rise by 3% in 2025/26 to 47 mmt, supported by favourable weather and sufficient fertiliser use. Between Oct-24 and May-25, palm oil prices surged 24% year-on-year (YoY), eroding competitiveness against other vegetable oils, though increased shipments to Pakistan and Bangladesh provided partial relief. Market sentiment has improved following the US tariff revision to 19% and the Indonesia–EU Comprehensive Economic Partnership Agreement (CEPA), which could lower European tariffs. While production growth underpins long-term supply, export performance will remain sensitive to demand shifts, trade policies, and currency fluctuations.

Indonesia's B40 Biodiesel Mandate Boosts Palm Oil Value and Cuts Fuel Import Costs in 2025

Indonesia's palm oil sector in 2025 has been shaped by the nationwide B40 biodiesel mandate, which requires 40% palm oil blending in diesel. In the first half of 2025 (H1-2025), the program distributed 6.8 million kiloliters (kL), saving USD 3.68 billion in foreign exchange through reduced fuel imports, while generating USD 583 million in added value from processing crude palm oil (CPO) into biodiesel. Having already achieved half of its 2025 target of 13.5 million kL, the policy underscores Indonesia's strategy to enhance value from palm oil while stabilizing trade balances.

Malaysia

Malaysia Sets Maximum 10% CPO Export Duty as Benchmark Price Rises in Sep-25

Malaysia will raise its CPO export duty to 10% in Sep-25, following an increase in the benchmark price to USD 959.51/mt (MYR 4,053.43/mt), a rise from USD 914.69/mt (MYR 3,864.12/mt) in Aug-25 when the duty was 9%. The revision, set by the Malaysian Palm Oil Board (MPOB), reflects the maximum rate under the country’s tax structure, which ranges from 3% to 10% depending on price levels.

Malaysia’s Palm Oil Futures Rise on Stronger Demand Signals Despite Higher Output and Stocks in Aug-25

Palm oil futures rose in early Aug-25 despite Malaysia's Jul-25 production reaching the highest level since Sep-24 and inventories climbing to a nearly two-year high. Oct-25 contracts on Bursa Malaysia gained 4.2% to USD 1,055/mt (MYR 4,435/mt), supported by China's restriction on Canadian canola imports and firmer Black Sea sunflower oil prices, offsetting recent declines in crude oil. Global vegetable oil markets remain volatile, with sunflower and soybean oil prices firming, while the USDA trimmed its 2025/26 output forecast. However, India is set to shift toward record soybean oil imports, reducing palm oil purchases, which could temper future price gains.

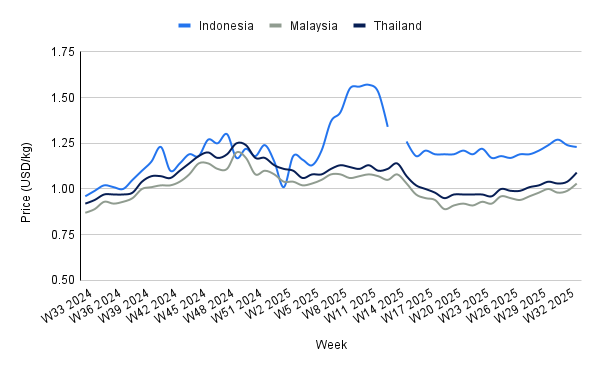

2. Weekly Pricing

Weekly Palm Oil Pricing Important Exporters (USD/kg)

Yearly Change in Palm Oil Pricing Important Exporters (W33 2024 to W33 2025)

Indonesia

In W33 2025, Indonesia’s palm oil prices declined by 0.81% both week-on-week (WoW) and month-on-month (MoM) to USD 1.23 per kilogram (kg), though they remain 28.13% higher YoY, reflecting strong demand and higher prices over the past year. In H1-2025, exports of CPO and derivatives rose 24.8% YoY to around 11 mmt, with average export prices up 22.2% YoY to USD 1,053/mt in Jun-25, driven by expanded EU market access and trade policy improvements under the upcoming CEPA. While the near-term price dip may signal market consolidation, sustained export demand and tariff reductions under CEPA could support prices going forward, although volumes exceeding the EU quota or slower global demand may moderate future gains.

Malaysia

Malaysia's palm oil prices increased in W33, rising 4.04% WoW to USD 1.03/kg and 18.39% YoY, supported by gains in futures, with the three-month benchmark at USD 1034.92/mt (MYR 4,372/mt) and FOB Malaysia for Aug-25 delivery reaching USD 1,062/mt, the highest so far this year. However, analysts note that rising stockpiles, which hit a 19-month high of 2.11 mmt in Jul-25, alongside continued production growth expected to peak in Sep-25 to Oct-25, could cap further upside in the near term. Price support may re-emerge later in Q4-2025 as Indian festive demand strengthens and output slows with the monsoon, while elevated soybean oil prices keep palm oil competitive in global markets.

Thailand

In W33 2025, Thailand's palm oil prices rose 4.81% WoW and MoM to USD 1.09/kg, up 18.48% YoY from USD 0.92/kg, reflecting tightening supply conditions. Palm oil production has declined 3 to 4% annually since 2025 due to climate shocks, labor shortages, and competition from other oils, contributing to market deficits. Continued supply constraints are likely to support prices in the near term, while any easing in labor or weather challenges could moderate future price increases.

3. Actionable Recommendations

Leverage CEPA and Tariff Adjustments to Boost Export Competitiveness

Indonesian exporters should optimize shipments to the EU under the Indonesia–EU CEPA, prioritizing volumes within duty-free quotas while strategically managing shipments beyond quotas. Continuous monitoring of global tariff trends and adjusting pricing strategies will help maintain competitiveness against soybean and sunflower oils.

Enhance Domestic Value through Biodiesel Integration

Producers and policymakers in Indonesia should continue to expand the B40 biodiesel program, targeting full-year distribution goals. Increasing domestic processing of CPO into biodiesel not only adds value but also stabilizes trade balances, mitigates foreign exchange outflows, and supports domestic demand during periods of weaker export markets.

Strengthen Market Intelligence and Supply Chain Coordination

Producers in Indonesia, Malaysia, and Thailand should invest in market intelligence to anticipate shifts in global vegetable oil demand, particularly in India and China. Coordinated inventory management and strategic shipment scheduling can stabilize prices, reduce stockpile pressure, and safeguard margins amid production fluctuations and climate-related supply constraints.

Sources: Tridge, Ukr AgroConsult, Grain Trade, Ainvest