In W35 in the palm oil landscape, some of the most relevant trends included:

- Ghana is working to close its large production-consumption gap in palm oil through the GTCDP and the “Red Gold” initiative, with measures focused on improved seedlings, out-grower schemes, value chain development, and tighter import regulations.

- India is diversifying edible oil sourcing by importing discounted palm oil from Colombia and Guatemala, increasing competition with Indonesia and Malaysia, and adding pressure to global palm oil futures.

- Indonesia raised its CPO reference price and export tax, which may limit export competitiveness. Meanwhile, exports are forecast to decline in 2024/25 under the B40 biodiesel mandate before recovering in 2025/26.

- Trade tensions remain central, with the US moving to exempt Indonesian palm oil from tariffs and Jakarta pressing the EU to remove countervailing duties and ease restrictions under the EUDR.

- Malaysia seeks tax relief for palm kernel oil products to reduce industry costs and preserve competitiveness, as domestic prices remain influenced by weaker soyoil trends, biodiesel demand, and currency effects.

- Pakistan's palm oil imports surged to meet domestic demand for cooking oil and ghee, reinforcing its reliance on imported edible oils despite falling exports of other agricultural commodities.

1. Weekly News

Ghana

Ghana Launches ‘Red Gold’ Initiative to Boost Palm Oil Production and Reduce Import Dependence

Ghana's Ministry of Food and Agriculture (MoFA) is implementing measures under the Ghana Tree Crops Diversification Project (GTCDP) to address the widening gap between domestic palm oil production and consumption. Annual consumption of roughly 250,000 metric tons (mt) far exceeds local production of 50,000 mt, creating economic and industrial pressures. The government's Medium-Term Expenditure Framework (2025–2028) and the ‘Red Gold’ initiative, Ghana’s strategic program to expand palm oil production, aim to boost output through improved seedlings, expanded cultivation, out-grower schemes, and the development of the entire value chain. New import regulations introduced by the Tree Crops Development Authority seek to curb substandard imports and encourage local production. Stakeholders highlight that small-scale producers and artisanal millers face low yields and inefficient extraction rates, underscoring the need for technology adoption and best practices to increase production and reduce import dependence.

India

India Turns to Latin America for Discounted Palm Oil, Raising Competition for Southeast Asian Suppliers

India has diversified its edible oil sourcing by purchasing palm oil from Colombia and Guatemala for the first time, as Latin American producers offered deep discounts to offload surplus stocks. The move comes as India's demand rises ahead of the festive season, with palm oil imports reaching 9 million metric tons (mmt) in 2023/24, mostly from Indonesia and Malaysia. Discounted South American cargoes, priced below Southeast Asian shipments despite longer delivery times, could increase competition and pressure Malaysian palm oil futures. Rising Indian demand, combined with new supply flows from Latin America, underscores intensifying competition in the global palm oil market.

Indonesia

Indonesia Lifts Sep-25 Palm Oil Reference Price

Indonesia raised its crude palm oil (CPO) reference price to USD 954.71/mt for Sep-25, up from USD 910.91/mt in Aug-25, according to a Trade Ministry regulation. As a result, the export tax will increase to USD 124/mt from USD 74/mt, alongside the existing 10% export levy. The higher reference price and tax structure could limit export competitiveness while supporting domestic availability.

USDA Lowers Indonesia's 2024/25 Palm Oil Exports, Sees 2025/26 Recovery

The United States Department of Agriculture's (USDA) Foreign Agricultural Service (FAS) lowered Indonesia's 2024/25 palm oil export forecast to 22.8 mmt, citing reduced demand and higher domestic use under the B40 biodiesel mandate. Production is projected to rise 3% to 47 mmt in 2025/26 due to favorable weather and improved yields. Industrial use is seen steady near 15 mmt, while food industry demand is expected to rise to 7.4 mmt. Exports are forecast to recover to 24 mmt in 2025/26, supported by Pakistan and Bangladesh, though weaker demand from China, India, and the United States (US) remains a constraint. Narrowing price gaps with rival vegetable oils continues to weigh on palm’s competitiveness. At the same time, Jakarta is pressing the European Union (EU) to remove tariffs on palm-based biofuels following a World Trade Organization (WTO) ruling in its favor.

US Agrees in Principle to Exempt Indonesian Palm Oil and Key Commodities from 19% Tariff

The United States (US) has agreed in principle to exempt Indonesian palm oil, cocoa, and rubber exports from the 19% tariff imposed in Aug-25, pending a final agreement. Aimed at products not produced in the US, the exemption would reduce tariffs to zero or near zero. The discussions also included potential US investment in Indonesian fuel storage and broader trade commitments, with Indonesia offering investments and purchases of American goods in exchange for tariff relief.

Indonesia Urges EU to Lift Biofuel Duties Following WTO Ruling, Seeks Free Market Access for Palm Oil

Indonesia has urged the EU to immediately lift countervailing duties on its biofuel imports following a favorable World Trade Organization (WTO) ruling. The Indonesian Palm Oil Association (GAPKI) criticized the EU's 8–18% duties as unjustified, citing a lack of evidence of actual harm to EU producers and alleged data distortions. GAPKI called for the restoration of free market access for Indonesian biofuels and emphasized the inclusion of 2.7 million smallholder farmers under the European Union Deforestation Regulation (EUDR). A forthcoming EU–Indonesia free trade agreement is expected to grant zero tariffs and special treatment for Indonesian palm oil.

Malaysia

Malaysia Seeks SST Exemption for Palm Kernel Oils to Boost Industry Competitiveness

Malaysia's Ministry of Plantation and Commodities (KPK) is seeking to exempt crude palm kernel oil and palm kernel olein from the 5% sales and services tax (SST), following their inclusion under the levy in Jul-25. The exemption request, submitted to the Ministry of Finance (MOF), targets raw materials used in oleochemical production rather than final products. Additional SST relief measures for key industry services are also under consideration to reduce costs and strengthen the global competitiveness of Malaysian palm oil products.

Malaysia's Palm Oil Market Expected to Remain Strong Amid Firm Exports and Trade Disruptions

Malaysia's palm oil market is forecasted to remain strong in the near term, supported by firm exports, manageable inventories, and global trade disruptions. CPO prices are projected to range between USD 993.19 and 1064.13/mt (MYR 4,200 and 4,500/mt), bolstered by shifting import tariffs, speculative buying, and higher soybean oil prices linked to US biofuel policy. Stronger shipments to India ahead of festivals are likely to sustain export momentum. While national inventories reached 2.11 mmt in Jul-25—the highest in nearly two years—production growth remains stagnant, indicating short-term supply-demand balance rather than oversupply.

Pakistan

Pakistan's Palm Oil Imports Rise 26% YoY in Jul-25 Driven by Growing Domestic Demand

In Jul-25, Pakistan significantly increased its palm oil imports to meet local demand, bringing in 286,836 mt valued at USD 302.15 million, an increase of 26.11% year-on-year (YoY) from 256,460 mt (USD 239.60 million). The rise in imports, alongside a surge in soybean oil imports, reflects efforts to fulfill domestic requirements for cooking oil and vegetable ghee. Overall, food commodity imports grew 44.90% YoY, while exports of key items, including rice, vegetables, and oilseeds, declined, highlighting continued reliance on imported edible oils to support domestic consumption.

2. Weekly Pricing

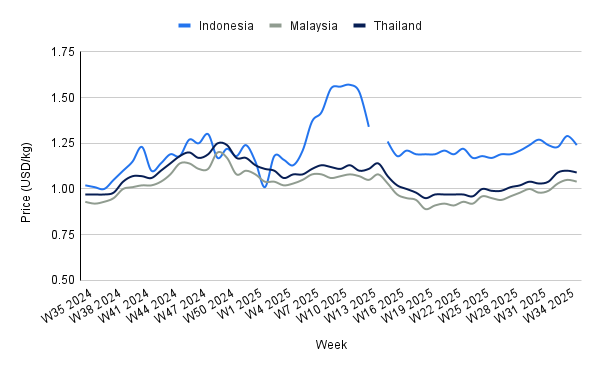

Weekly Palm Oil Pricing Important Exporters (USD/kg)

Yearly Change in Palm Oil Pricing Important Exporters (W35 2024 to W35 2025)

Indonesia

Indonesia's palm oil prices fell 3.88% week-on-week (WoW) to USD 1.24 per kilogram (kg) in W35, though they remain 21.57% higher YoY, reflecting sustained underlying strength. The Trade Ministry raised the Sep-25 CPO reference price to USD 954.71/mt, up from USD 910.91/mt in Aug-25, which lifts the export tax to USD 124/mt from USD 74/mt, alongside a 10% export levy. While the higher fiscal burden could limit exporters' margins and temper shipments, firm YoY gains signal resilient demand. However, if export volumes slow under the heavier tax regime, domestic inventories may build, exerting further downward pressure on prices in the near term.

Malaysia

In W35, Malaysia's palm oil prices eased by 0.95% WoW to USD 1.04/kg, though they remain 11.83% higher YoY from USD 0.93/kg in W35 2024. The decline was largely driven by weakness in soyoil across the Dalian Commodity Exchange (DCE) and the Chicago Board of Trade (CBOT) exchanges, which pressured palm oil due to its close substitution in the global vegetable oils market. Futures also retreated as traders monitored upcoming US–China trade talks, with the potential for increased Chinese soybean imports from the US shaping sentiment. While stronger exports and lower-than-expected domestic production continue to lend support, downside risks stem from softer crude oil prices, which reduce biodiesel demand, and a firmer ringgit, which raises export costs. Malaysian palm oil prices may remain range-bound, with external market cues and trade policy developments playing a key role in the near-term direction.

Thailand

Thailand’s palm oil prices dropped 0.91% WoW to USD 1.09/kg in W35, though they remain 12.37% higher YoY. The market faces mounting pressure from a sharp inventory buildup, with CPO stocks surging 112% since Jan-25 to 170,000 mt, as low global prices have curbed exports and refiners slowed purchases. Weak external demand, highlighted by large-scale cancellations from China and India, combined with Malaysian palm oil futures hitting a 17-month low, is dragging Thai prices lower. Unless government intervention supports domestic farmers, elevated stocks and sluggish exports point to further downside risks, potentially weighing on Thailand's palm oil prices in the near term.

3. Actionable Recommendations

Boost Local Value Chains and Technology Adoption in Emerging Producers

Ghana should prioritize mechanization and technology transfer for small-scale producers and artisanal millers, focusing on efficient extraction and higher-yield seedlings. Partnerships with private investors and international development agencies can accelerate value chain development, reducing reliance on imports while building a competitive domestic industry.

Diversify Export Destinations and Pricing Strategies amid Rising Competition

Producers in Indonesia and Malaysia should strengthen export penetration in secondary markets such as Pakistan, Bangladesh, and Sub-Saharan Africa to offset reduced buying from China and India. Flexible pricing strategies, including discounts on long-haul shipments, can safeguard market share against low-cost Latin American cargoes.

Leverage Policy and Trade Negotiations to Support Competitiveness

Southeast Asian exporters should maximize gains from tariff exemptions in the US and push for expedited implementation of zero-duty access under the EU-Indonesia Comprehensive Economic Partnership Agreement (CEPA). Coordinating with governments to ensure biodiesel mandates and tax adjustments are market-stabilizing will help balance domestic supply with export competitiveness.

Sources: Tridge, Hellenic Shipping News, Ukr Agroconsult, Grain Trade, Reuters