In W35 in the tomato landscape, some of the most relevant trends included:

- Spain's tomato sector is in crisis, as a 20% harvest shortfall due to extreme weather coincides with a price collapse that is making the crop unprofitable for farmers. This creates a significant supply chain risk for European buyers.

- Global trade dynamics are shifting. Argentina has aligned its tomato standards with the Mercosur bloc to streamline regional trade, while the EU has proposed eliminating tariffs on US tomatoes to secure a broader trade deal.

- Nations are aggressively investing in food security through technology and infrastructure. China has launched a high-speed air freight route to Dubai, drastically cutting delivery times for fresh produce to the Middle East, while Egypt and the UAE are pouring billions into agricultural modernization and agri-tech to boost domestic production.

- Scientific innovation offers a path toward climate resilience. Researchers in the US have discovered a natural immune response in tomatoes that protects them after droughts, providing a new avenue for developing hardier crops that can better withstand environmental stress.

1. Weekly News

European Union

EU Proposes Tariff Cuts to Secure US Trade Deal

The European Union (EU) is moving to eliminate tariffs on a wide range of American agricultural and industrial goods in an effort to finalize a major trade agreement with the United States (US). The proposal includes removing duties on key US exports such as oranges, tomatoes, pork, dairy, steel, and aluminum.

This move is a strategic concession aimed at persuading Washington to ease its own tariffs on European automobiles. By offering better market access for American products, Brussels hopes to secure a general tariff rate of 15% for its car exports, retroactive to August 1st. The European Council and Parliament must still approve the European Commission's proposal before the tariff reductions can take effect.

Argentina

Argentina Aligns Tomato Standards with Mercosur

Argentina has updated its quality and identity regulations for tomatoes to align with standards set by the Mercosur trade bloc. Implemented by the national food safety agency, Senasa, the measure replaces a 1995 rule and ensures that tomatoes produced in Argentina are automatically recognized in all member states.

This regulatory alignment is designed to streamline marketing and facilitate smoother commerce within the region. By reducing technical barriers, the update enhances the competitiveness of Argentina's tomato sector, which is concentrated in provinces like Mendoza and San Juan and exports primarily to Mercosur partners such as Paraguay and Brazil. The move strengthens market access and creates more fluid, secure trade conditions for this key horticultural product.

Brazil

Paraná Holds Fourth Place in National Tomato Production

Paraná remains as Brazil's fourth-largest tomato producer, with a 2024 harvest of 266,500 metric tons (mt) from 4,300 hectares (ha). However, the state's average productivity of 62.5 mt/ha falls below the national average. The 2025 year saw mixed results across its two harvests.

The first harvest yielded 174,200 mt, a 15% year-on-year (YoY) increase over the previous cycle. In contrast, the second harvest is expected to produce only 92,600 mt, a 16% YoY decrease attributed to pests and adverse weather conditions. This volatility was also reflected in the market, with tomato prices experiencing sharp fluctuations throughout the year for producers, wholesalers, and retailers alike.

China

Xinjiang Expedites Fresh Produce to Dubai with New Direct Flights

Xinjiang has launched a new direct air cargo route from Urumqi to Dubai, drastically cutting the delivery time for its fresh produce to the Middle East. The first flight carried nearly 18.5 mt of local agricultural goods, including melons, grapes, and tomato products.

Previously, shipping fruit to the region took 20-30 hours by air with layovers, or much longer by sea or land. The new direct flight takes only six hours, a more than 70% increase in efficiency. This reduction in transit time minimizes spoilage and ensures that seasonal fruits arrive in optimal condition. Xinjiang plans to establish similar direct freight routes to markets in Southeast Asia, Japan, South Korea, and Europe.

Egypt

Egypt Invests in Modernizing its Agricultural Sector

Egypt's 2025/2026 plan allocates almost USD 2.99 billion (EGP 144.8 billion) to advance its agriculture and irrigation sectors, aiming to bolster food security and economic growth. The strategy focuses on expanding land reclamation in key areas like the New Delta, improving crop yields by up to 15%, and increasing water use efficiency with modern irrigation. A core component is the expansion of contract farming to cover approximately 756,000 ha (1.8 million feddans), supporting key crops such as wheat, sugarcane, and tomatoes. Further goals include developing livestock to increase self-sufficiency, boosting agricultural exports to over USD 5 billion, and completing significant water management projects to support this growth.

Italy

Sea Reshapes Future of Agriculture

As traditional agriculture confronts mounting pressures from climate change, innovators are turning to the sea for solutions. Pioneering projects like Italy's Nemo's Garden demonstrate the potential of underwater biospheres, which create self-sufficient, pest-free environments to grow everything from basil to strawberries, accelerating plant growth and boosting antioxidant levels.

Similarly, seawater greenhouses are proving effective in arid regions. For instance, Australia's Sundrop Farms, uses this solar-powered technology to produce thousands of tons of tomatoes with desalinated seawater. Meanwhile, ancient techniques like Bangladesh's Food and Agriculture Organization of the United Nations (FAO)-recognized floating gardens offer climate resilience in flood-prone areas. The strategic importance of this emerging field is underscored by the prestigious Roullier Innovation Awards, which have dedicated its 2025-2026 cycle to the theme "From the Sea to Agriculture," signaling a significant shift toward sustainable and innovative food systems.

Russia

Russian Tomato Harvest Surpasses 217,000 MT

Russian farmers are actively harvesting open-ground vegetables, with the total collection so far exceeding 1.2 million metric tons (mmt). According to the Ministry of Agriculture, the tomato harvest has reached 217,800 mt, making it a significant portion of the yield.

Leading production is concentrated in the Astrakhan, Volgograd, Rostov, Moscow, and Belgorod regions. To support the sector's growth, the Russian government has implemented various measures, including allocating RUB 3.7 million in 2025 for vegetable and potato farming. This funding provides per-hectare subsidies and helps cover costs for modernizing storage facilities, ensuring the stability of the harvest.

South Korea

Cheongyang County Prepares Farmers for Prolonged Heatwave

Cheongyang County, South Korea, is taking preemptive measures to protect its horticultural farms from an unusual heatwave expected to last through Sep-25. With 2,716 farms growing crops like tomatoes, watermelons, and melons in over 660 ha of greenhouses, there is significant concern about heat-related damage.

The county's Agricultural Technology Center is advising a three-step management approach of shading, ventilation, and cooling, which can lower greenhouse temperatures by up to 8°C. Officials are also emphasizing farmer safety, urging them to avoid work during peak afternoon hours. To support these efforts, the county is investing USD 46,671 (KRW 65 million) in technology to help farms mitigate damage and ensure stable operations through the extended period of high temperatures.

Spain

Weather Disrupts Spain's Tomato Harvest

Extremadura's tomato harvest is facing a difficult season, with production expected to fall significantly below 2024 levels. The campaign was initially hampered by rains that delayed planting, followed by intense heatwaves that shortened the plants' growing cycle, reducing yields by an estimated 20%.

Compounding the poor harvest, market prices have plummeted from USD 174.88/mt (EUR 150/mt) to USD 134.07/mt (EUR 115/mt). This sharp price drop, combined with rising production costs, is pushing many farmers toward operating at a loss, making the crop unprofitable without yields of over 100 mt. The sector also faces growing concerns over competition from Chinese tomato exports, creating a challenging outlook for one of the region's most vital crops.

Andalusia Sets Record for Fruit and Vegetable Exports

Andalusia's fruit and vegetable exports soared to a record USD 5.89 billion (EUR 5.052 billion) in the first half of 2025 (H1-2025), marking an 11.6% YoY increase from the previous year. This performance solidifies the region's position as Spain's top exporter, accounting for 41% of the nation's total sales in the sector.

Tomatoes were the fourth most valuable export product, contributing USD 577.17 million (EUR 495 million) to the total with a 4.4% YoY growth. The leading exports were peppers, strawberries, and blueberries. Almería was the top-performing province, responsible for half of the region's sales. Europe remains the dominant market, with Germany being the largest single importer of Andalusian produce.

United Arab Emirates

How Nations Are Innovating to Secure Food Supplies

Highly dependent on imports, the United Arab Emirates (UAE) and South Korea treat food as a matter of national security. While Korea focuses on logistical efficiency and diversifying suppliers for staples, the UAE has become a global pioneer in agri-tech to bolster domestic production.

Through significant investments in vertical farming and hydroponics, the UAE now grows high-value produce like tomatoes and berries locally, year-round, reducing its reliance on foreign markets for fresh food. This strategy is complemented by maintaining large strategic reserves and owning farmland abroad. Both countries demonstrate that in a volatile world, food is a strategic resource that must be secured through foresight and technological innovation, not just purchased on global markets.

United States

Why Tomatoes Fortify Their Defenses After a Drought

After a drought, plants don't immediately resume growing; they prioritize self-defense. Salk Institute researchers discovered a rapid immune response, dubbed "Drought Recovery-Induced Immunity" (DRII), that activates within 15 minutes of rewatering. This mechanism was confirmed in both wild and domesticated tomatoes, which showed increased pathogen resistance.

When a thirsty tomato plant reopens its pores to absorb water, it becomes vulnerable to outside threats. The DRII response acts as a protective shield during this critical recovery window. The finding that tomatoes and other plants share this evolutionarily conserved strategy—choosing immunity over immediate growth—provides a new roadmap for engineering more resilient crops that can better withstand environmental stress and secure the global food supply.

2. Weekly Pricing

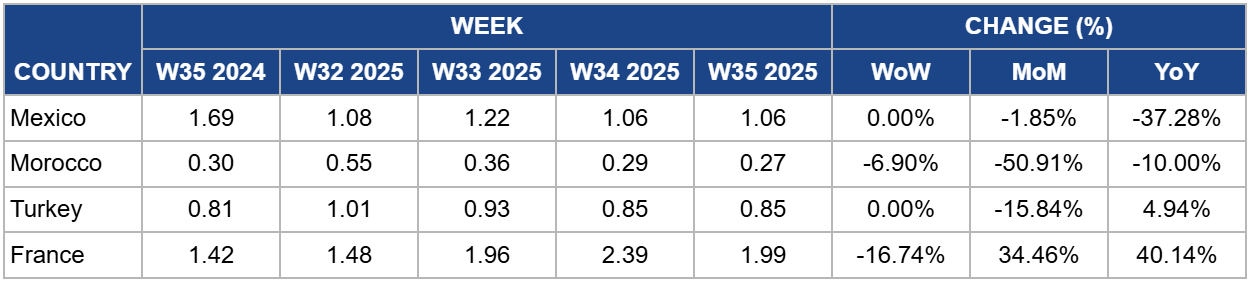

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W35 2024 to W35 2025)

Mexico

In W35, the wholesale price for Mexican round tomatoes held steady week-over-week (WoW) at USD 1.06 per kilogram (kg). However, this stability follows a significant downward trend, with the price down 1.85% month-over-month (MoM) and sharply lower by 37.28% year-over-year (YoY) due to the trade shock from the US’ termination of the Tomato Suspension Agreement in mid‑July and the imposition of a 17.09% duty on Mexican imports. Exporters have been forced to reroute volumes and adjust pricing, while the government’s August 8, 2025 minimum export price policy (USD 0.95/kg for round/bola; USD 0.88/kg for Roma; USD 1.70/kg for specialty types) effectively sets a floor that is helping stabilize quotes around current levels. Sector data show the dislocation’s scale: fresh tomato exports fell 19.2% YoY in H1-2025, the steepest first‑half drop since 2012, underscoring persistent demand uncertainty from the US market and explaining why prices remain depressed versus last year despite recent WoW steadiness.

Morocco

In W35, the wholesale price for Moroccan tomatoes decreased by 6.90% WoW settling at USD 0.27/kg. This continues a steep (MoM) correction of 50.91%, with the price also dropping 10% below last year's level. The sharp MoM slide reflects ample availability and an aggressive export tempo into the European Union (EU). This is particularly evident in Spain, where Moroccan shipments surged in early 2025, reinforcing Morocco's role as a key off-season supplier to the European market.Strong flows help satisfy elevated EU demand but simultaneously pressure origin‑side wholesale quotes when volumes move quickly through the chain. At the same time, continued sector resilience despite years of drought has enabled exporters to keep filling European gaps, even as European producer groups intensify pushback against Moroccan competitive pressure, an ongoing policy risk to watch for pricing ahead.

Turkey

In W35, the wholesale price for Turkish tomatoes was stable, remaining unchanged WoW at USD 0.85/kg. However, this weekly stability contrasts with a sharp 15.84% MoM decrease. Despite this recent drop, the price remains 4.94% YoY higher than the same period last year. The flat weekly print masks a typical late‑summer pattern: broad harvesting across regions and Turkey’s scale as one of the world’s largest tomato producers keeps supply heavy, tempering prices during peak availability. Local reporting of wide farmgate‑to‑retail spreads, offers as low as TRY 8/kg at the field versus around TRY 25/kg in urban markets, also points to abundant origin supply and strong throughput, consistent with softer wholesale export quotes. Even so, YoY firmness persists on cost pass-through and steady external demand, with some products increasingly directed to value-added channels such as dried tomato exports, which can lift the overall price floor as the fresh season transitions.

France

In W35, French wholesale round tomato prices saw a decrease of 16.74% WoW, dropping to USD 1.99/kg. Nevertheless, this weekly drop comes after a period of significant price hikes, and prices remain sharply elevated, up 34.46% MoM and 40.14% YoY. The pullback follows a weather‑driven spike through late August: extreme heatwaves and drought in southern regions (notably Occitanie) caused severe yield losses, reported at 60–80% for some growers, tightening domestic supply and pushing prices sharply higher before this week’s correction. As EU import flows picked up, particularly from Morocco and Spain, additional supply helped stabilize the market and cap further upside, allowing prices to retract from the W34 peak. Even with the WoW decline, lingering domestic shortfalls and quality issues from heat stress keep price levels well above 2024, implying continued volatility as France balances uneven local output with import pacing over the coming weeks.

3. Actionable Recommendations

Diversify to Mitigate Supply Risk

With Spain's tomato harvest facing a 20% yield reduction and farmer profitability collapsing due to low prices, buyers reliant on the Spanish supply face significant risk. European importers should immediately diversify their sourcing. Morocco remains a primary alternative, having already established itself as a key, cost-effective supplier to the EU. Exploring long-term contracts with Egyptian producers, who are set to expand production under a major government investment plan, would also be a prudent strategy to ensure supply chain stability.

Capitalize on the New China-Middle East Air Freight Corridor

Importers in the UAE and across the Middle East should leverage the new direct air cargo route from Xinjiang. The 70% reduction in shipping time minimizes spoilage and ensures a higher quality of fresh produce, including tomatoes. Buyers can secure a competitive advantage by establishing partnerships with Xinjiang-based suppliers to source fresher products and reduce losses associated with long transit times.

Invest in Climate-Resilient Production and Genetics

The severe weather-related disruptions in Spain and South Korea highlight the vulnerability of traditional agriculture. Agribusinesses and producers should invest in innovative, climate-resilient technologies like the seawater greenhouses used in Australia or the vertical farming methods pioneered by the UAE. Furthermore, the discovery of the DRII mechanism in the US provides a new frontier for Research and Development (R&D). Companies should focus on developing crop varieties that incorporate this trait to build more robust and stress-tolerant plants.

Prepare for Shifting Global Trade Flows

The global trade landscape for tomatoes is set for a shake-up. US exporters should prepare to capitalize on the proposed elimination of EU tariffs, which would open up significant market access. Simultaneously, traders within the Mercosur bloc can take advantage of Argentina's newly harmonized quality standards to facilitate smoother, more efficient commerce with partners like Brazil and Paraguay. Businesses must adapt their strategies to these evolving regulatory and trade environments.

Sources: Tridge, Ilnuovo Agricolotore, Phys Org, Mena FN, Afi News, Gulf News, Revista Campo, Government of Argentina, Portal do Agronegócio, Kvedomosti, Cuaderno Agrario, La Nueva España, International Produce Report